Yet Another Terrible Jobless Claims Report

We've now had terrible jobless claims reports for 6 weeks, as the report on Thursday was poor yet again. Now people are starting to notice because seasonally adjusted claims rose for the first time since the peak on March 28th just as predicted. T

echnically, the streak ended last week as unadjusted claims rose. This report was the reverse as unadjusted claims fell. Keep in mind, the media and some lagging traders are still just realizing the economy is in a slowdown.

We knew there was a slowdown since mid to late June and the market knew about it from early to mid June. The market already priced in this weakness over a month ago. Rech stocks are having a bad July because the market is now pricing in a rebound in August and September.

That’s because national COVID-19 cases have peaked and a stimulus is coming. There are talks about a $100 weekly unemployment benefit that will last to the end of the year. Details on the plan will trickle out over the next few days; it will be passed by the 2nd week of August.

We're not expecting another spike in COVID-19 cases this fall because people are acting more cautiously (masks). Obviously, that can be wrong as the virus can mutate. This is just an expectation. Investors always have expectations, but they only act on them when they are confident in them and the market disagrees. The market has been rewarding cyclical stocks in July and selling the secular growth stocks so it agrees with me.

Specifics Of The Report

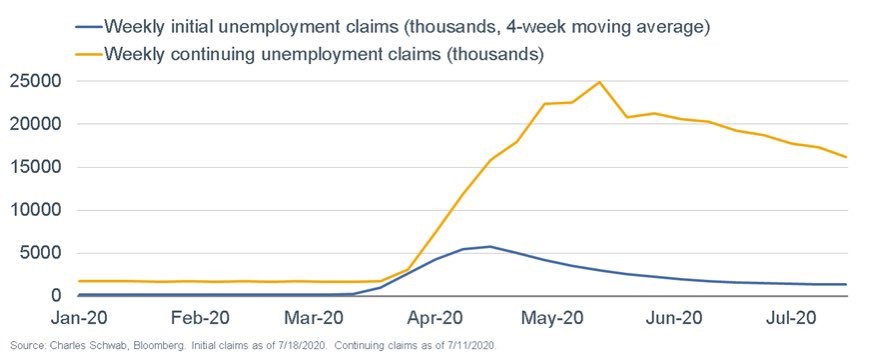

Specifically, initial claims were up from 1.307 million to 1.416 million. Because of the 7,000 upward revision to last week’s reading, they only fell 3,000 last week. Personally, I think some economists were scared to call for an increase after the record long 15 week decline in claims.

Consensus was 1.308 million. Economists always seem to be late to the party. Even in mid June, economists didn’t realize the strength of the rally; the economic surprise index hit a record high. Remember, this was the survey week for the BLS report. Initial claims picked a terrible time to end their streak of declines. This further supports my expectation for a weak BLS report. We can expect job losses.

As you can see from the chart above, continued claims in the week of July 11th fell from 17.304 million to 16.197 million. Next week is the survey week for this reading. It has correlated with the recent BLS reports. Even though last week’s initial claims reading wasn’t good, the continued claims reading was good. It had a 1.107 million decline which was the biggest decline since May 16th by a hair.

Many economists are adding up continued, initial, PUA, and other pandemic related claims. Since continued claims is the largest component, this reading makes that total look better. Unfortunately, PUA claims rose 19,000 this week to 2.35 million. That means unadjusted claims (including initial and PUA) fell 5%. That’s actually good compared to the past 4 weeks which had increases. It’s the biggest decline in 6 weeks.

COVID-19 Cases Fall On Thursday

Thursday was a good day for COVID-19 as cases fell from 71,967 to 68,295. That’s down from 73,388 last Thursday. It’s clear that the 7 day moving average is topping. Bad news is there were 1,117 new deaths which puts the 7 day average even closer to 1,000 like predicted. It will be easy to predict the decline in deaths because it will occur about 2-4 weeks after cases start falling. We can expect new deaths per day to peak in mid to late August.

At this point, I’m done with using Arizona as a signal. We already know the national number of new cases is done increasing. New signal is California because it is the largest state and one of the few hotspots that hasn’t peaked yet.

On Thursday, there were 10,024 new cases which was below Florida which had 10,249. That was down from the record 12,137 on Wednesday for California. Maybe Wednesday’s record will be the peak. We need a few more days of data to tell.

Tax Increases Are Coming

Let’s not call it tax reform. For investors, these are tax increases. It could still be bad for stocks which investors are completely ignoring. Long term tax rate paid by corporations has been falling for decades. That’s because there has been an international trend towards lowering the corporate tax rate. America finally got on board a few years ago.

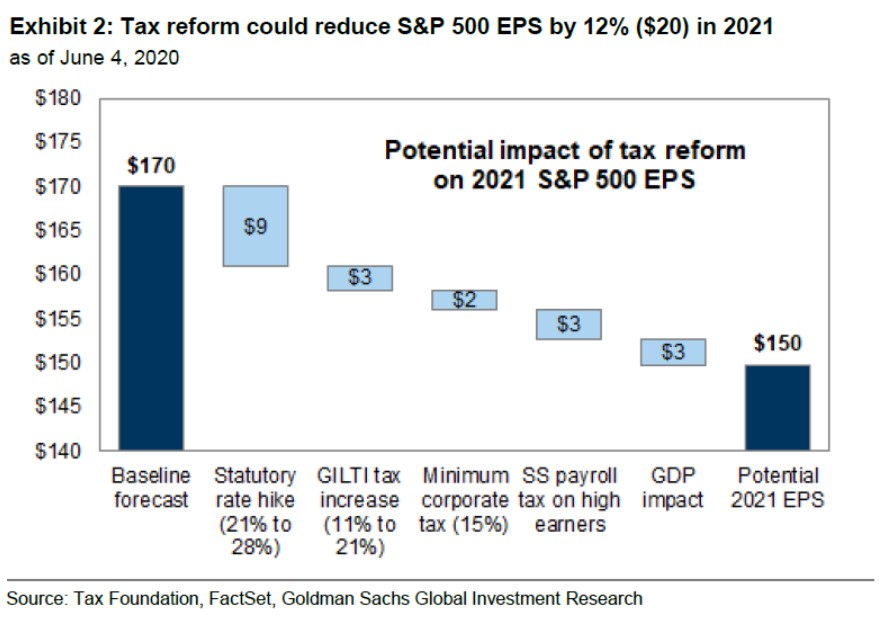

As you can see from the chart above, these tax hikes are going to have major impacts on earnings. Plus, the government might raise the capital gains tax which would be bad for traders (hence bad for stocks). Baseline impact of tax hikes could be $20. That would put the S&P 500’s 2021 EPS at $150 which means the current multiple is 21.6. That’s very expensive. The market is more expensive than usual because of the big internet stocks.

It’s possible that we can see a major sector rotation out of the FAANG names and into the value stocks. This is one thing Tesla doesn’t need to worry about since it barely makes a profit. Dems would likely pass new laws that help green technology like solar and electric cars. To be clear, the tech sector is more international so it will be less impacted by tax hikes.

Conclusion

Initial jobless claims reading was weak again. However, we are likely approaching the bottom of this slowdown. Maybe we see 2-3 more weeks of bad reports before the turnaround becomes apparent. States will start to fully reopen in August and September as the number of new COVID-19 cases falls.

Bad news for stocks is tax hikes will be coming if Joe Biden and the Democrats win the November election. We can expect a sector rotation out of the FAANG names because they are expensive.