Fed Doesn’t Change Rates

In a surprise to no one, the Fed didn’t cut or hike rates. Most discussed quote by Powell was when he said, “We’re not thinking about raising rates. We’re not even thinking about thinking about raising rates. What we’re thinking about is providing support for the economy. We think this is going to take some time.” This surprised no one. The economy either is in a recession or just exiting one. Fed has multiple QE programs in place to combat it. Obviously, the Fed won’t be hiking rates soon. We’d need to see very high inflation for the Fed to hike rates.

To be clear, some are not 100% on board with the Fed’s goal to keep rates near 0% through 2022. It's certain that rates will stay at 0% throughout this year and next year. We don’t have an outlook on 2022. Fed doesn’t know what will happen then either. This forward guidance is about affecting markets now. Fed can always change its mind and raise rates in 2022.

And, this cycle is much different than the last one, meaning rates are unlikely stay near zero for as long. Fed kept rates near 0% for 7 years. Even if the Fed raises rates in 2023, this cycle will be quicker. Last recession was a financial crisis; this was an exogenous event. And the unemployment rate will fall quicker than it did in the last expansion. That being said, there is a lot of uncertainty right now, so minds can change.

Review Of Fed Statement

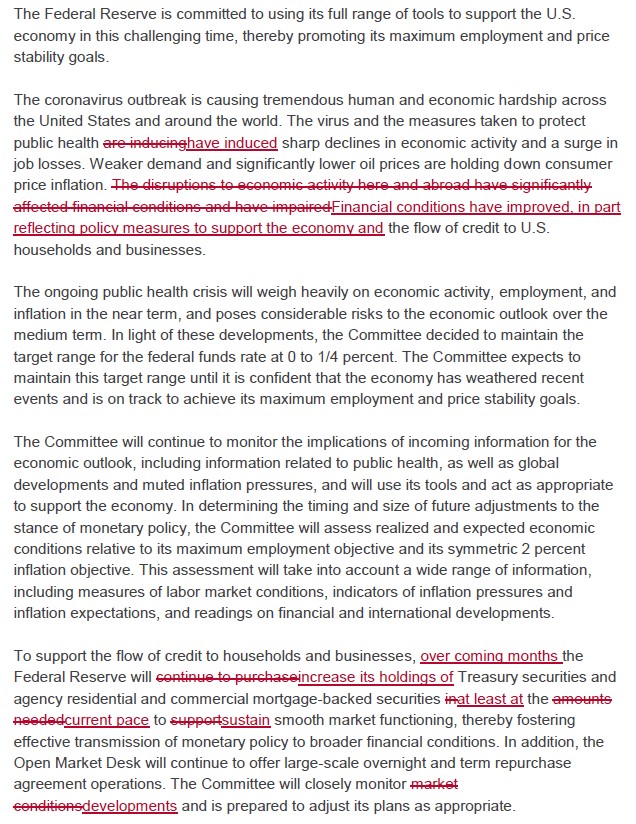

Now let’s review the changes to the June Fed statement. Fed stated financial conditions have improved because of its supportive policy responses as the image below shows. That was a stark change from saying disruptions to activity have affected financial conditions and the flow of credit to US households and firms. And Fed is taking some credit for the improvement in financial conditions. For the first time ever, the Fed was directly involved in improving conditions as it bought corporate bonds which allowed firms to issue debt.

It was an interesting sight because just when money managers were calling on firms to payback debt, they were issuing record amounts. To be fair, this was the smart thing to do because liquidity is more important than ever as business can be shut down for a few weeks. On the other side, long term debt is less important because rates are so low. Junk bond yields spiked, but even they have come down. Most firms would have been stupid not to take out the available money on their line of credit.

Bottom paragraph shows the other changes. Fed said it will support the flow of credit to households and firms over the coming months by increasing its holdings of treasuries and agency residential and commercial mortgage backed securities at least at the current pace to sustain market functioning. Fed is saying even in the best case scenario, it will maintain this level of QE for the nest few months. So the Fed is pulling out all the stops to keep the economy going.

Fed Guidance

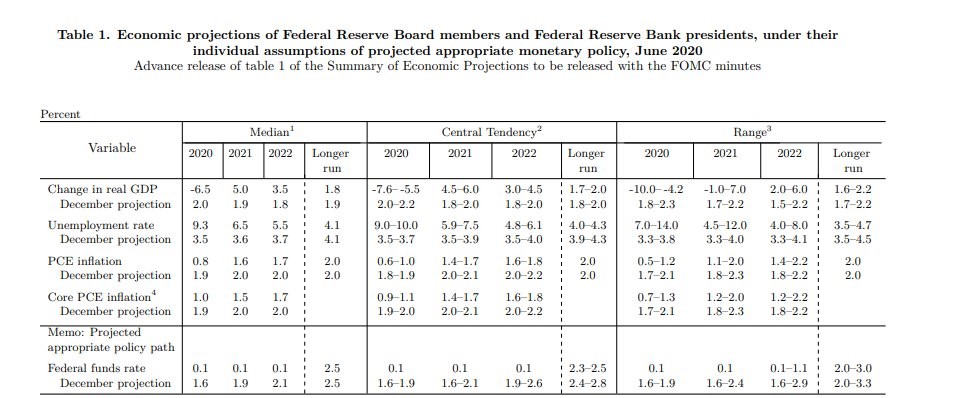

The table below shows the Fed’s forecasts for the next couple years. Again, the Fed plans to keep rates at 0. It still thinks the long run rate is 2.5%. That can change if inflation spikes. Inflation has been low for so long that it’s tough to imagine a new regime. If inflation doesn’t increase with all this monetary and fiscal stimulus, that further supports the thesis that it won’t increase in the long term. We just had a 3.5% unemployment rate and inflation was still low.

As you can see, the Fed sees GDP falling 6.5% in 2020 and rising 5% and 3.5% in the following 2 years. Fed lowered the long run growth rate by a tick to 1.8%. Frankly, many don’t get why the long run rate should be lowered just because of a quick recession. Cyclical slowdowns don’t have any impact on the long term rate. This was an exogenous impact which is even less impactful than cyclical changes to the long term.

Unemployment rate is expected to be 9.3% in 2020. You have to calculate the average this year because it was so volatile. Average rate this year is 7.9%. While the rate will come down in the rest of the year, the average will be higher because the first 3 months suppressed the current average.

Implication is that the Fed thinks the unemployment rate is going to average 10.3% in the next 7 months. That is far too bearish. It might even fall below 10.3% by July. It will likely average between 8% and 9% in the following 7 months. Fed sees the unemployment rate falling to 6.5% in 2021. I won’t predict anything that far out. It’s too uncertain.

Inflation is low even with all this stimulus. That’s because demand is weak. Fed’s estimate for headline PCE inflation in 2020 is 0.8% and its core PCE estimate is 1%. That explains why the Fed isn’t close to hiking rates.

Powell Quotes

Let’s look at Powell’s statements from his presser. He said the economic projections were made with the “general expectation of an economic recovery beginning in the second half of this year and lasting over the next couple of years, supported by interest rates that remain at their current level near zero.”

That obviously true because the unemployment rate is currently higher than the projected average for the year. If it were to stay at 13.3%, the average would be higher than 9.3% for the year.

Fed’s dot plot shows all Fed members think rates will stay at 0% in 2021 and 2 think rates will rise in 2022. It’s very tough to forecast where rates will be in 2022. The entire purpose of the dot plot is to affect current markets, not predict the future.