The earnings season is now about 90% over, so when we look at the results, they are close to what the finalized ones will look like. The biggest lever of this great earnings season remains margins. The latest results show margins were 10.22%. That’s higher than the previous cycle high which was 10.10% in Q3 2014. The S&P 500 just missed the as reported record high in trailing 12-month earnings. The record is $105.96; it reached $104.00 this quarter. On a year over year basis, financials had the highest sales growth which was 25.33%. That’s because of the Fed’s rate hikes which improve their net interest margins. There’s also an improvement in credit conditions compared to last year. There has been moderate issues in the auto and student loans sectors this year, but that pales in comparison to the weakness seen in the energy sector in 2016. Some may look in hindsight at the recession calls in 2016 and say they were ridiculous because there was only weakness in energy and manufacturing, but they would be ignoring the record low recovery rates. The credit conditions came close to signaling a recession.

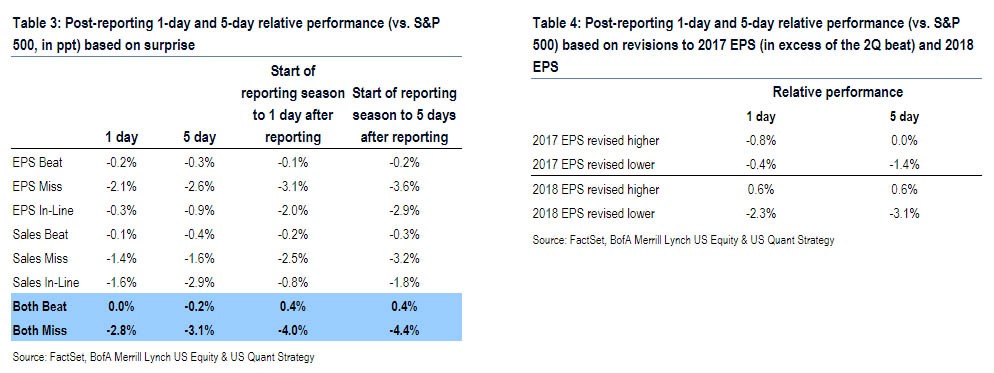

Total sales growth year over year was 5.78% showing how the profit growth was mainly driven by margin expansion. 68.3% of firms beat sales growth and earnings were beat 70.59% of the time. Expectations were high, so the fact that more firms beat earnings expectations than average is impressive. Even with those impressive results, stocks still fell versus the S&P 500 after beating sales and earnings for the first time since Q2 2000.

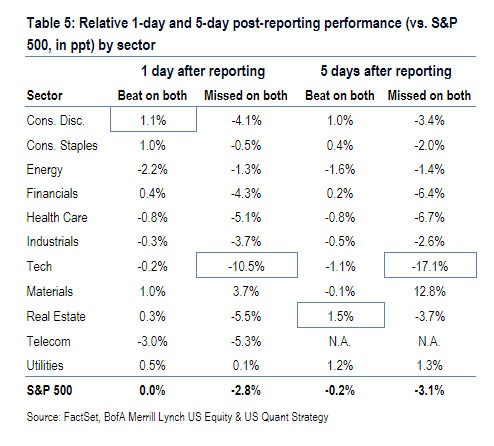

The chart below breaks down how firms reacted to earnings results by sector. This shows energy declining 2.2% after beating on both. I think that might be because oil prices were down, so guidance was bad. Energy is a unique sector where it’s reasonable for a firm to beat results and talk about how bad the business is doing because it’s dependent on oil prices. It gets especially complicated when it comes to hedging because sometimes firms sell oil for below the spot price. Pioneer, which is considered to be the best firm at hedging, sold at below spot price. Besides having poor results, the firm may have lost the premium it got for being a well-managed firm when it crashed after reporting.

Technology firms did the worst after 1 day and 5 days when they missed on both sales and earnings. The sector also fell when beating sales and profits. These results are affected by Alphabet which had a great result and fell. Part of the reason the stock may have sold off after reporting was the massive fine the EU handed the firm. The main headline surrounding the quarter was about the fine as the results were a sideshow. Alphabet almost always beats results, so the fine was a new story which got a lot of discussion. The other reason for the weakness in tech despite the fact that it is firing on all cylinders is the excessive hype. The stories about Amazon and Apple reaching trillion dollar market caps need to calm down. If everyone thinks a firm will beat, it is priced for perfection even if it doesn’t have a high valuation. That’s an alternate way of looking at valuations, but needs to be mentioned when you see Alphabet falling when it seems reasonably priced.

The charts below give us a more specific picture about what may have happened this earnings season. One of the other trends this earnings season was that Q3 earnings estimates fell quite sharply. As you can see below, after 5 days, the stocks which had their 2017 guidance lowered fell 1.4% compared to flat results after guidance was raised. Looking at 2018 guidance, firms which lowered guidance fell 3.1% after five days. Stocks which raised 2018 guidance were up after one day and five days. It shows how 2018 guidance is more important than 2017 as investors start looking at next year in the late summer usually. It’s a great sign for a firm to have the visibility to talk about 2018 earnings let alone talk about how great the year will be.

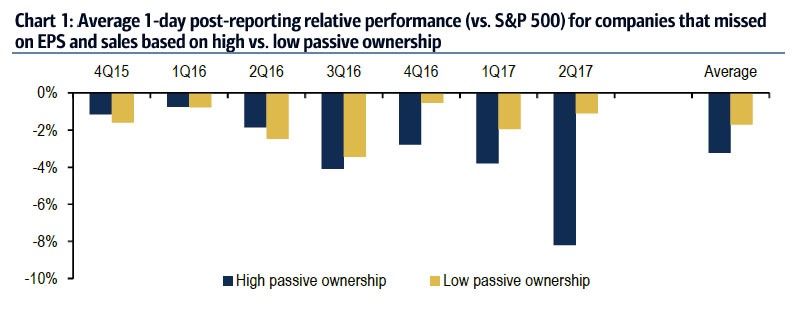

Besides excessive optimism, the other aspect thrown around is how passive investing is messing with earnings reactions. It’s logical that if some investors don’t buy stock based on fundamentals, when fundamentals take a turn for the worse, there will be a mass exodus out of stocks. The chart below shows stocks with high passive ownership did very badly this quarter after missing sales and earnings results. Some would expect that passive investors would calm the market, but they don’t because it causes securities to not be accurately priced. The big worry is that this could happen on a mass scale during a recession. It’s not a big deal when only 20.04% of firms miss estimates, but when most firms miss estimates it could be a blood bath. Keep in mind, this selling is coming from active investors. Imagine what happens when passive investors start selling stocks. That would only happen if earnings as a whole took a tumble which is why I mentioned a recession. You only see the consequences of a change when the tide goes out.

Conclusion

The earnings season was great as technology firms continued to power higher. Weirdly, their stocks didn’t react to the great results and they fell sharply when they missed expectations. That’s a sign of over optimism. If earnings season was bad, there could have been a crash. Don’t take that the wrong way because the fact that earnings were good is still a positive. I don’t expect as much weakness as I normally did earlier in the year now that we’re seeing a crashing dollar. My prediction for slowing earnings growth in the back half of the year and the dollar bubble popping was inconsistent unless the economy showed more weakness than it is showing now. I don’t expect stocks to fall unless there’s a monetary policy screw-up or debt ceiling related stress.