Fed Raises Rates In A Hawkish Hike

As expected, the Fed raised interest rates by 25 basis points. In my opinion, the hike was hawkish because the Fed was one vote away from switching its expectations to 4 hikes this year instead of 3. My expectations have been slightly more dovish than the street because I was thinking there would be 2 or 3 hikes this year. Heading into the meeting, the market anticipated 3 or 4 hikes. Therefore, this decision didn’t really catch the market by surprise. It was a modestly hawkish meeting with an improved growth outlook. Investors can look at this positively by saying the Fed is expecting faster growth or negatively by saying the Fed is hiking too fast.

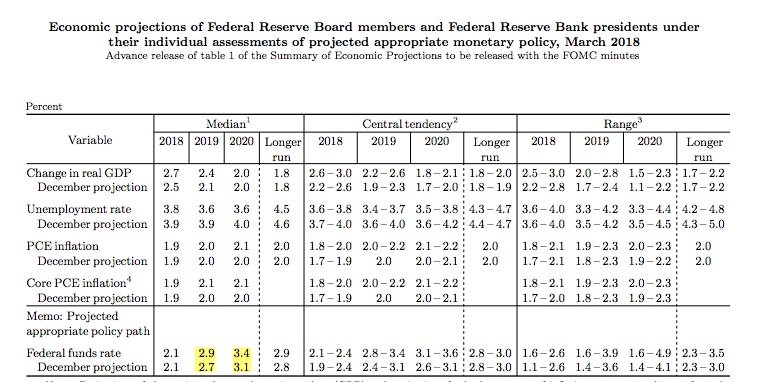

Ultimately, one hike either way isn’t going to be the difference between a recession and strong growth. However, that wasn’t the only change to forward guidance. As you can see from the table below, the Fed increased the projection for the Fed funds rate from 2.7% to 2.9% in 2019 and from 3.1% to 3.4% in 2020. The Fed often is completely at odds with its projections from a few years prior, so don’t take this to mean those rates hikes will certainly happen. I expect the economy to weaken by 2020 meaning there might not be any hikes that year. Powell stated the Fed is watching the yield curve. He didn’t dismiss it. My expectation is that the Fed will start to focus on it more when it comes close to inverting. It’s not close yet; rather, it’s close to being close.

Bullish Powell Pushes Up Median GDP Estimate

The table above also shows the other changes to the Fed’s expectations. As you can see, the projection for 2018 GDP growth moved up from 2.5% to 2.7%. The Fed sees economic momentum, but recognizes that the tariffs could stymie growth. Last year, I thought the growth expectations were slightly too low throughout the year. This year, I think the expectations are too high. Once the Q1 GDP growth comes in below the 2.7% estimate, it will be tough to reach 2.7% for the full year. I think the Fed is biased towards looking at its own reports instead of hard data. That’s a mistake because the regional Fed data has been far too optimistic on inflation and the overall economy. The only place where the hard and soft data are meeting is the manufacturing sector.

The estimate for 2019 GDP growth also increased from 2.1% to 2.4%. This is consistent with the narrative I’ve seen out of other government agencies which suggest the tax cuts will boost growth this year and next year and then taper off, having no effect in the remaining years of the cuts. So far, we’ve seen more of a boost to GDP from the hurricanes last year than the tax cuts this year. That’s based on the facts we have now. I will update my opinion if the Q1 GDP report is a positive surprise. It will be released on April 27th.

Inflation Estimate Virtually Unchanged, Unemployment Estimate Falls

I think this Fed meeting supports the narrative that Powell was bullish on growth at the Congressional testimony, but not that hawkish. That’s a very nuanced and almost contradictory opinion because if you expect growth and inflation to be strong, you should want to hike rates. However, it can work if the Fed thinks the labor market has room to grow before wage inflation kicks in.

As you can see from the table, the estimate for inflation barley changed at all, but the estimate for the unemployment rate fell from 3.9% to 3.8% in 2018, from 3.9% to 3.6% in 2019, and from 4.0% to 3.6% in 2020. I disagree with this expectation, but I agree with the motivation behind it. The motivation is that the labor market isn’t at full employment and probably won’t get there for the next year or two. The reason I disagree with the forecast is because I think the labor participation rate will increase and the unemployment rate will stay stagnant. If the unemployment rate was correctly measuring the labor market, the labor market would be more than full since the rate is at 4.1% and projected to fall to 3.6%, while the long run estimate is for 4.5% unemployment.

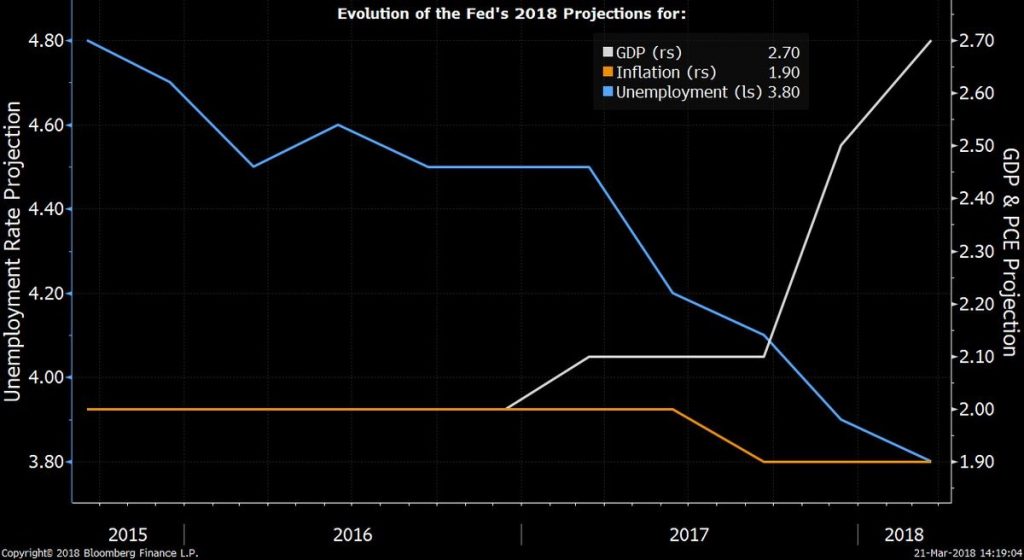

Historical Fed Estimates Have Vacillated A Lot

The chart below shows the Fed’s 2018 estimates for GDP growth, inflation, and the unemployment rate. The GDP growth estimate increased since mid-2017 when the economy started to gain momentum and it became clear that the Congress would likely pass a tax cut. The estimate for inflation decreased slightly in the middle of 2017 when the inflation fell. It’s interesting to see that Yellen claimed the 2017 disinflation was temporary, but the 2018 estimate for inflation is very close to what we saw last year. The big increase, if you even call it that, was when inflation bottomed in the summer of 2017 and moved slightly higher in the fall. The Fed agrees with the inflation data from February which showed the inflation rate will stay stagnant. This was unlike the January reports which indicated accelerated inflation. The unemployment estimate fell as the Fed now expects the rate to fall below the long run rate.

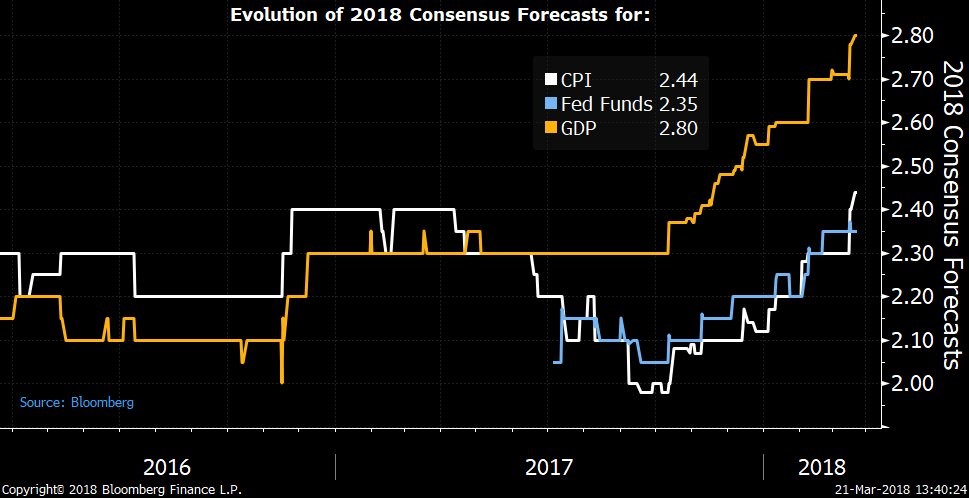

Consensus Follows The Fed’s Estimates

The chart below shows the changes in the consensus forecasts for CPI, the Fed funds rate, and GDP growth. The consensus is almost in lockstep with the Fed on GDP growth. The Fed pushed up estimates slightly before the consensus. The CPI estimate is overzealous in my opinion. Keep in mind, it’s similar to what the Fed has because CPI is usually a few tenths of a point above the PCE. The Fed funds rate is expected to be higher than the Fed’s median guidance, but the Fed can easily change that if the economy heats up because only one voting member needs to change his or her position for there to be 4 hikes in 2018.