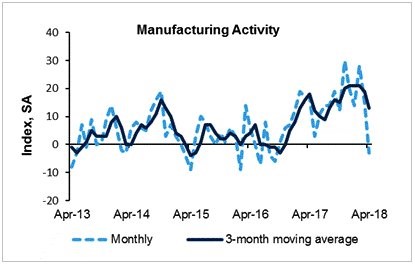

Richmond Fed Survey Shows Weakness

Manufacturing has apparently weakened in April as growth has peaked. The levels seen earlier this year have historically not been maintained. It’s certainly possible that manufacturing could reach a permanently high plateau, but that’s not something I’d bet on. We’ve seen some conflicting stats from the Philly Fed and Empire State index, so the Richmond Fed report from Tuesday can be thought of as a tie breaker. I’ll also be discussing the Kansas City Fed report in a subsequent post.

As you can see from the chart below, the April Richmond Fed report was terrible as the index fell 3 points which ended a 17 month streak of positivity. The consensus range was 14-20 and the average estimate was 16. The prior report was 15. Shipments had a 23 point decline to -8. In the past two months, it has gone down 39 points. You can see, February marked a peak in the 3 month moving average of this survey. The volume of new orders fell from 17 to -9. The local business conditions index was 29 in February and now is -1.

It’s possible that this data is a temporary vacillation, but because I am seeing global weakness in manufacturing, I don’t think that’s likely. One good part of the report is the capex index increased from 16 to 31. However, the inventories were up for finished goods, dampening hope. Like most other reports, wages were up and prices paid were up. The perception of increases to prices paid on an annual rate was up from 2.39% to 2.43%. The expectations fell 7 basis points to 2.52%. The prices received index was the reverse as it fell 8 basis points to 1.46% and the expectations rose 7 basis points.

Facebook Reports Blowout Earnings

Facebook beat earnings estimates just like Twitter, showing that social media has far from peaked in terms of profitability. User growth rates and engagement won’t improve like they have in the past, but ad rates became more expensive, boosting Facebook’s EPS. Some have suggested Facebook may not have wanted to be so profitable because the regulators are on the firm’s back. To me, that seems silly because Facebook is in hot water over data collection not over being a monopoly. Furthermore, a vacillation in EPS of few cents wouldn’t make Congress more or less likely to go after the company. Headlines which unveil another issue with data collection and privacy would motivate regulators.

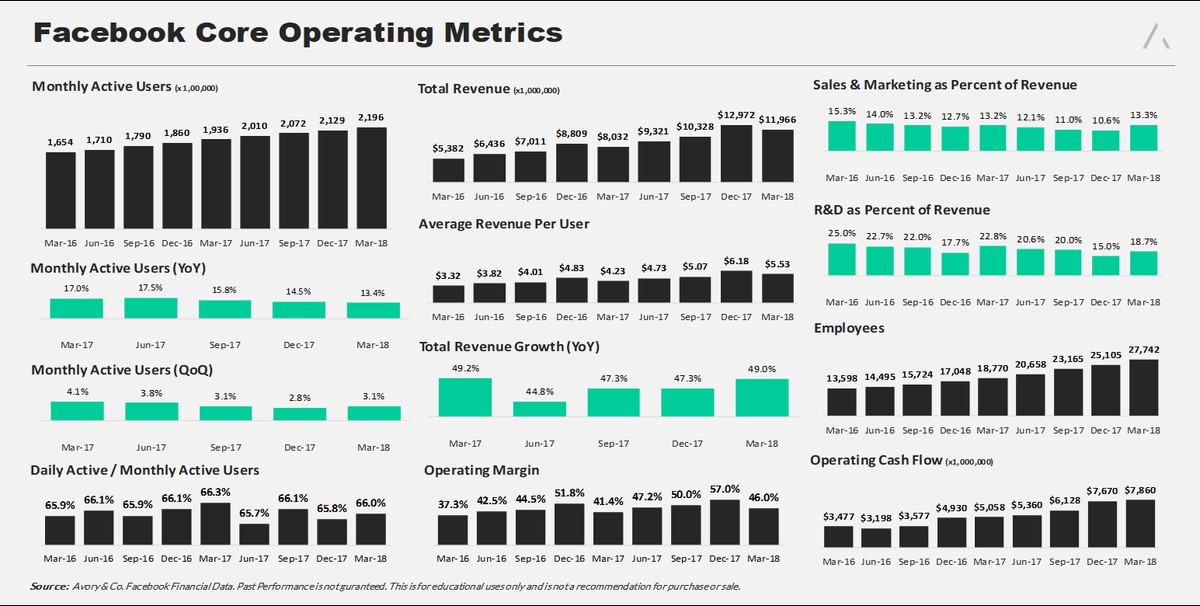

I think it was very important for Facebook to produce great numbers because it reminds investors why they own the name. It dominates the time people spend on the internet which is extremely valuable. Clearly, the ads are very valuable because average revenue per user was $5.53 which was up from $4.23 in the same quarter last year. The firm delivered in every possible way with this great report; it sent the stock up 10% on Thursday.

Adjusted EPS was $1.69 which beat estimates for $1.35. That’s 62.5% growth from last year. Revenues were $11.97 billion which beat estimates for $11.4 billion. As you can see from the charts above, the monthly active users were 2.2 billion and the daily active users were 1.45 billion. Both saw decelerating growth and met expectations. The key for Facebook is keeping users engaged rather than just building up the user total. There aren’t many internet users without a Facebook account. One of the most amazing parts of this quarter is R&D expense as a percent of revenue was down 4.1% from last year and sales as a percent of revenue was up only 0.1%. The total employees were 27,742 which was a 47.8% increase from last year.

Profitability and revenues are growing so quickly that the firm is still outgrowing the employee count which is supposed to be increasing because of safety and privacy concerns. It’s tough to grapple with how profitable this juggernaut would be without this recent surge in hiring. Specifically, the firm doubled its site operations workforce to 14,000. Even though Facebook is spending more money on lobbying and hiring more workers to secure the platform, it still was able to deliver more profits than Wall Street expected.

The new hiring makes the platform more sustainable which is important because some view social media apps as faddish. The company also made changes to improve quality of engagement which reduced time spent by 50 million hours which is 5%. It’s debatable if the firm is simply losing people’s attention or if it really did make changes which limited time on the platform. I believe Facebook’s claim because the firm has recently become more aggressive towards spam and offensive content. Temporarily banning users limits hate speech and spam which is good for the platform in the long run. The hope for the firm is the users which aren’t ‘bots’ who post this low quality content learn what is ok and start using the platform in a safer way.

Despite the stories about how people were deleting Facebook, there wasn’t a meaningful impact on total users which is what Mark Zuckerberg mentioned in his Congressional testimony. The guidance included Capex of $15 billion for the year which was at the high end of expectations. Expenses are expected to go up 50% to 60% which would be an acceleration from the current growth rate. The money will be spent on safety investments, content acquisition, and long term innovation. The uncertainty of how much the safety investments would cost and how many users left the platform have dissipated. To be clear, if another negative headline about the firm’s practices surfaces, the stock will crater again. That’s the biggest risk besides regulation. Finally, Facebook added another $9 billion to its buyback after initiating a $6 billion one last year. If the stock craters again, the firm will be in the public market supporting its shares. Obviously, with the great numbers from Wednesday, that won’t be happening soon.