Spending Finally Falls

Many have been predicting that Redbook retail sales growth would fall in the next few weeks as people are done excessively grocery shopping. People need to actually eat and use what they bought at the grocery store when they hoarded goods in mid-March. Plus, people now know how much they need to live.

It’s not surprising that people would err on the side of buying too much considering the worries about health and safety. Now people know the routine of how life will be in an economic shutdown. Stores won’t run out of items. It’s ok to be calm, yet precautionary.

In the week of April 11th, Redbook same store sales growth fell from 5.3% to -2%. It’s rare for this calculation to show negative growth. Now that it is negative, we can actually trust it more because obviously spending is down. Every private data point shows spending is down on most items. Many will be watching Redbook data closely to see when consumption starts to recover.

On Wednesday, the March retail sales report comes out. This will be the first retail sales data that includes the recession. It’s amazing how delayed this feels. Normally, having the data from the previous month isn’t a big deal because the economy is relatively stable. Now, 6 weeks ago is like a completely different world. Every aspect of our lives is different from early March.

With that being understood, monthly retail sales growth is expected to be down 7% and control group sales growth is expected to be down 1.8%. Implied in the assessment is that auto sales will be down because excluding auto sales, monthly retail sales are only expected to be down 3%. We can expect non-store sales to do well.

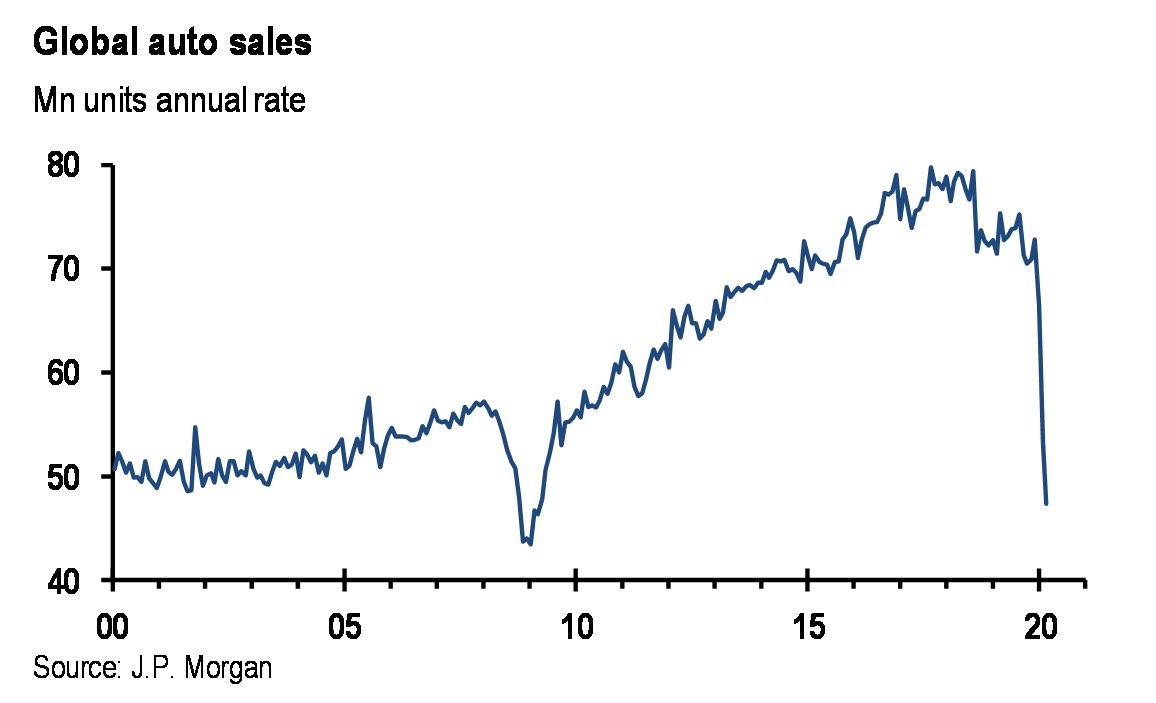

As you can see from the chart below, global auto sales have been crashing. They fell 11.2% in March after falling 19.7% in February because of China. This is a much bigger drop than the one in the 2008 recession. Data will only get worse in April. Despite this, Tesla stock has been on a tear. It’s up 56% since April 2nd.

IMF Lowers Estimates, But Is Optimistic On 2021

IMF always updates their forecasts well after changes are apparent. Since this move in the economy has been very sudden, it’s no surprise the IMF is behind the curve. Even Goldman Sachs has been caught behind the curve a few times in this recession.

As you can see from the image above, the IMF’s outlook for world GDP growth in 2020 is -3%, but the outlook for 2021 calls for 5.8% growth. There is expected to be a sharp rebound. The Euro area is expected to be hit the hardest as it will have -7.5% growth in 2020 and a rebound of 4.7% in the following year. America’s 5.9% decline this year is actually more optimistic than many estimates I’ve reviewed.

IMF is usually near the consensus. You will never see the IMF have the most optimistic or pessimistic view on Wall Street unless it is an old report. For example, before this update, the IMF was relatively bullish. However, everyone knew COVID-19 made those predictions obsolete.

Many thought the economy was about to rebound before this virus shut it. IMF is very optimistic about emerging and developing Asian economies. It sees a 1% increase in 2020 and a big rebound of 8.5% growth in 2021. Many think China will rebound in the 2nd half of this year. Because China was impacted first, it will probably outperform relatively in 2020, but underperform in 2021. That’s relative to its historical performance as it usually outgrows the rest of the world.

Global Fiscal Stimulus

The global economy is isn’t going to fall into a depression because of the explosion of fiscal and monetary stimuli. This stimulus shouldn’t necessarily make you bullish at these prices. It simply eliminates the worst case scenario. Even the most bullish catalyst would be for a vaccine to be developed this year and for the number of new daily cases to fall.

We’ve already seen the growth rate decline and there are talks of a vaccine coming soon. J&J might develop a vaccine by April 2021. Investors suspected the 18 month time horizon was too long.

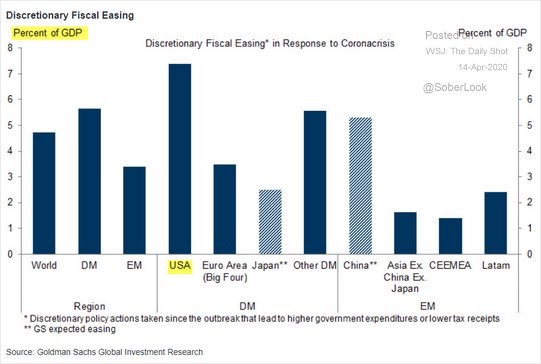

As you can see from the chart above, America has had the most discretionary fiscal easing as a percentage of its GDP. One of the main reasons it needs to ease more than other countries is the dollar has gotten too strong. The dollar usually spikes in times of fear.

Another obvious reason is America was hit the worst by the virus in terms of deaths and cases. NYC was hit the worst. Places like North Dakota, Hawaii, West Virginia, and Alaska weren’t hit hard, but they don’t contribute much to GDP.

Finance Leaders Think The Recovery Is 1-6 Months Away

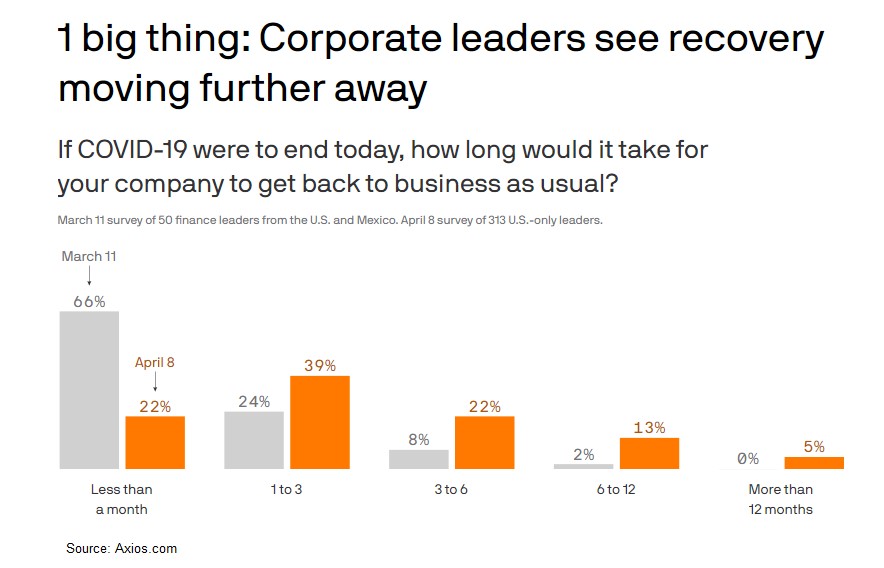

The chart below shows finance leaders have moved back their time horizon for a recovery. To be fair, we didn’t know that much about COVID-19 on March 11th. That was before the shutdowns were announced. The NBA, which was one of the first organizations to shut down, announced the suspension of its season on the 12th.

As you can see, on April 8th 22% said their company will get back to business as usual in less than 1 month. That’s probably too optimistic because the economy will only start to reopen in mid-May. 39% say the recovery will occur in 1-3 months, while 22% say 3 to 6 months. Keep in mind, this answer is different for each industry.

For example, the cruise industry isn’t going to go back to business as usual this summer even if the economy reopens before then. On the other hand, some companies are already close to doing business as usual. A lot of Amazon’s divisions are doing better than normally. That’s why its stock hit a record high on Tuesday.