Trump Vs. Powell Drama Ends Peacefully

On Friday, we got more clarification about President Trump’s statement on monetary policy in his interview on CNBC. Firstly, the President isn’t happy with the Fed’s plan to raise rates 2 more times this year. According to the Fed fund futures, there is a 62.3% chance of at least 2 more hikes this year. Trump’s fear is legitimate because the Fed is getting close to contractionary policy. The futures market hasn’t moved in response to Trump’s statements because the market feels these are opinions which won’t cause policy changes.

The market was proven correct since the White House stated, "He's not putting any pressure on them." To be clear, the President isn’t putting any pressure on the Fed. The White House added that the President realizes that Powell and several others are his appointees. An aide said "They're all his guys. It's his board." Furthermore, Larry Kudlow and Steve Mnuchin told the President that “The Fed is doing it right, let it happen. The sooner it happens, the sooner it will be over." The second point is correct since the more the Fed raises rates, the quicker the hiking cycle will be over. However, the President really shouldn’t wish for it to be over because historically the ends of hike cycles are followed by recessions.

Fed Making The Right Decision?

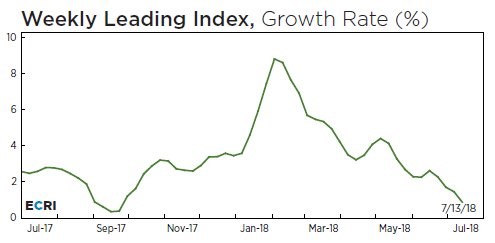

The Fed might not be making the right decision in hiking rates two more times this year. It’s debatable because I think year over year inflation will die down in the fall. Furthermore, there is some evidence that economic growth will slow sharply in the 2nd half, making rate hikes look like a big mistake. Clearly, the Fed isn’t on the same page as ECRI. As you can see from the firm’s leading index, a sharp slowdown like the slowdown after the hurricanes last fall, will occur in Q3 and Q4. The growth rate in the leading index has fallen to 0.9% as it shows no sign of perking up. The year over year comparisons aren’t even tough now as the index grew about 2.5% this time last year. The comparisons will get much tougher in the winter of 2019.

Dollar Index Falls On Trump’s Comments

The most interesting part of this kerfuffle between the President and Powell is that the President’s aides told him that the Fed will stop hiking rates when the Fed funds rate is around 2.5%. That’s much lower than the Fed’s target of 3.4%. Since the Fed funds rate is at 1.91%, the aides are telling the President that the Fed will raise rates 2-3 more times. I’m also expecting 3 more rate hikes, so I agree with their perspective. It’s tough to see the Fed funds rate getting to 3.4% because that’s above the 10 year yield which has been anchored below 3% for a few weeks.

The 10 year yield is agreeing with my point about inflation and the ECRI’s prediction that growth will slow. Keep in mind, a key cog in the growth slowing narrative will come out on July 30th with the release of the June PCE. If it shows consumption and income growth slowed, the ECRI will be vindicated because it has been showing the chart of those data points to support its leading index and its overall thesis that American growth will follow the rest of the world lower.

The final point in this drama is that the dollar weakened on Friday, possibly in response to the President’s statements. The dollar has been known to react to the President’s rhetoric. It was down 0.78% to $94.42. That’s a key movement technically because the dollar index made a new 52 week high on Thursday. This is a decent sized reversal from that point. It puts the index closer to a holding pattern than an uptrend since it is actually down slightly in the past month.

Earnings Growth Looks Amazing

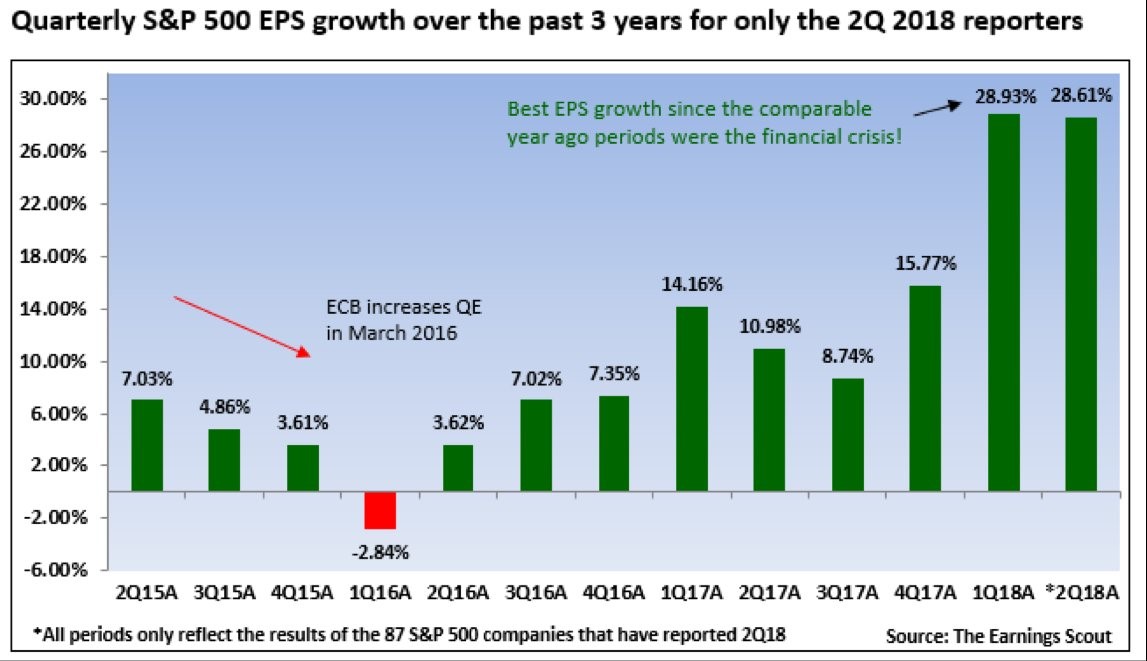

This earnings season is looking remarkable with this week’s reports in the books. Next week will have the most reports of this season as there will be 183 reports (3 of the FAANG names will be reporting results). As you can see from the chart below, the first 87 earnings reports this quarter have an average EPS growth rate of 28.61%. That is only 0.32% below the growth rate of the first 87 earnings reports in Q1. Not surprisingly, the EPS growth rate in Q1 has come down since the last update because it was way above the final growth rate.

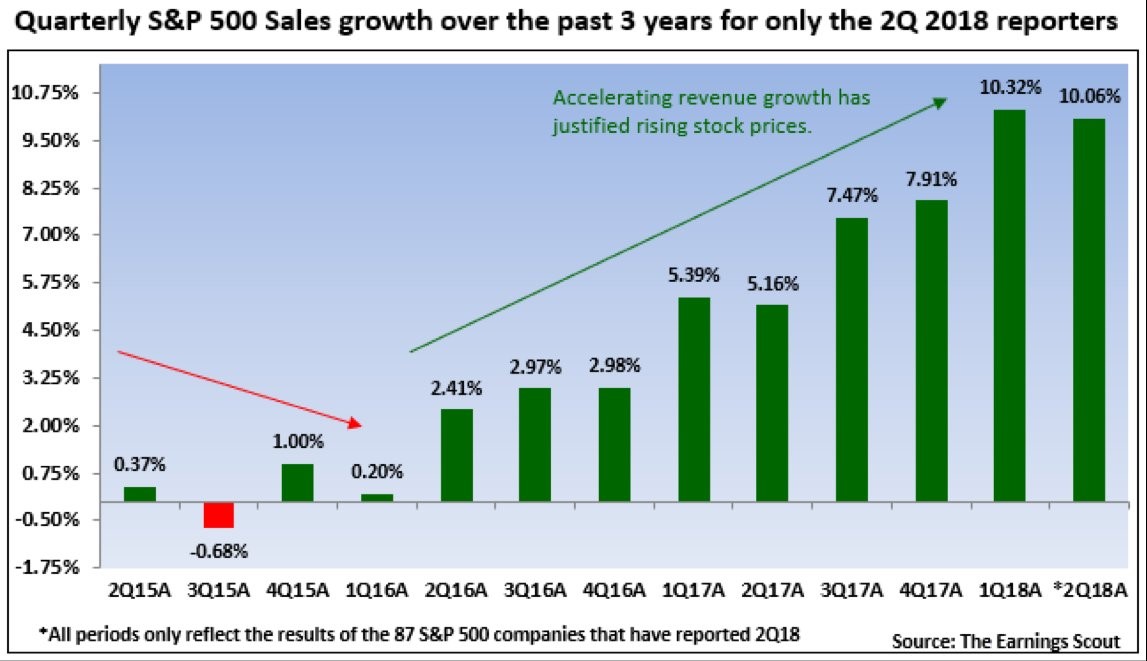

This quarter is coming close to challenging last quarter’s growth rate which means the beat rate is high and the EPS surprises are high. As you can see from the chart below, the sales growth rate is also doing well as the latest update shows it is at 10.06% which is just 0.26% below the growth rate in Q1 2018. This proves that EPS growth isn’t just from the tax cuts and buybacks. Tax cuts play the most important role in the high earnings growth, but that’s not the whole story. Either the economic momentum continued into 2018 or the tax cuts bolstered GDP growth. Either way, sales growth and EPS growth are a one two punch which will either power stocks higher or make them much cheaper.

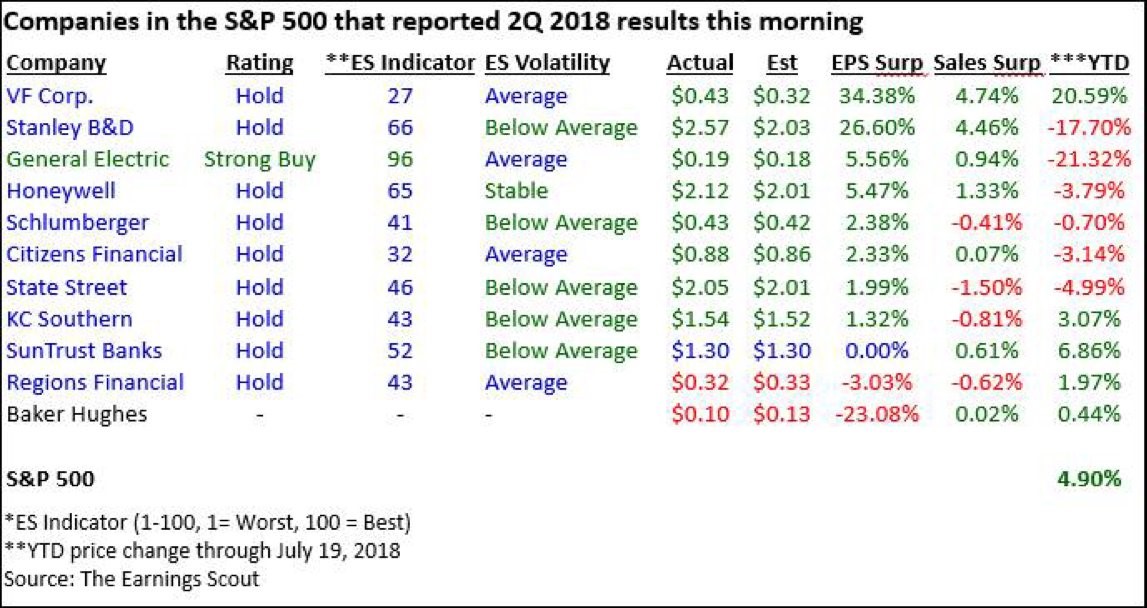

As I mentioned, the improvement in the overall growth rate in relation to Q1 means the recent beat rate must have been high and the EPS surprises must have been great as well. The table below lists the companies that reported on Friday morning. As you can see, there were 8 companies that had positive EPS surprises and only 2 that had negative surprises. Interestingly, this great data is coming from a group which includes 6 names which are down year to date. There were 3 names which had positive EPS and sales surprises which are down year to date. The beleaguered GE stock was down 4.44% on Friday even though it was one of the 3.

1 Comment

James Teh

July 24, 2018Many thanks Bro Don