My prediction for Fed policy was wrong. As a reminder, I was looking for a dovish hike based on the latest disinflation, but instead the Fed didn’t deviate much from its policy. There was a stark difference between reality and what the Fed spoke about today as the core CPI and the headline CPI missed expectations, yet the Fed was hawkish. I will review those reports later in this article.

The Fed maintained its guidance for one more rate hike by the end of the year, saying the causes of the latest bout of disinflation were temporary. Specifically, Yellen said "The recent lower reading on inflation have been driven significantly by what appears to be one-off reductions in certain categories of prices such as wireless telephone services and prescriptions drugs." While I have highlighted the dramatic decline in telecom services inflation, I would’ve thought Yellen would give specific reasons why this trend won’t last, if she was going to make policy decisions based on it. I’m shocked to see telecom services being blamed for the hawkish policy.

Despite the Fed saying the inflation risk is transitory, it cut its forecasts for inflation. The headline PCE inflation estimate for 2017 was cut from 1.9% to 1.6% and the core inflation estimate was cut from 1.9% to 1.7%. This is the broad definition of transitory which I discussed in a previous article. If a year is transitory, then technically any change in markets is transitory. You can say the bull market in treasuries which has lasted decades is transitory because it will eventually end. The forecast for 2018 and 2019 inflation for both indicators stayed at 2.0%. From my perspective, estimates for inflation 1.5 years in advance are meaningless because there’s little data to base it on. Even though inflation for this year missed the Fed’s estimate, the Fed is basing its entire monetary policy outlook on its next guess.

The Fed and the ECB have been dealt a similar hand. Both America and Europe are seeing decent growth and low inflation. Even though the European economy is slightly stronger, the ECB acted dovishly and the Fed acted hawkishly. The Fed’s 2018 average estimate was unchanged, seeing rates at 2.125%; 2019 estimates increased slightly from 2.938% to 3.000%. The Fed decided to blame GDP growth accelerating for the hawkishness. This makes no sense to me because it doesn’t take much to accelerate from 1.2%. By the way, the Fed didn’t predict the economy would be so weak in Q1. Essentially, it’s ignoring that faulty estimate.

The Fed raised its 2017 GDP forecast to 2.2% from 2.1%. I don’t see that forecast as being obviously incorrect. However, I question why the Fed is raising estimates for GDP growth since the chance of fiscal policy stimulus affecting the 2017 economy is nil. The changes to its viewpoint on the economy were that it sees the economy growing moderately instead of slowing. I don’t agree with the Fed basing its positive outlook on the 2017 economy on forecasts for Q2 GDP growth. As I have said, Q2 growth will be higher than Q1 growth, however, there will be a headwind from auto sales weakening for the rest of the year. On the labor market, the Fed said job gains have moderated. This is inconsistent with policy because the Fed’s entire point on why inflation will increase is because of the tight labor market.

Wage growth of 3.5%, according to the 3-month rolling average the Atlanta Fed calculates, doesn’t add up with how tight the jobless claims and unemployment report show the labor market is. On unemployment, the Fed changed its 2017 forecast from 4.5% to 4.3%. Objectively the unemployment rate is broken in terms of forecasting wage inflation, but the Fed keeps using it. I think there needs to be a catalyst to accelerate wage inflation, but the Fed thinks the same labor market will eventually cause more inflation. Two tenths of one percent change in the unemployment rate isn’t the size of a catalyst necessary to move inflation.

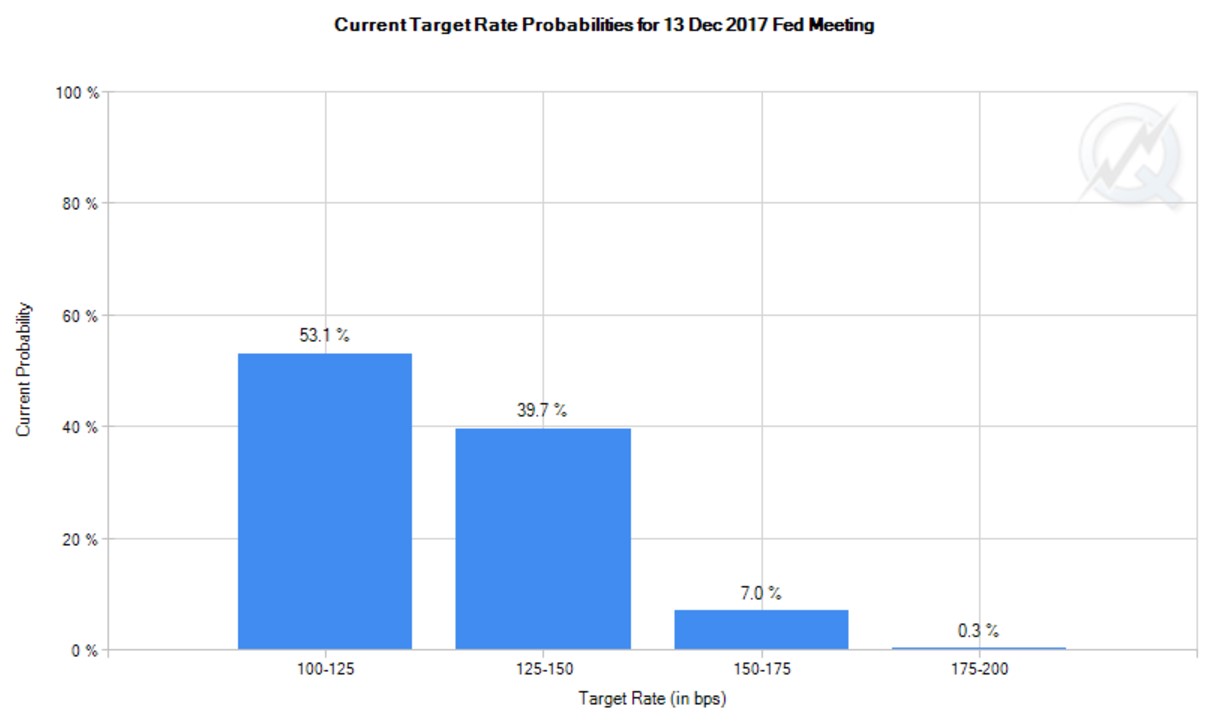

Looking at the probabilities of a rate hike by December, there is now a 47% chance of a rate hike this year. This is low considering that it’s part of the Fed’s guidance. The Fed has increased its credibility on rate hikes as it takes a ‘by any means necessary’ approach to policy. If the Fed raises rates in December, the market will need to adjust, meaning stocks may fall, short-term yields may rise, and long-term yields may fall. The market thinks the Fed will follow the inflation data, but it just ignored the data staring it in the face, so the market may be wrong.

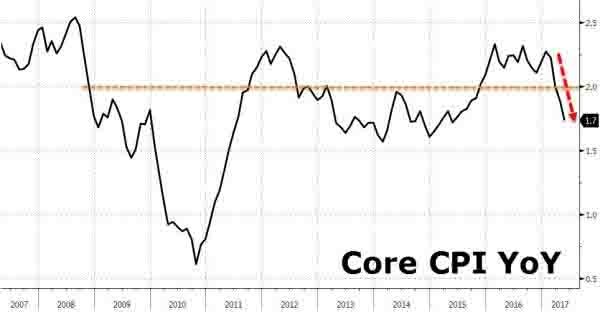

The May CPI report was released Wednesday, as I have mentioned. The chart below shows that core CPI growth fell to 1.7% which was below expectations for 1.9% year over year growth. The headline CPI number also missed expectations as it came in at 1.9% growth year over year compared to estimates for 2.2% growth. May inflation falling might be the tip of the iceberg because oil prices crashed on Wednesday. WTI fell 3.7% to $44.73 which is the lowest close since November 14th. The crash was caused by the latest EIA data. Gasoline inventories were up 2.1 million barrels which is a higher glut than the estimates for a 0.5 million draw down. Crude inventories fell 1.7 million barrels which was a lower draw than the 2.7 million barrels draw down expected. I have been calling for a decline in oil prices all year. Finally, we are seeing this play out. It will hurt S&P 500 bottom up earnings in the 2nd half and pinch the headline CPI report in June. This will make the Fed look bad for raising rates.

On the other hand, core PPI inflation increased to 2.1% which is the highest rate since May 2017. This report is less important to the Fed than the CPI and is different from most of the regional Fed reports I have reviewed.