Hawkish Fed - Stocks Fall As Fed Won’t Cut Rates

Stocks now must stand on their own because the Fed won’t support them with rate cuts. This isn’t necessarily a bad thing because earnings season has been solid and the ECRI leading index implies growth will improve later this year.

Atlanta Fed’s first few Nowcasts don’t matter much because they aren’t accurate. But it’s interesting to see the guess showing only 1.2% growth in Q2. That would be terrible. Essentially, that would be the Q1 growth rate without the boost from trade and inventories. Economic reports that support such a low growth rate could get the Fed closer to cuts. However, there might not be an opportunity to cut rates before the economy starts to turn around.

On Wednesday S&P 500 fell 0.75%, Nasdaq fell 0.57%, and Russell 2000 fell 0.93%. With earnings season mostly over, the market is going to go back to watching economic reports instead of earnings reports. Since the economic reports have been mediocre that’s not good.

Hawkish Fed - Could catalyze a correction.

Even though there won’t be a recession this year, the market has gotten way ahead of the fundamentals. A 5% correction is in order this month.

VIX rose 12.8% to 14.80. With that decline, the CNN fear and greed index fell from 66 to 62. Somehow the market is less than 1% away from its record high and this index is already close to being neutral again.

Regardless of what this indicator says, the market is extremely overbought in the intermediate term. S&P 500 is having its best start to a year since 1987 and the 18% monthly gain in the past 4 months is the best monthly streak since December 2010.

Hawkish Fed - Bond Market’s Reaction To Hawkish Fed

Chances of a rate cut next meeting and for the rest of the year fell. I never thought the Fed would cut to begin with. Why cut rates with the economy showing no sign of being near a recession?

Unsurprisingly, the near term bond market reacted sharper than long term bonds. The 10 year yield fell 2 basis points to 2.46% after the announcement. Then it went from 2.46% to 2.52% about an hour after the Fed statement was published. It settled at 2.5% which is where it opened. The 10 year yield is only 5 basis points above the Fed funds rate.

On the other hand, the 2 year yield had a much bigger reaction. Just after the Fed’s decision to not cut rates was announced, it fell from 2.26% to 2.21%. That's because the market thought this was a dovish announcement.

However, after it realized this was a modestly hawkish announcement, the yield rose to 2.31%. It closed at 2.3% which was a 4 basis point increase on the day. Therefore, the difference between the 10 year yield and the 2 year yield fell to 20 basis points which is still substantial.

In reaction to this move in the bond market, the financials fell 0.86% which was only slightly worse than the market’s performance. The worst sector was energy which fell 2.17% and the best sector was real estate which rose 4 basis points.

Hawkish Fed - Very Weak Inflation

This PCE report is the last report to still be affected by the government shutdown as data from February and March were released. Inflation was very weak in both months. Whenever PCE inflation misses estimates it’s a big deal. This report almost never is above or below estimates by a wide margin.

In February, overall inflation was 1.3% which fell from 1.4%. Core PCE price growth was 1.7% which missed estimates and January’s reading of 1.8%. Core inflation is below the Fed’s target. It stayed below that target in March. Even though energy prices were up 3.6%, headline inflation was 1.5% which missed estimates for 1.7%. It was up from 1.3%.

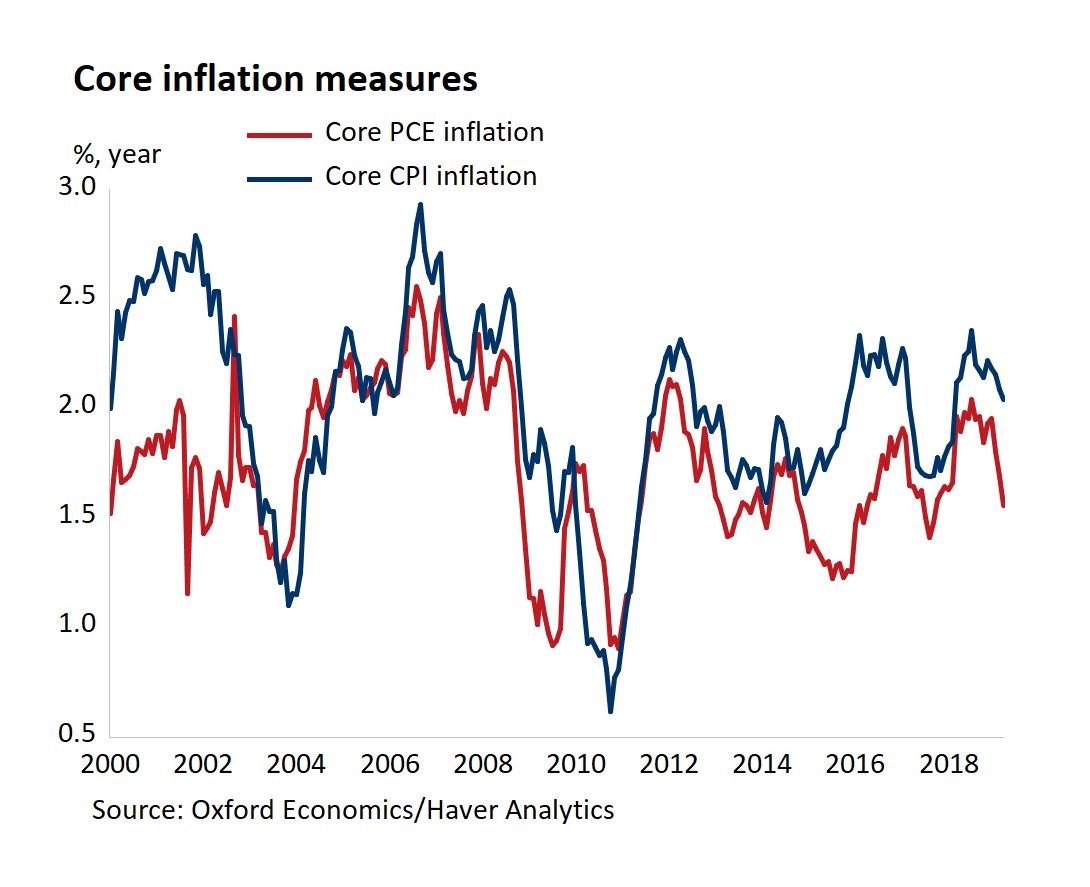

As you can see from the chart below, core PCE inflation was 1.6% which missed estimates and last month’s reading of 1.7%. The chart shows how core PCE inflation has fallen much sharper than core CPI. April CPI report will come out next Friday.

This weak reading partially explains why some investors were expecting more dovish language from the May 1st Fed meeting. However, the Fed thinks this dip in inflation is transitory.

Hawkish Fed - Weak Income Growth

March PCE report was very bad. Income growth missed estimates. Because consumer spending beat estimates, the savings rate plunged. Specifically, monthly personal income growth was only 0.1% which missed estimates for 0.4% and was below the low end of the consensus range which was 0.3%.

Consumer spending growth was 0.9% which beat estimates for 0.7% and the high end of the estimate range which was 0.8%. It’s good to see consumer spending growth beat estimates, but that’s unsustainable if income growth is weak.

As you can see from the chart above, real disposable yearly income growth was 2.3% which was the lowest growth rate since early 2017. Consumer spending growth was 2.9%.

As you can see, this is like the 2016 slowdown when real spending growth was above real income growth. This gap caused the personal saving rate to crater. It went from 7.3% to 6.5%. On a monthly basis, this was the biggest drop since January 2013. The savings rate still isn’t at cyclical lows, at least, as the rate is only the lowest since November.

Another month like this would be very bad for the consumer. Outside of the post-recession period, the cycle low was 5.8% in February 2013.

Personally, I think it’s more likely for consumer spending growth to fall in the next few months if income growth falls than it is for the savings rate to plunge again. Weekly Redbook report in the week of April 27th, showed yearly same store sales growth fell from 6% to 5.5%.

The decline was expected because the main reason why growth increased in the previous week was the Easter holiday. This wasn’t a great reading, but it wasn’t a bad one either.