Inflation - Weak Services Push Composite Flash PMI Lower

The flash September composite PMI from Markit was weak because the service sector missed estimates sharply. The composite PMI was 53.4 which missed estimates for 55 and the prior report of 55.

This was below the lowest estimate of 53.8. This shows Markit is restarting its relative negativity after showing growth rebounded in the second half of August. Manufacturing was strong as it hit 55.6. This beat the consensus for 55 and the highest estimate which was 55.2.

It also was higher than August’s reading of 54.5. The service sector was the weak point as its PMI came in at 52.9. This missed the consensus for 55, the lowest estimate which was 53.6, and August’s PMI of 55.2.

Since the service sector is much bigger than manufacturing, it brought down the overall metric. This was more than canceling out the strong manufacturing reading.

Manufacturing can still be important because it tends to be more volatile than services. Services hit an 18 month low. Pushing the overall composite to a 17 month low. This is while manufacturing and manufacturing output hit a 4 month high.

Positive sentiment on services activity growth was the weakest since December 2017. Even with this weakness, there was a renewed increase in backlogs. There was also stronger new business growth. And finally, the fastest rate of job creation since May 2015.

Even though we’ve seen some inflation metrics moderate, the Markit report showed the opposite. Average prices charged by service providers increased at the quickest pace since at least October 2009. This is when the stat started being calculated.

Interestingly, even though the manufacturing PMI hit a 4 month high, the 12 month manufacturing outlook hit a 2.5 year low. This was partially because of higher costs due to the tariffs on metals. There was a decrease in manufacturing hiring growth consistent with the September BLS report.

Inflation - 3% GDP Growth & 200,000 Jobs Added

The Chief Business Economist at Markit stated this report is consistent with annualized GDP growth approaching 3% and non-farm payroll growth of 200,000.

It’s important to contextualize this report before blindly selling based on the services weakness. I need to see the full month’s report before judging because the flash reading for August was partially rescinded after the final reading.

This report is certainly weaker than the ISM reading. However, it’s not weak enough to coincide with the slowdown predicted by ECRI. I think growth is somewhere in between what the ISM and Markit show. The ISM report has been way too optimistic.

I expect GDP growth around 3%, but that can obviously change once we get the September hard data reports. Because the stock market has been overbought, any weak reports can be enough to catalyze a mini correction of about 5%.

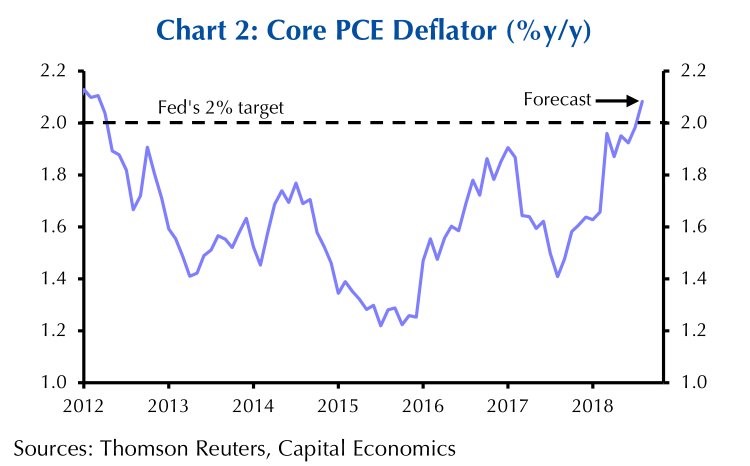

Inflation - Core PCE Forecast

The Fed has stated the inflation metric it focuses the most on is headline PCE, but everyone knows the Fed pays closer attention to core PCE based on its actions.

Since the Fed’s target for inflation is 2%, year over year core PCE getting above 2% is important. The PCE report comes out on Friday. The PPI and CPI showed year over year inflation growth declined. However, that’s not a guarantee we’ll the same result from the PCE report.

The consensus is for headline year over year PCE inflation to stay at 2.3% and core year over year PCE inflation to stay at 2%.

As you can see from the chart below, Capital Economics disagrees with the consensus as it expects core PCE growth to increase to 2.1% which would be above the 2% target.

That's not surprising because in 2017, July core PCE growth was 1.5% and August 2017 core PCE growth was 1.41%. Meaning, the base effect implies growth acceleration in August 2018. The Capital Economics analysis is much more detailed than that as it expects medical care inflation to accelerate which will bring the whole metric higher.

Since the PCE report comes out after all the other data (besides GDP) has been released, it usually isn’t shocking. That’s why a one tenth difference from the consensus is meaningful.

It would be especially meaningful in this report because it could be the first time inflation breached the Fed’s target in 6 years.

Keep in mind, this PCE report will come after the Fed’s rate hike on Wednesday, so it only could alter policy set at the November and December meetings.

Since there will likely be deceleration in core PCE in September and October because of the base effect, it’s reasonable to suggest that even if this reading beats expectations, it won’t change the Fed funds rate policy.

The Fed will probably raise rates one more time this year after the September hike, no matter what the PCE report shows. I’m more interested in the personal income aspect of the report this time.

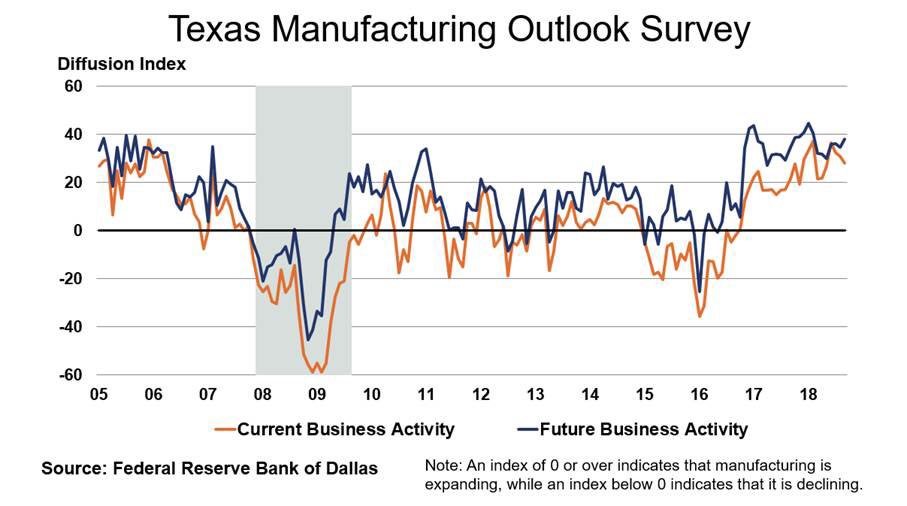

Inflation - Dallas Manufacturing Report Weakens

The September Dallas Fed manufacturing production index was 23.3 which fell from 29.3 in August. The general activity index missed estimates for 31.2, coming in at 28.1.

That was down from 30.9 in August. Every single metric declined as the new orders index fell 9.2 points to 14.7, the growth rate of orders fell 8.4 points to 11.5, and capital expenditures fell 8.1 points to 17.

Inflation metrics only fell slightly as prices received fell from 15.3 to 13.6 and prices paid fell from 45.3 to 44.4.

The company outlook and outlook uncertainty match the Markit PMI as the outlook fell 9.1 points to 18.2 and uncertainty increased 3.7 points to 19.9.

The sharp dispersion between current production and outlook appear to be catalyzed by the tariffs as manufacturing is more affected by trade than services.

Wages and benefits index fell 0.4 to 33 which makes sense because manufacturing hiring has weakened slightly.

Oddly, even though the outlook was weak, the 6 month future indexes were stronger than the current month.

General business activity index increased 3.3 points to 38. New orders only fell 2.5 points to 44.9 and wages and benefits increased 11.9 points to 57.4. Overall, this report showed signs of weakness, but it doesn’t overtake the strength seen in the Empire Fed and Philly Fed indexes.