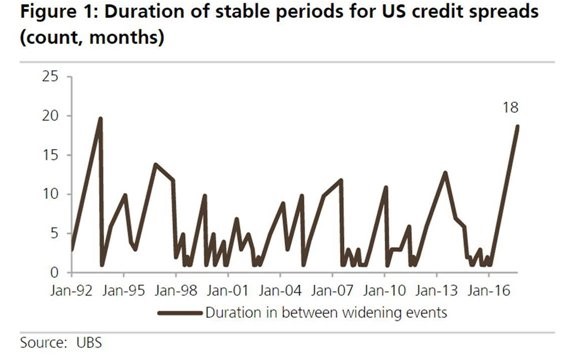

The chart below shows the situation the bond market is currently in. The tightening of credit spreads has occurred for the past 18 months as the ECB’s bond buying has been combined with animal spirits creating a great scenario for risky bonds. As you can see, this is the longest period of tightening since the early 1990s. It shows how the bond market is also coming close to records just like stocks are. Stocks have gone 221 days without a 3% selloff which is 20 days shy of the all-time record.

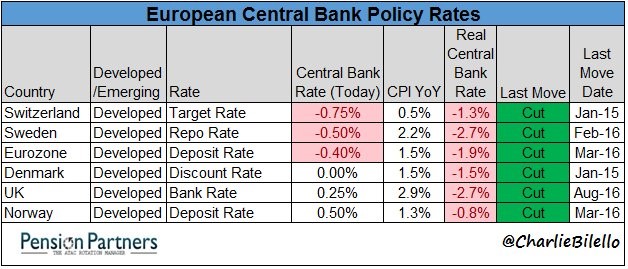

The chart below explains how the European central bank policy has shifted capital into the high yield market. As you can see, all the central banks’ last moves were cuts and all the policy rates are below 1%. The last time the ECB cut rates was March 2016. It’s not expecting to raise rates again until 2019 at the earliest. That shows how the ECB has combined dovish policy with dovish guidance. The ECB is basically saying not only should you buy high yielding bonds, but you should also not worry about this purchase for the next few quarters.

The European high yield index fell down to 2.33% which is an all-time low. High yield barely has any yield at all. At this pace, a company with no business model will be getting free capital to do whatever it wants. That’s not an example of efficient capital markets. The European high yield credit spread recently hit a 10 year low at 271 basis points. Some are saying we need to ignore the high yield spread in this past cycle and start with looking at the mid 2000s as a comparable period. It gets dicey when you try to avoid history. That would be like ignoring times PE multiples were low and only looking at bull market peaks to justify prices. There’s no doubt the ECB is pressuring yields. The main question is when this corporate bond buying spree ends and normalcy returns.

One of the reasons the three major indexes were down on Monday was Apple. AAPL is now down 8.23% since September 1st and is down 4 days in a row. This is AAPL’s worst month since April 2016. As you can see from the chart below, AAPL is responsible for 20% of the S&P 500’s rally, so it’s clearly important. I think now would be a good time to buy the stock since it will get hype again from those who are waiting with baited breath for the iPhone X to go on sale. Bank of America is saying that you can’t look at poor iPhone 8 results as a reason to write off the entire product cycle. I’m not sure if the iPhone X will sell well, but I think the optimism will grow for the iPhone X in the next 4 weeks as we see a mini-hype cycle which is unusual for Apple because there typically isn’t a large period between a product unveiling and launch. The company decided to delay the iPhone X much longer than usual to make sure there aren’t production issues. Apple users are a group that values having the best devices; we’ll see if that mindset continues in late October.

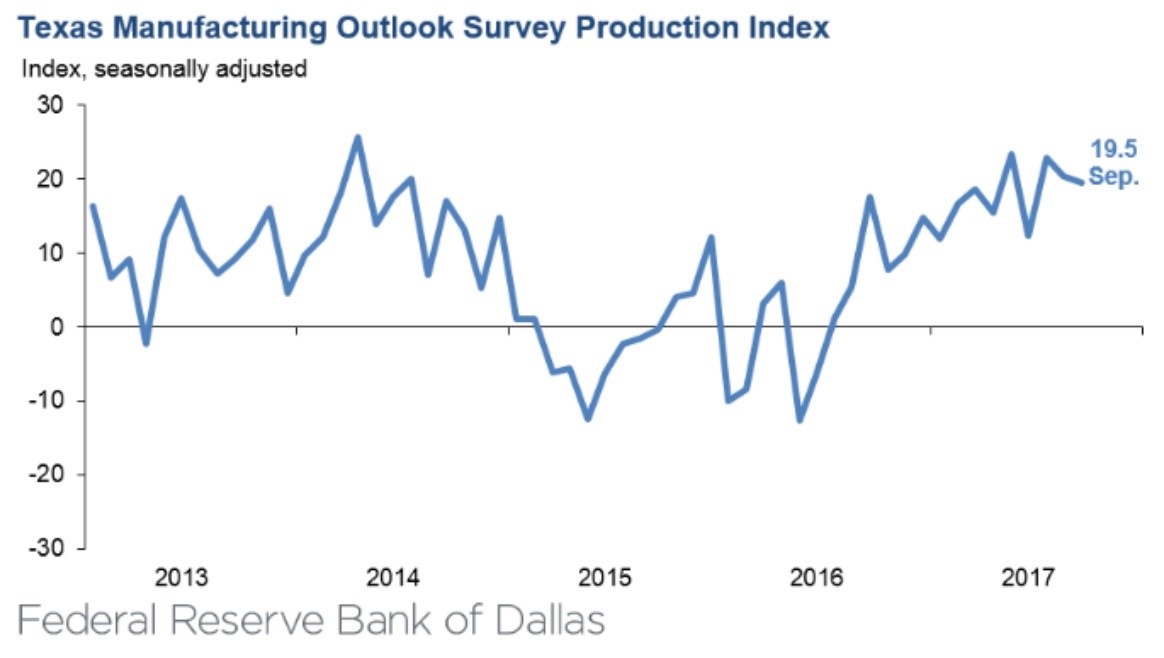

The Dallas Fed’s Texas manufacturing report was released on Monday. This is probably the most important report in a while for Texas because it gives us an idea of where the economy is following the devastating hurricane in late August. As you can see, the index fell from 20.3 in August to 19.5 in September showing little effect from the storm as the manufacturing growth remained steady. The index which shows perceptions of general business activity increased to 21.3 from 17.0, reaching a 7 month high. The company outlook index increased 9 points to 25.6. Every single index within the survey was positive except for the finished goods inventory index. Every index within the forward looking survey showed a positive reading.

There was special questions and quotes taken from businesses to help economists get a feel for the effect of the storm and how far along the economy is towards a full recovery. A chemical manufacturing company said the following about the storm: “Hurricane Harvey resulted in increased raw materials costs and increased inventory. We expect raw materials prices to stay elevated for about six months and then eventually settle back down, but not to pre-hurricane level, probably 50% of the difference.” This supports the point I’ve been making which is that the hurricanes boosted inflation. However, this business says increased raw materials prices will stay high for another 6 months. If inflation stays high until December, there will be another rate hike. After December, I start ignoring the data because the next Fed chair pick is more important than individual metrics.

A nonmetallic mineral product manufacturing company said they shut down business for 7 days. That gives you an idea for how many days some S&P 500 firms may have shut activity down for their southern divisions. A prime metal manufacturing firm said they may see increased construction related to Texas and Florida. That means there hasn’t been much rebuilding yet. Finally, a fabricated metal product firm said that it couldn’t find enough workers to make repairs to the damaged refinery. This is consistent with the discussion we’ve had about how manufacturing labor is tight. Obviously, adding a bunch of new workers is tough in an already tight labor market.

Conclusion

If the Texas manufacturing economy looks fine, then the overall economy should easily rebound from hurricane Harvey. The work stoppage of a few days is a temporary issue that will affect Q3 earnings and GDP growth. The rebuilding process could add to inflation as raw materials inventories run low and there is tightness in the manufacturing labor market. Even the first major hurricane in 12 years making landfall in America hasn’t ended the trend of credit spreads tightening and hasn’t caused the S&P 500 to have its first 3% decline this year.