Fed Ignores Inflation - Mixed June PPI Report

It's an interesting market mix as Fed Ignores Inflation and the Labor Market Reports. Headline PPI inflation was 0.1% monthly. It met estimates and was the same as May.

On a yearly basis, it was 1.7% which met estimates and fell from 1.8%. Inflation readings that include energy have been weak this year. Excluding food and energy monthly PPI was 0.3%. It beat estimates for 0.2% and May’s reading of 0.2%.

Similarly, yearly core PPI was 2.3% which beat estimates for 2.2% and was the same as May’s reading. Trade services had a positive effect on inflation. So core inflation without trade services was 0% monthly. It missed estimates for 0.2% and May’s reading of 0.4%. Yearly it was 2.1% and fell from 2.3% which was also the consensus.

Energy was a big weak point just like in the CPI report as prices fell 3.1% monthly. Finished goods PPI fell 0.4% and computers fell 0.8%. On the positive side, food and total services were up 0.6% and 0.4%.

Trade services were up 1.3%. That reverses the past 2 months of declines. That's good for retailers and wholesalers. Core personal consumption was up 0.5%. Meaning core PCE should be relatively strong when it’s released on July 30th.

Core PCE To Increase To 1.7%

Fed Ignores Inflation - As you can see from the chart below, the estimate of core PCE based on inputs from CPI and PPI show it will be 1.66% on a yearly basis.

This prediction is very highly correlated with actual results as the grey line shows. Just as the Fed seems to have given up on inflation increasing to its target, inflation is rising.

Core PCE is very likely to be below 2% for the rest of the year. But this still shows how the Fed seems to be ignoring its mandates one of which is to keep prices stable.

Tariffs, the tight labor market, and now the easy Fed will all put upside pressure on inflation. I still don’t see inflation being an issue.

If inflation were to creep up in the next few months, the market might get skittish and project either fewer rate cuts. I can’t see the Fed going along with those fears if the economy continues to be weak. If the economy strengthens, obviously there’s room for a more hawkish Fed.

Fed Ignores Inflation - Focused On The Business Cycle

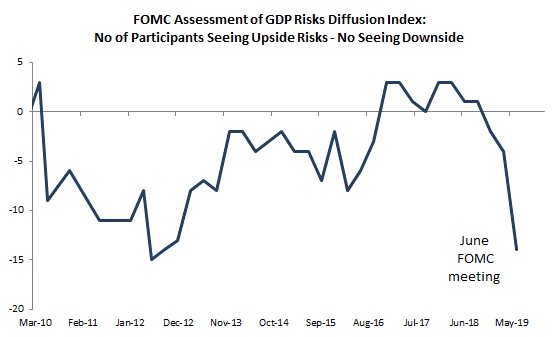

In my opinion, the Fed following the economic cycle makes more sense than just looking at the labor market and inflation. Fed can get out ahead of weakness if it uses other indicators. In tune with my point that the Fed’s new goal is to keep the economic cycle going at all costs is the chart below.

As you can see, the Fed is reacting to the risks it sees which are now to the downside. Fed is getting out ahead of those risks. Even though there is no sign of a recession, the labor market is solid, and inflation is similar to where it has been for the past few years.

This chart signals the Fed will be very dovish

Fed Ignores Inflation - Especially as the net number of Fed members that see downside risks to the economy is the lowest since 2012. There aren’t many economic indicators that suggest the economy is in worse shape than 2015-2016. But the Fed is more bearish.

The fact that that the Fed was very bearish in 2012 seems to suggest it is putting a high weight on global economic weakness. Especially since the weakness in 2012 was centered in Europe.

The market loves the Fed’s new focus. It seems to be putting a lot of faith in policy makers. This market thinks if the economy really starts to weaken, Trump will make a trade deal with China and the Fed will cut rates quickly.

Will that be enough to stave off cyclical weakness? It depends on the severity of the downturn and what’s causing it. If the weakness is caused by uncertainty related to trade, a trade deal will definitely help.

Fed Ignores Inflation - Leading Index’s Growth Rate Improves

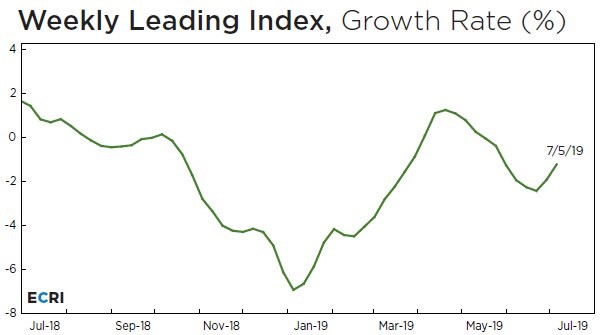

ECRI weekly leading index increased 1 point to 146.2. That increase caused the growth rate to go up from -1.9% to -1.2%.

As you can see from the chart below, the growth rate is much higher than the recent bottom of -2.4% 2 weeks ago. This index’s growth rate has plenty of runway to improve in late July and early August because of the easier comps.

The past 2.5 months of data suggests economic growth in the 1st half of 2020 should be near the long term trend. This indicator correctly predicted the economic weakness in Q2 all the way back in December and January.

You can say the stock market did as well. I am looking forward to next week’s coincident indicator. Specifically to see if growth in June is close to the trough in 2016.

Growth troughed at about 1% then and it was 2% in May. If growth goes below 0%, it’s a clear sign the economy is in a recession. I expect it to fall to about 1.6% in June.

GDP Estimates

Fed Ignores Inflation - This week was a very quiet one for economic data as only 3 reports effected the NY Fed’s GDP Nowcast. Its estimate rose 1 basis point to 1.49%.

Nowcast for Q3 rose 1 basis point to 1.75%. I consider that Q3 growth rate to be solid since I have very low expectations for Q2 and Q3. I have had these expectations since the ECRI readings came out in January.

Even the St. Louis Fed’s estimate isn’t that strong. Which is unusual because it tends to be optimistic. It expects 2.78% growth. If that growth rate is reached, I would be shocked. I expect growth to be between 1.4% and 1.7%.

Median of 11 estimates in the CNBC rapid recap has GDP growth coming in at 1.5%. Average estimate is 1.7%. These aren’t recessionary numbers, but they signal there is a slowdown.

This is near what growth would have been in Q1 if it wasn’t propped up by inventory investment and net exports.