The CPI report came out today. To no one’s surprise, the stock market is up on the news. It reached a record high for the 5th straight day even as the VIX was up 11.45%. The Shiller PE has reached a 29 handle which means it is about 3.5 points away from the high set in 1929. I consider this significant even though the bulls will point to the period in the 1990s when it went into the 40s. According to a paper done by Valentin Dimitrov and Prem Jain called “Shiller’s PE: Market-Timing And Risk” stocks outperform treasuries unless the Shiller PE is extremely high. The level where it reaches extremely high is 27.6. They concluded buying and holding stocks is usually a good strategy unless stocks are extremely expensive like they are now. Even if you hold stocks for the long term, you’ll likely experience subpar returns.

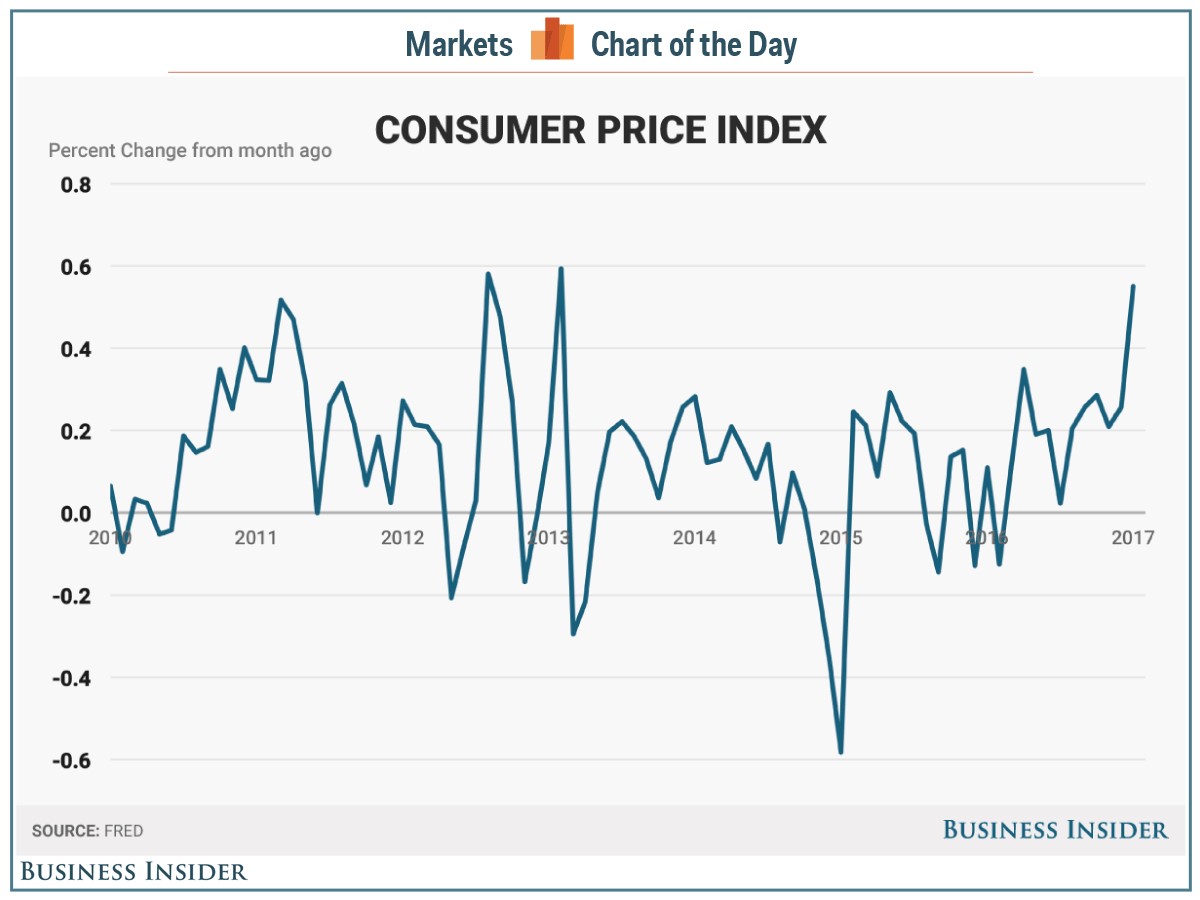

The CPI report showed 0.6% price growth in January which was up from the 0.3% growth in December. It was much higher than the 0.3% expected by economists. As you can see in the chart below, this was the highest rate since February 2013. The trailing 12-month CPI is now up 2.5% which is the highest rate since March 2012. Core CPI, which excludes food and energy prices, increased 0.3% in January and 2.3% in the trailing 12 months. Even though oil prices have stabilized in the low $50s, the biggest contributor to the overall CPI gain was gasoline.

The 7.8% rise in gasoline accounted for nearly half of the CPI gain. One would think this rate of increase is unlikely to continue, but the reason the core CPI is studied is because of this consistent volatility. The EIA reported the 6th straight week of increases in crude oil supplies. The total stockpiles increased 9.5 million barrels to 518.1 barrels. This is a record high stockpile going back to 1982. This potential decline in oil prices may allow the Fed some wiggle room with the number of rate hikes it needs to do to quell inflation in 2017.

This brings us to the Fed’s potential reaction to this report. Even though the CPI is above the Fed’s 2% target, the Fed’s favorite inflation gauge, the PCE, is still at 1.7%. This means there won’t be a drastic change in policy. However, the market had a more substantial reaction to how it priced in rate hikes than its reaction to the Fed’s report to the Senate on Tuesday. The chance of a rate hike in March went from 17.7% to 26.6%. On CNBC, Steve Liesman claimed he didn’t know what Yellen would have to say to move the market. He thought Yellen was relatively hawkish in her Senate report. The difference of opinion depends on if you take the Fed’s words at face value or not. The Fed must raise rates in March if it wants to raise rates 3 times this year. The Fed must eventually go against what the market prices in if it raises rates 3 times as the market still is pricing in 2 hikes. The increase in the odds for a March hike doesn’t change my perspective that it’s still not a ‘live’ meeting. The odds need to reach 70% for it to be ‘live.’ Reaching that rate in 4 weeks is highly unlikely.

The 10-year bond yield rose 3 basis points which is significant as it’s now above 2.50%. The stock market views inflation increases as good because it believes the economy will be less reliant on the Fed. In terms of the goldilocks analogy which is often used, the economy was too cold and it’s moving to be the perfect temperature. There’s a difference between what is good for the economy and what is good for stocks. I think moderate inflation, rate hikes, and a higher 10-year bond yield isn’t bad for the economy if it is accompanied with real growth. However, any of those results occurring should lower stock multiples. The stock market is ignoring reality. At some point a higher CPI will start to hurt stocks even though they are enthused by today’s relatively hot report.

The initial reaction by the dollar was to rally. It is weird to see a dollar rally on higher than expected inflation, but this is in tune with the narrative that the U.S. economy is improving relative to other economies. If a hot European CPI caused the ECB to raise rates before the Fed, it would hurt the dollar. The hot CPI report today makes that scenario less likely. In my opinion, the reason why the dollar sold off after its initial pop is probably because it had been on such a tear previously. It increased from 99.51 to 101.73 at the day’s peak in just about 2 weeks. This appears to have been a counter trend rally. I’m surprised to see the dollar increasing given that it looks like the border adjusted tax is less likely to be passed now than the last time I discussed it. Trump met with retail CEOs today where they told him why it is a bad idea.

Retail sales for January beat expectations. They grew 0.4% which is better than the 0.1% economists projected. December’s report also had a significant positive revision as it was moved to up 1% from up 0.6%. This goes against the disappointing earnings reports from consumer discretionary firms in Q4. Year over year January retail sales were up 5.6% despite the biggest drop in motor vehicle sales in 10 months. Receipts at auto dealerships fell 1.4% after increasing 3.2% in December. There may have been a sequential decline in discounting, but I don’t have that metric.

Conclusion

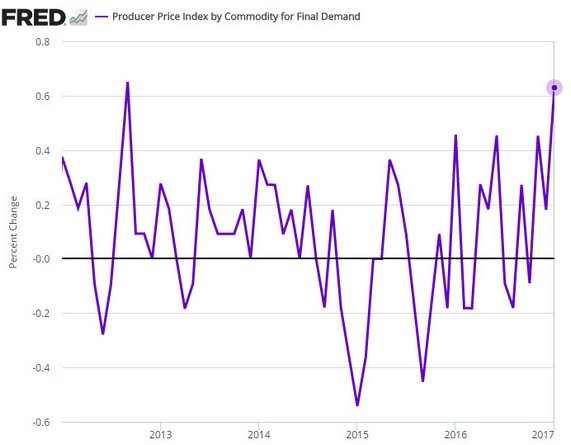

In my opinion, it makes sense to look at several metrics of inflation to decide policy. The chart below shows the producer price index for final demand is increasing at the highest rate since 2012. However, the Fed likes to pick favorites with metrics. For example, the labor market conditions index is Yellen’s favorite labor market report. With the PCE at 1.7%, the Fed will still stay on track with its policies. It would be interesting to see what would happen if the PCE indicator started to shoot higher.