Global Earnings Drive Growth

If an analyst states “the fundamentals are sound” on financial T.V. during a correction, he/she gets mocked because the fundamentals have no relationship to the near term trading action. However, it is an important assertion because if the fundamentals are sound, the selling will be limited. If the fundamentals aren’t sound, the correction will turn into a bear market. Part of the reason these analysts get mocked is because there’s always someone saying the fundamentals are sound. Even before the financial crisis, there were analysts downplaying the negative catalysts. They said housing was only a small part of the economy. Obviously, the home builders and real estate agents are a small portion of the economy, but elevated default rates hurt banks and borrowers.

This time, the fundamentals are sound which means the current correction probably won’t get much worse than down 15%. My basic understanding of technical analysis says stocks might retest the lows before rallying again; it seems like the correction is almost over. The chart below shows the fundamentals are principally boosted by earnings growth from international firms. This means tech is doing well because the sector has a large international presence. As you can see, the firms with over 50% of their sales coming from international markets have greater sales growth and margin growth. Their earnings growth is 17.4% which is much higher than the 12% growth from firms with less than half of their sales coming from international markets. The tax cut is supposed to help domestically oriented firms, but the repatriation holiday also helps international firms. Therefore, this relationship should continue in Q1 2018.

Stocks Are Much Cheaper Now

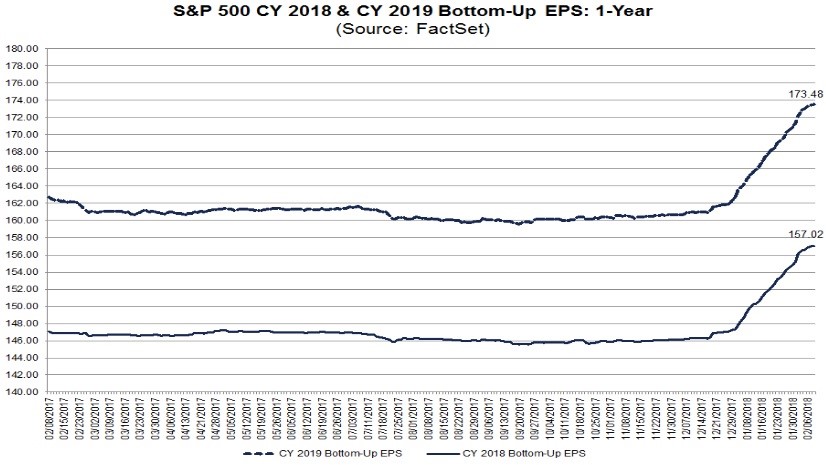

The fastest way for the forward earnings multiple to decline is if expected earnings increase and stock prices fall. That’s what has been happening in the past couple weeks. This is a sharp reversal from what we have seen in the past couple of years when either stocks were going up faster their earnings growth or stocks were stagnant and earnings growth was negative. The chart below shows the recent changes in 2018 and 2019 earnings estimates.

Normally, I’m not concerned with over 12 months into the future because those estimates are far from reality. I care about 2019 estimates now because their recent change is unprecedented. It appears both estimates have slowed down from their rapid increase. This makes sense because 68% of firms have now reported earnings. If it took until after the reports for analysts to update their models, I think most of the impact from the tax cut is now in the estimates. Therefore, I expect both estimates to go up less than $3 in the next month. That being said, $173.48 is an amazing number. At the current level, the S&P 500 has a 15.3 multiple on the 2019 earnings. The 5 year average 12 month forward PE is about 16. If stocks don’t rally in the next 10 months, there will be a severe multiple compression because the forward PE multiple peaked at about 20 last year.

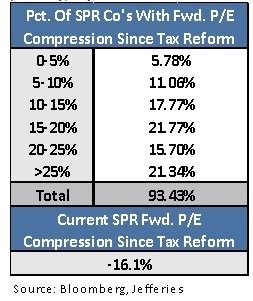

Tax reform was billed as a big catalyst for stocks to increase. Few discussed the possibility that the tax reform would increase earnings, but decrease multiples. As you can see from the chart below, the current forward multiple has compressed 16.1%. Stocks went from very expensive to near average multiples. Obviously, this is counterintuitive. Let’s review why it might be incorrect. Firstly, stocks just had a correction because sentiment got too high in January. If stocks rebound in the next few months, the multiple compression will be smaller. Secondly, stocks probably rallied in 2017 because of the prospect of tax reform. Now that it has passed, stocks aren’t going up much. The high multiple at the end of 2017 was likely related to the expectation that the corporate tax rate would be lowered.

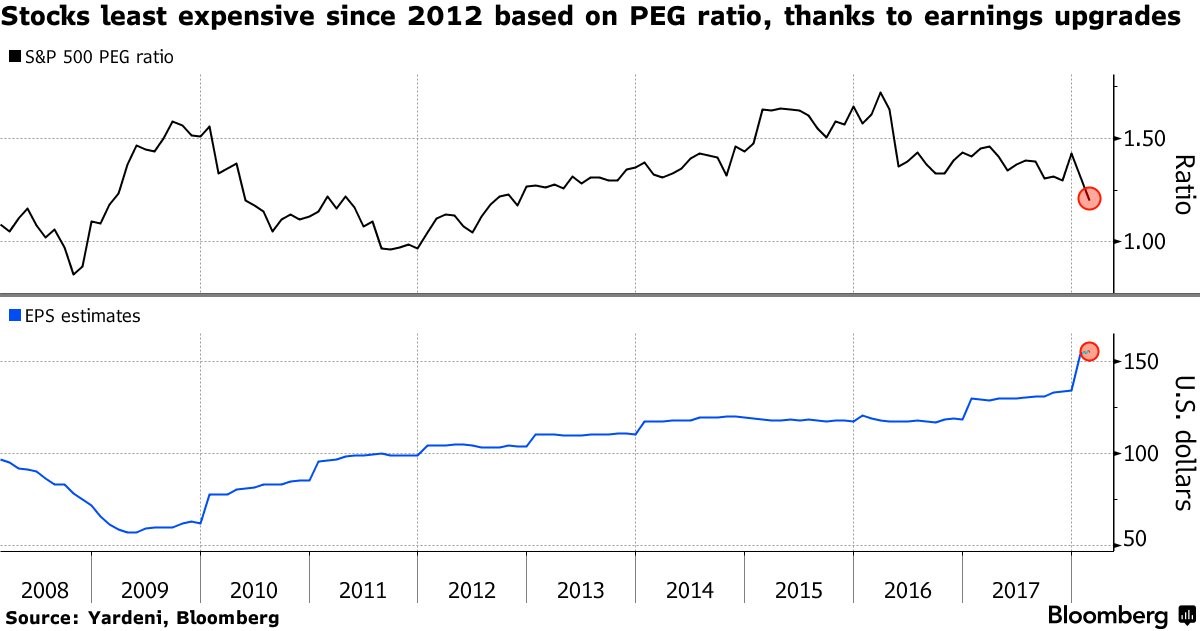

The valuation metric which has been the most affected by the recent action in earnings estimates is PEG because reported earnings and growth expectations are up. As you can see from the chart below, the increase in earnings and growth along with the decrease in stock prices has caused the PEG to decline to the lowest level since 2012. The PEG is probably artificially low because the earnings growth in 2018 is boosted by tax reform. 2018 earnings are compared to 2017 when the tax rate was higher. The earnings growth in 2017 is expected to be 10.9%. It’s expect to be 18.9% in 2018. In 2019 it’s expected to be 10.5%. As you can see, the earnings growth spikes higher in 2018, before leveling off.

2019 Earnings Estimates Might Come Down

I also think the earnings growth next year might not meet the current expectations. Since most analysts have added the benefit from tax reform to their estimates, there’s only one way for earnings growth to go: down. Earnings estimates usually fall throughout the year. I expect next year to be no different. The economy next year might not get the same stimulative effect as this year as the tax reform boost wears off. At that point, the Fed will also be hawkish since the unwind will be $50 billion per month and rates will be 75 basis points higher to start the year. The latest odds for a rate hike in March is 77.5% as the meeting is 36 days away.

Conclusion

For the first time since early 2016, stock multiples fell. Since 2018 earnings growth is expected to be 18.9%, stocks need to go up significantly to not have some multiple compression. I don’t think stocks will go up 18.9% this year because 2017 returns partially priced in the tax cut. However, I still expect stocks to have positive returns as the economy and earnings continue their expansion. Next year looks great according to earnings estimates, but I’m less excited about it because the stimulative effect of the tax cut should wear off and the Fed will be hawkish for the first time in over a decade.