Another Big Factor Day

There have been a few days where tech has underperformed in this recovery from the early September correction. Tuesday was different as the speculative tech stocks had a great day. Nasdaq was up 1.2%, while the S&P 500 was up 0.5%. Russell 2000 was only up 8 basis points. Most stocks were mixed outside of the Nasdaq.

Penn National Gaming was up 4.1% as it is launching its betting app this Friday. The stock is up 27.8% in the past month and 699% in the past 6 months. That’s not a typo. That stock has been on fire. It's like the euphoria about marijuana stocks as retail traders are piling in with reckless abandon.

It's unlikely that sports betting will be a profitable business for Penn Gaming as Draftkings and FanDuel are spending a lot of money in advertising. Remember, Penn invested in Barstool Sports which it’s using to market its betting app. These stocks will all crash when reality hits just like how the marijuana stocks have fallen in the past 1.5 years. Ever since peaking in February 2019, Cronos stock is down 75%. Cronos rallied well over 1,000% prior to the peak.

Apple’s announcement didn’t impress investors as they are more concerned with the new iPhones than iPads and the Apple Watch. A flat day on such an announcement is a negative in this uber bullish environment. It was a s disastrous day for the banks as Citigroup fell 7%.

It took down the rest of the industry as JP Morgan fell 3.1% and the regional bank index fell 1.9%. Citi’s credit card delinquency rate fell 10 basis points to 1.43%, but its net charge off rate increased 33 basis points to 2.75% in August. That’s far from a disaster as it was 2.62% last year.

Tesla stock rose 7.2% on no news which is apparently a normal thing that we are supposed to accept. The stock is up 36.2% in its 5 day winning streak. There will likley be a double top as most have expected the stock to peak around a week before Battery Day when the hype peaks. Battery Day is in 6 days.

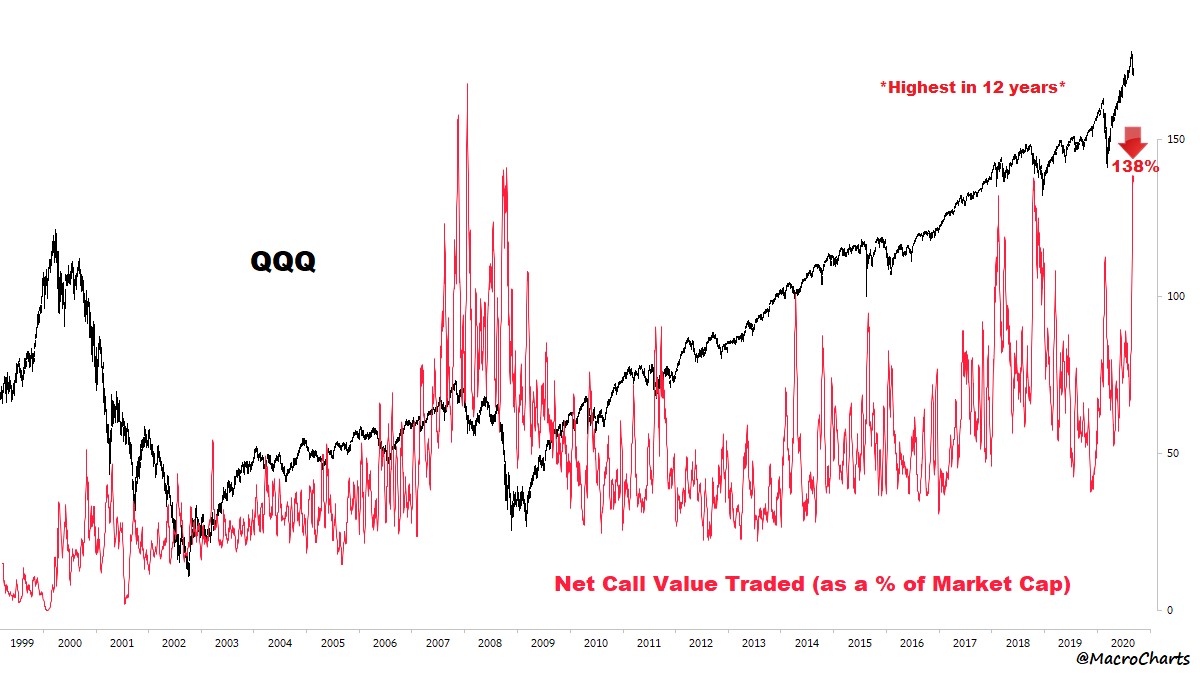

Speculators Are Still Here

A 10% decline in the Nasdaq in 3 days may have been a record, but it did little to stop the euphoric speculation in tech stocks. As you can see from the chart below, the net call value traded as a percentage of market cap in the Nasdaq 100 reached 138% which is the highest in 12 years.

This is nothing like the speculation in 1999 because options weren’t as prevalent then. This decline in momentum tech stocks will be swifter than the one in the early 2000s. Interestingly, despite the speculation in Tesla and the rally in the Nasdaq, the cloud index is still down 12% from its peak on September 1st. Number of stocks that are rallying is dwindling.

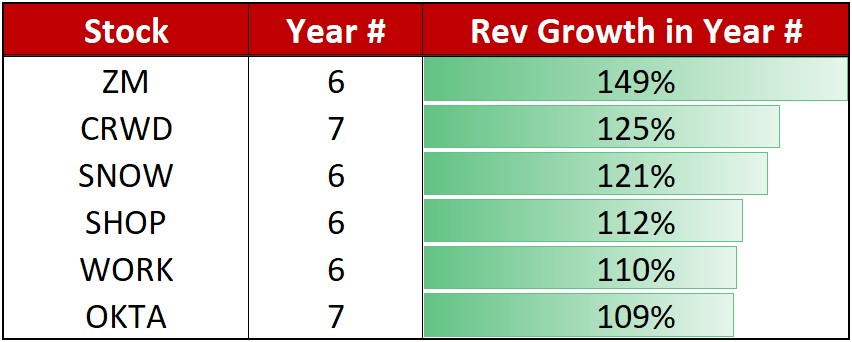

Snowflake To Make Good Use Of Speculation

Snowflake is doing its IPO at almost the perfect time as speculation for tech stocks is high. It’s possible that some investors sold their cloud stocks to buy this incredibly hot IPO. Snowflake’s IPO is like feeding meat to a starved alligator.

As you can see from the chart below, it has the 3rd fastest revenue growth out of the recent cloud IPOs. The company is set to receive a $33 billion valuation which is almost triple the $12.6 billion valuation it got in its private funding round earlier this year. No one cares that this company isn’t profitable. They love the track record of the CEO who previously took ServiceNow and Data Domain public, but this frenzy has gotten out of hand.

Fund Managers See Tech Frenzy

Fund managers agree that it’s a craze, but they need to perform well each year, so they need to buy into the mania. For 5 months in a row, long tech has been the most crowded trade.

An interesting aspect of this survey is that by receiving over 80% of the votes, this is the most crowded trade in the history of this survey. Unfortunately, we don’t have data from the late 1990s. Keep in mind, the limit is 100%. Above 80% is very high.

Fund managers are trying to move out of the growth stocks and into value, but oddly they sold the banks. This makes no sense because banks are the best value trade there is. As you can see from the chart below, value beat growth and small beat large caps.

Industrials received money, while the banks and tech positioning fell. This chart doesn’t include energy, but I would think they sold energy because it has done poorly. ExxonMobil is on an 11 day losing streak. If you’re not buying energy and banks, you’re not a value investor.

As you can see from the chart below, virtually every fund manager thinks tech is overvalued and virtually no one thinks the banks are overvalued. Net percentage saying tech is overvalued minus the percentage saying the banks are overvalued is so high the y axis shows 110 even though it’s not possible for this reading to get above 100%. Investors don’t want to take the first swing at buying the banks.

Conclusion

Many thought we might be done with days where the Nasdaq outperforms the small caps. But we had one more on Tuesday as Tesla powered the index higher. Cloud stocks are still down double digits from September 1st. Snowflake IPO could mark the beginning of the end of the euphoria in tech since it is adding new stock supply. There is only a certain amount of SaaS stock the market can handle before this bubble implodes.

Fund managers agree that tech is a bubble and they all think it’s overvalued in relation to the banks. Some tried to switch to cyclicals. But they didn’t buy energy or banks which is a major mistake no value investor should make.