Facebook Falls 20.23% After Hours

Facebook stock had a massive crash after hours after it reported weak guidance and had a bad conference call. Facebook had rallied to new highs despite the Cambridge Analytica scandal. That was given back in a matter of minutes as the stock fell 20.23% to $173.5 from $217.5. The size of the decline in Thursday’s trading session could be historic because the company has such a large market cap. After hours it lost $130 billion in market cap which is the size of about 4 Twitters. While other big cap tech names haven’t been able to move the Nasdaq, this decline surely will even if it regains some of its losses during the day. Facebook’s reports sometimes disappoint investors because it has high implied expectations. This will probably be the biggest disappointment.

Headline Metrics

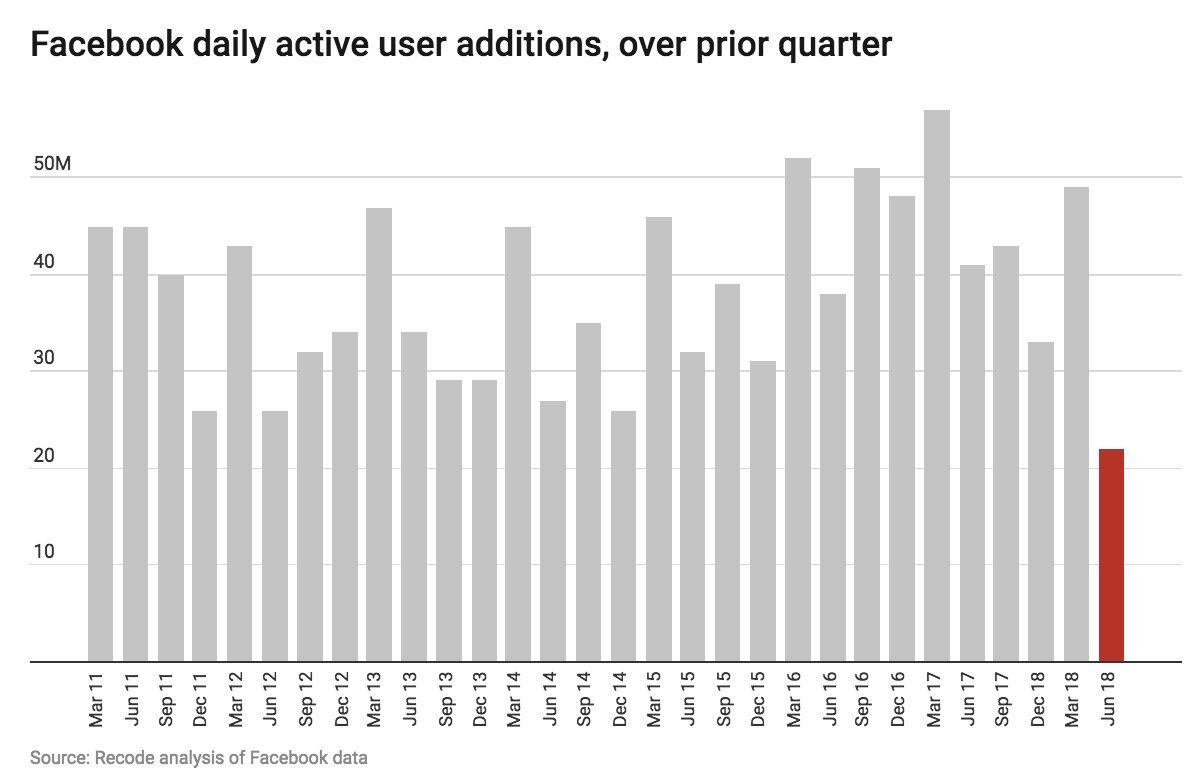

Earnings per share were $1.74 which beat estimates by 2 cents. Revenues were $13.23 billion which missed estimates for $13.36 billion. Global daily active users were 1.47 billion which missed estimates by 20 million. It’s very rare for Facebook to miss estimates on global user growth because international markets still aren’t as saturated as America. As you can see in the chart below, user additions over last quarter are the lowest since at least Q1 2011. Mark Zuckerberg claimed the negative press wasn’t hurting North American user growth, but GDPR came out of left field and is hurting European user growth.

North American daily active users were 185 million which missed estimates for 185.4 million. North American users are monetized at the highest rate which means Facebook needs to add many more users from emerging markets to keep up its growth rate. Average revenue per user was $5.97 which beat estimates for $5.95. It’s easy to increase the number of ads on the service, especially in video because so many advertisers want to spend money on the platform.

Ads Cause Users To Leave Social Networks

A problem arises when users hate the ads so much that they leave the platform. One thesis that some have is that the main reason new platforms keep gaining steam is that the old ones have ads and the new ones start with no ads. It’s like advertisers are chasing users around the internet. That’s bad news for Facebook because it means there will be new apps which steal users’ attention in the future. It means each platform diminishes over time.

Europe Sees A Drop In Daily Active Users

If you thought the flat North America user growth was bad, you’ll be very disappointed with the European growth. European daily active users were 279 million which missed estimates for 279.4 million. This is a decline from last quarter which had about 282 million. Facebook is reaching the maturation point Twitter hit a couple years ago. Now only monetization, Instagram, and WhatsApp can save the company. Those are great assets to fall back on. The company is far from being in a tailspin. The problem is profit growth could decelerate.

Overall Company Review

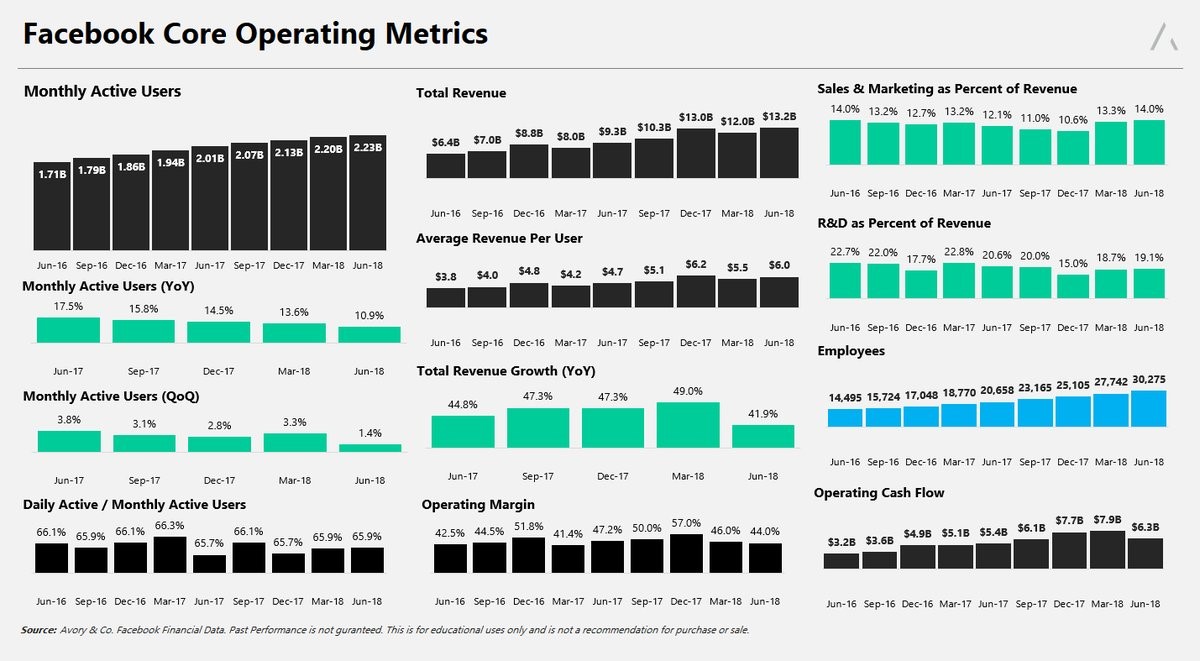

The charts below show an overall review of the firm’s metrics. As you can see, revenue growth fell 7.1% from last quarter and operating margins fell from 47.2% in the June 2017 quarter to 44% this quarter. Monthly active user growth was only 10.9% year over year and 1.4% quarter over quarter. The company is fast approaching a brick wall in terms of user growth. Revenue per user went from about $4.7 in Q2 2017 to $6 this quarter. This drove revenue growth more than the increase in users, meaning ARPU improvements are already a bigger deal than DAU growth. The number of employees continues to soar as the company tries to police content on its site with human workers instead of algorithms, bots, and user reports.

Is Facebook Shrinking?

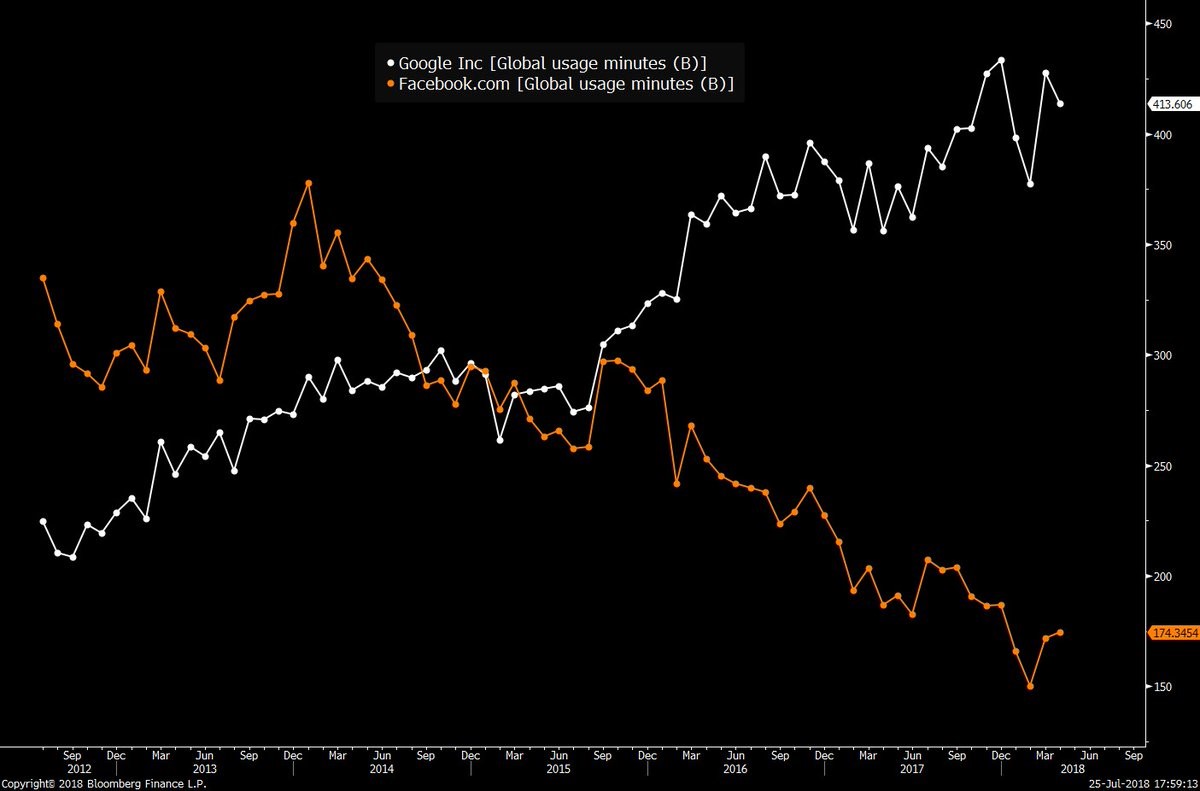

You will see charts which mostly go from the bottom left to the top right on Facebook’s investor relations page, but it might not be all smooth sailing for the company. In other words, there have been cracks under the surface before this quarter. As you can see from the chart below, Google is beating Facebook.com in global usage minutes as Facebook has been in decline since 2013, while Google has been increasing usage since 2012.

GDPR Hurts European Business

Even though Facebook has 2.5 billion people using its network of apps, a small slip up in Europe caused the stock to crater, showing us how the stock was priced for perfection and how reliant it still is on its main app even though rapid growth is coming from WhatsApp and Instagram. User growth came from Indonesia and the Philippines which have low ARPU, while the high ARPU European market was hurt by GDPR. GDPR gives European internet users more control of their online data. GDPR didn’t have a huge impact on Facebook’s business in Q2, but it caused the company to be more pessimistic on future quarters because it wasn’t fully implemented in Q2. A growth company missing on forward guidance is deadly for its stock. Advertising revenue projections were $13.04 billion which missed estimates for $13.16 billion. For a company which usually beats estimates, the business momentum has been lost.

Takeaway

It’s easy to bash the stock because these numbers weren’t as good as what we are used to, but stock being down over 20% certainly changes the situation. The company is at a fork in the road as its main app is dying while its smaller apps are growing quickly. If you don’t think Facebook will be able to monetize its Instagram users as well as its main app users, you should avoid the stock. The IGTV experiment is a big bet for the company. If it can create a viable competitor to YouTube, the stock is a buy. Personally, I would avoid the name because I like Alphabet and Microsoft better. If Facebook has a bad run, it can be a big drag on the overall market. Losing leaders is bad for a bull market if they aren’t replaced.