Earnings Revisions - Predicted Stocks Would Fall

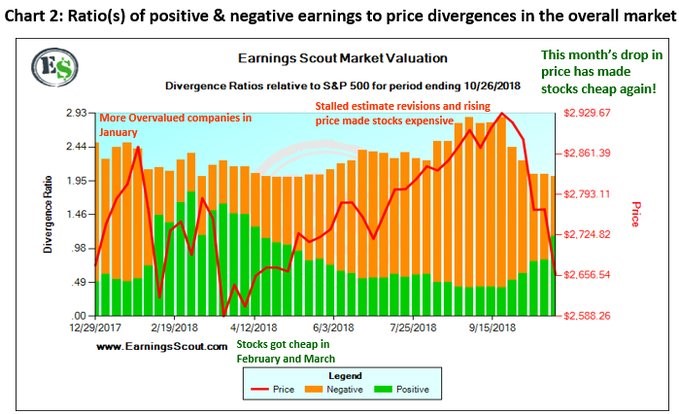

Earnings Scout chart on earnings estimate revisions versus the S&P 500 did a great job of forecasting the volatility in October.

I always put various economic and stock market related research into my articles. It gives readers an understanding of the bullish and bearish arguments.

And it helps you see in real time which analysis worked and which analysis failed.

As you can see from the chart below, there was an increase in negative revisions and a decrease in positive revisions late in the summer.

Shortly afterwards, stocks peaked. I showed this chart in an article over the summer. Thus proving there was no data manipulation after the fact to make it look correct.

Obviously, the next step in reviewing this chart is to see where stocks will go in November. As you can see, the S&P 5000 has fallen near the winter lows. Negative guidance has fallen, and positive guidance has risen.

Based on the guidance changes, stocks are a buy right now. However, not as much of a buy as they were in February. Also, the sell signal was stronger this summer than last winter. There were more negative revisions in September than January. I will review 2 important earnings trends in this article.

Earnings Revisions - Sharp Earnings Multiple Compression

First, it’s important to recognize that earnings have grown from the last sell off until now. Whether you choose to look at trailing or forward earnings multiples, stocks are cheaper now. They're actually lower than they were at the February low even though they are higher now.

As of Friday, October 26th the S&P 500 was nearly flat for the year which means there has been sharp multiple compression.

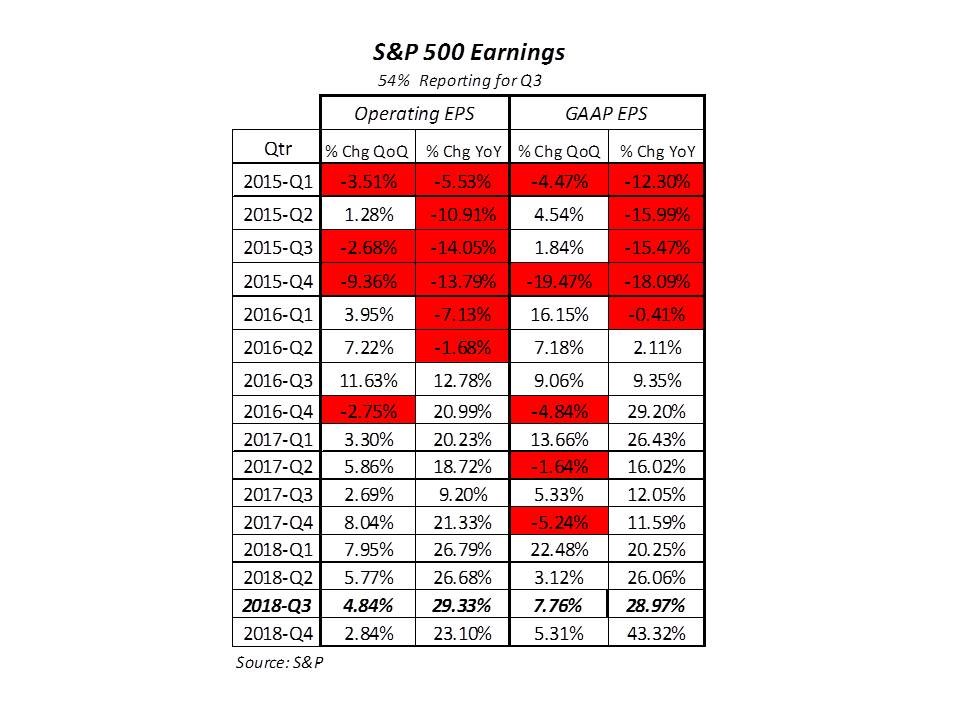

The table below shows the operating and GAAP EPS growth rates for S&P 500 firms. It shows since Q1 2015 on a quarter over quarter basis and a year over year basis.

As you can see, year over year operating EPS was up 26.79% and 26.68% in the first two quarters of this year. GAAP EPS growth was 20.25% and 26.06%.

There has been sharp multiple compression. That's very rare for a bull market which hasn’t fallen much on the year. It’s fair to question how much of the great 2017, which had no corrections, priced in the tax cuts and earnings growth acceleration.

Simply, stocks are way cheaper now than they were at the February bottom.

Earnings Revisions - Weakening Earnings Growth

The second trend to focus on is the deceleration in earnings growth. Stocks have followed earnings growth in the past few years.

From 2015 to 2016, stocks plateaued and had a couple sharp corrections as earnings growth was negative. Since the 2nd half of 2016 stocks and earnings growth have accelerated.

Much has been made of the peak in earnings growth this year, but that’s irrelevant to market timing. Rate of change is important to follow. Stocks move up even if earnings growth slows. So, you can’t call for a bear market if earnings growth returns to the long term trend.

It was always impossible to sustain this year’s growth rate.

Earnings Revisions - Not shocking to See Earnings Closer to Long-term Average Growth Rate

A major unanswered question on investors’ minds was never when earnings growth would peak. It’s how far growth will fall. This bull market will continue if earnings growth is in the high single digits in 2019.

That correction in October is pricing in the increased probability that 2019 earnings growth estimates won’t be achieved.

For the past few months I have been discussing the possibility of earnings growth disappointing. I’m not willing to project earnings declines or a bear market. But the economy could set that up for 2020.

The Fed is tightening rates quicker and the boost from the fiscal stimulus is almost over. A potential trade war is just starting to hurt the economy. Global growth is slowing. However, the Chinese tax cut could save growth.

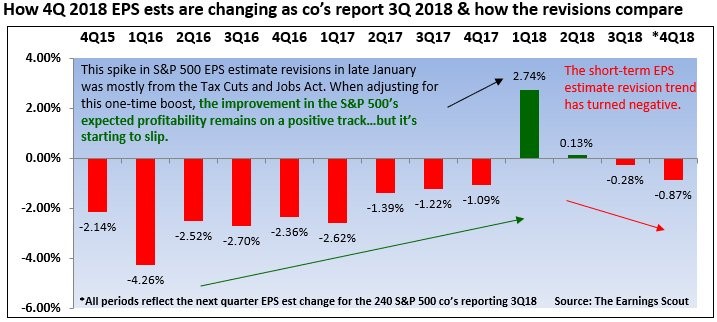

The chart below shows the current estimates for future earnings. As you can see, the Q3 results have pushed down Q4 EPS growth estimates. However, Q1 and Q2 2019 estimates have been stable.

From October 1st, Q4 year over EPS growth estimates fell from 15.37% to 14.29%. Estimated growth in Q1 fell from 8.79% to 8.39%. It rose from 6.47% to 6.54% in Q2.

A new problem is earnings growth estimates have been weakening intra-quarter. Starting with lower estimates makes this more difficult to deal with.

Going from 25% growth to 20% growth isn’t ideal. But going from 9% growth to 4% growth limits the bull market severely.

The chart below shows the recent stats on these intra-quarter declines. As you can see, estimate revisions were up in the first 2 quarters of 2018. They have fallen in the last 2 quarters, which is back to the historic trend.

If estimates keep falling less than 1%, it wouldn’t be an issue. However, there would need to be a catalyst for this reversal.

Instead of a positive catalyst, firms are faced with the negative trends and very tough comparisons. Q4 earnings season isn’t for a few more weeks. Which means we could see more deterioration than last year’s 4th quarter.

Earnings Revisions - Q3 Results

According to Bespoke, EPS results have been solid this year, but revenue has been sub-par. 67.2% of S&P 500 firms have beaten EPS estimates.

Even in recessions, it’s unusual to see more firms miss than beat because the estimates are manipulated. That’s why it’s better to look at estimates than the beat rate.

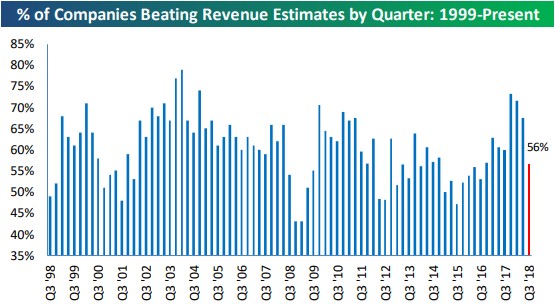

The revenue beat rate is a better indicator than the EPS beat rate. As you can see from the chart below, 56% of S&P 500 firms have beaten their revenue estimates. That's the lowest beat rate since late 2016.

This data makes it look like late 2018 could be like the slowdowns in 2011-2012 and 2015-2016. There are still many firms left to report earnings. But the trend of 3 straight quarters with declining beat rates isn’t ideal.

Earnings Revisions - Takeaway

The takeaway from the data in this article is the Q3 results are middling in relation to expectations. The future EPS estimates aren’t cratering like the stock market correction implies. Stocks are a buy now, but the underlying growth trends are weakening.

1 Comment

Sharon Thorne

October 30, 2018The earnings are going lower. The market is losing steam. It's time for the market to reverse for a while.

Sharon