Some Final Unwind Thoughts

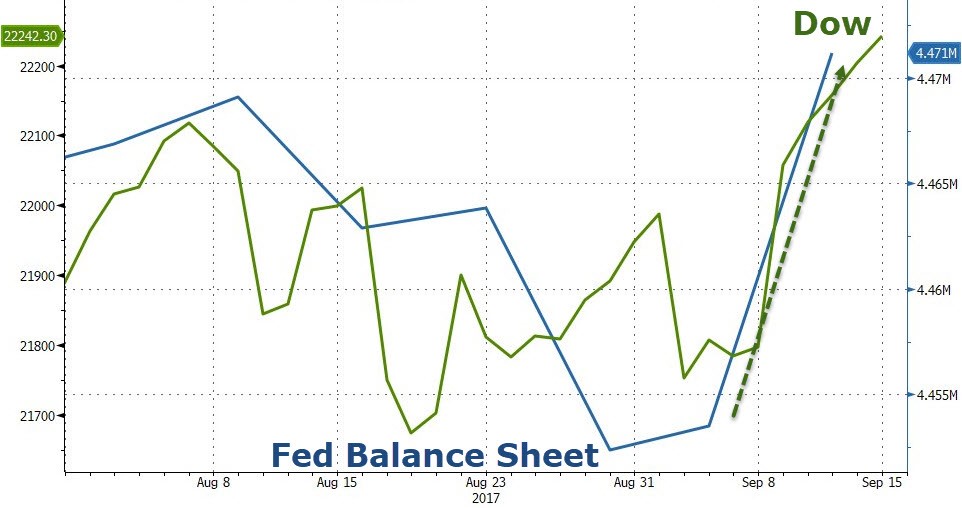

On Thursday, the Fed’s balance sheet was released like it is every week. As you can see in the chart below, the balance sheet increased $17.7 billion which was the biggest spike since December 2016. That’s weird timing because the Fed is expected to finalize the unwind announcement next week. This increase in the balance sheet is probably due to lumpiness in the maturity dates in the bonds outstanding. This calls into question how the unwind will look in action. The Fed is supposed to have a flat balance sheet right now because there’s no policy in place, yet there was a $17.7 billion spike this week. If the Fed can’t keep it steady now, then it probably won’t descend in a perfect trendline lower. That might or might not be a factor that will affect the markets.

One way it could affect markets at the start would be if the Fed does something unusual one week because of maturity date lumpiness and it spooks the market. We haven’t seen anything in the past few months affecting the market, but there will be more focus on the balance sheet now that it’s expected to change. Keep in mind, that I don’t endorse comparing the Dow to the balance sheet as this chart does because daily action is guided by hundreds of factors. Putting that all on the Fed is an oversimplification of the market. The Fed has had a heavy hand influencing stocks at times during this bull run, but daily spikes can be random or caused by a multitude of catalysts.

Another aspect to this could be extrapolations of Fed policy changes based on actions. That would be a throwback to times when rates were changed without vast explanations. I’m guessing that if there was a sharp change in the balance sheet and the Fed didn’t want to convey a policy change, an FOMC official would talk about it in an interview to calm the market. Considering the correlation with tapering and volatility, it’s surprising nothing has come up yet. My working thesis is that QE is a crutch for the market. When the economy is weak and earnings are sagging, the market looks to the Fed for a bailout. When the economy is solid and earnings are great, the market doesn’t wince at minor rate hikes, tapering, or a slow unwind. It’s not as if the Fed is ever hawkish; it just isn’t a crutch for the market. That’s why I think this unwind policy won’t start affecting the market when it commences in a few weeks.

If the start was going to affect markets, we would have seen trembles when it was floated earlier this year. I think this policy will start to matter when there’s turmoil in the markets and investors realize the Fed isn’t there to save them. The obvious place where I could be wrong is if the Fed abandons the unwind if the market falls. We talk often about how the market is lucky for the Fed to not be hawkish on rates, but the Fed is also lucky the market has been placid. There’s a good argument to be made that the unwind wouldn’t be starting in 2017, if the S&P 500 was down year to date.

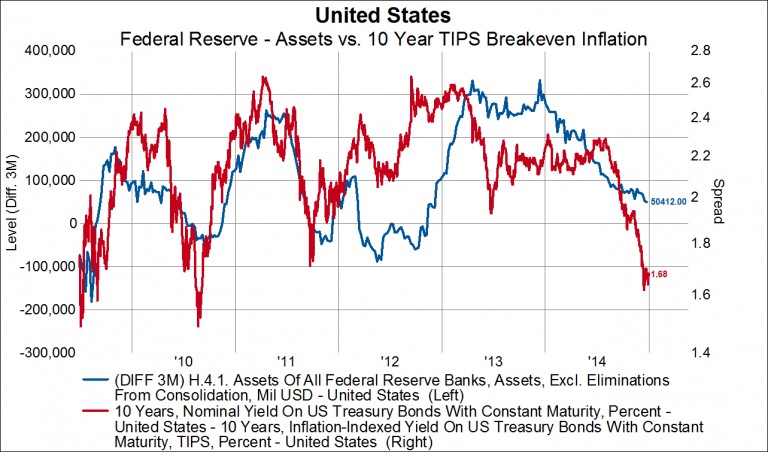

The impact of the Fed’s balance sheet to markets is hotly debated. That’s because it is uncertain. There’s not a clear explanation because, as I said before, the market had been volatile during tapering up until this year. The action this year is spurring some to argue the balance sheet doesn’t matter, but that’s hogwash. If it didn’t matter, then the Fed wouldn’t keep a $3 trillion terminal balance sheet. It would let all the bonds it owns mature. The chart below gives you a comparison between the 10-year breakeven inflation rate and the Fed’s assets. As you can see, when the Fed stopped QE from 2009 to 2014, there was a drop in inflation. This year we’ve seen a drop in inflation. The obvious question is whether the unwind further pressures inflation. The inflation rate is already low, so that would push it towards a zero handle. By the way, we have seen a minor pick-up in the breakeven inflation rate to 1.85 from 1.66 in the past few weeks. That helped me accurately anticipate the boost in CPI in August.

Economic News

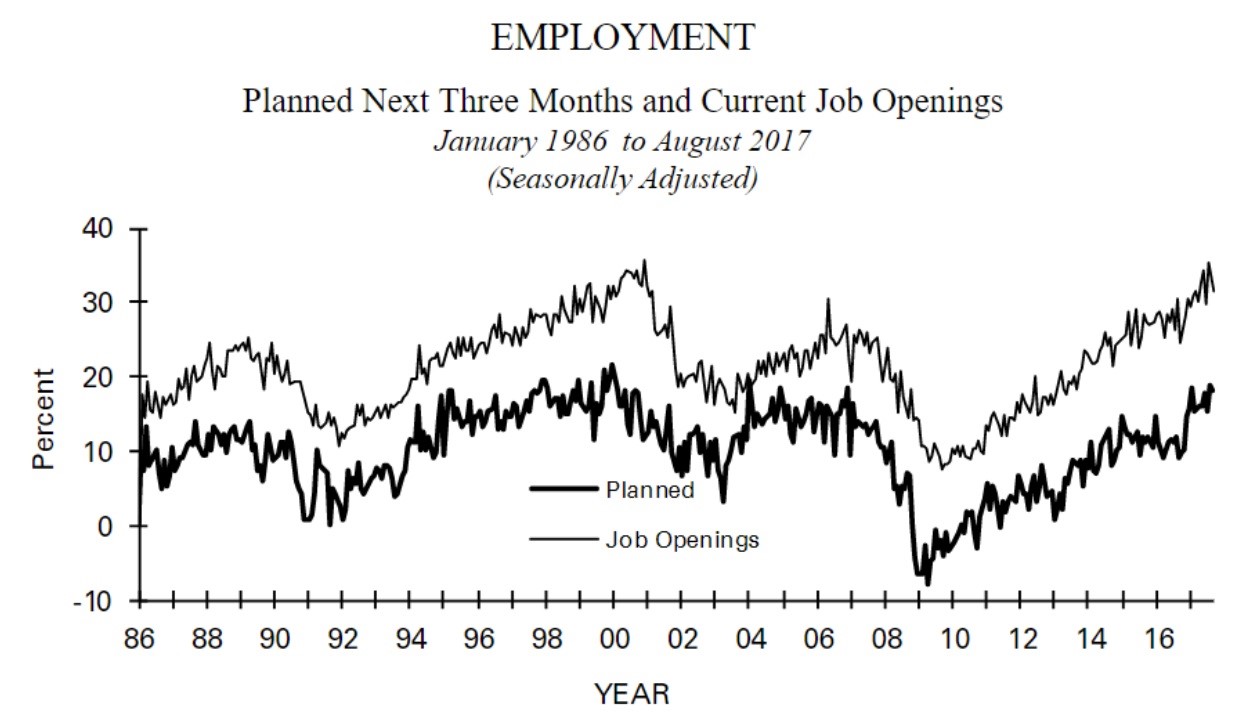

One aspect of the labor market we’ve discussed often in the past few months is how the number of jobs openings that go unfilled is increasing. This is especially true for manufacturing jobs and small businesses looking for workers. The survey below is an update to that situation. This time the job openings fell by 4 points to 31 and the hiring plans fell by one point to 18. That didn’t narrow the gap much. In an optimal situation, we’d want to see planned hiring shooting up while openings are stagnant. Compensation changes improved this month near the highs seen earlier in the year. This further signals tightness in the labor market.

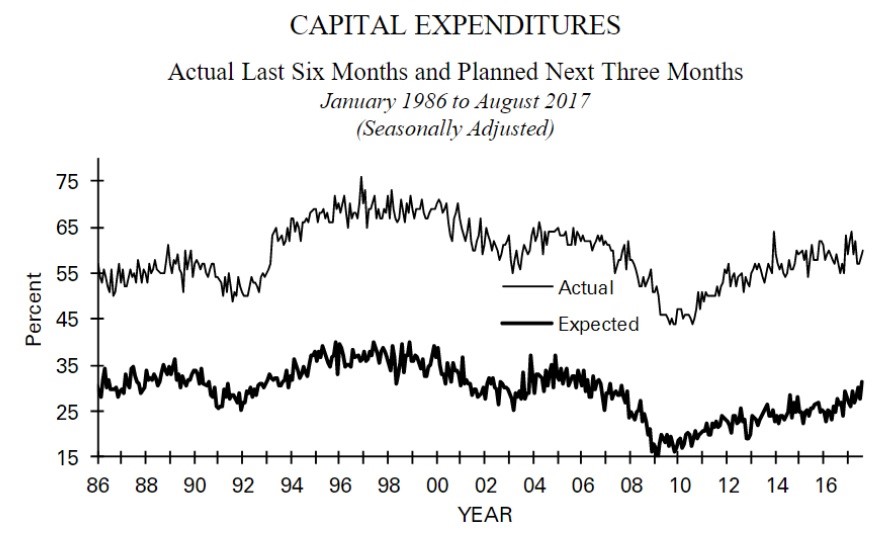

We’ve looked at charts previously showing how investors want firms to put more money into capex. While small businesses aren’t the companies investors were talking about in that survey, the chart below shows capex plans and actual actions this cycle still haven’t met the peaks seen in previous cycles. This is perplexing because this survey showed credit conditions were amazing and sales were impressive. This is one of the unanswered questions of this business cycle.

Conclusion

The Fed’s guidance on future rate hikes and balance sheet reductions will be the focus of next week. As far as who will be picked to be the next chair, Yellen is at 24%, Warsh is at 20%, and Cohn is at 16%. There has been some sensing that President Trump is moving towards the center on issues. That would foster the possibility of Yellen being picked. We will know very soon who the pick is.