Update On The Consumer

September labor report is this Friday. Consensus calls for 850,000 jobs added. Merrill Lynch is calling for 800,000 jobs added with the unemployment rate falling to 8.1%. We are testing how far the labor market can improve without the leisure and hospitality industry.

Sports are starting to let some fans in the stadium, but we need a lot more improvement to get back the jobs that were lost. There might be some weakness from outdoor activities ending. There was more spending on things like camping materials and RVs because of social distancing restrictions.

Chase card spending growth fell in the week of September 21st, albeit barely. Yearly growth went from -5.1% to -5.2%. It is 35.6% above its low of -40.8% in March when most of the country was in lockdown and we had no idea what the death rate of the virus would be.

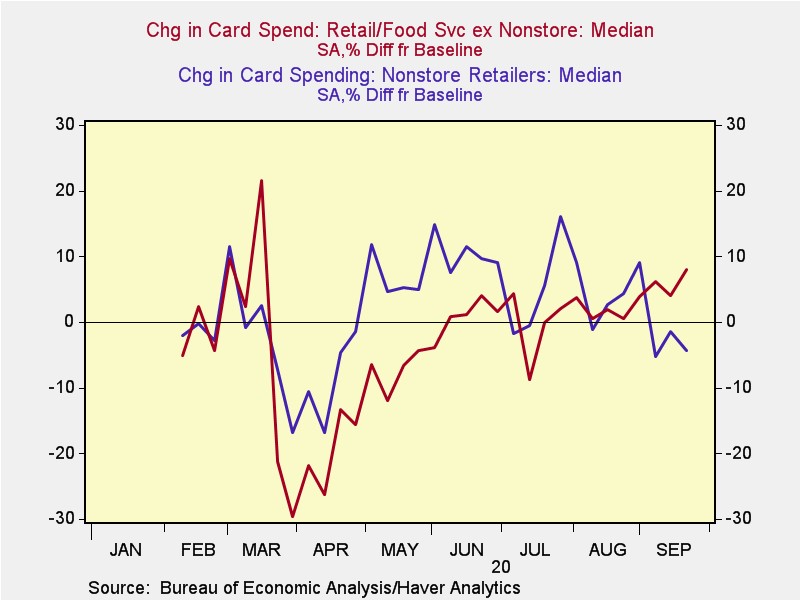

According to the BEA spending estimate seen in the chart below, card spending was up 6.4% in the week ending September 22nd. Spending at general merchandise stores and on home furnishing, auto parts, and accessories were strong.

On the other hand, the chart shows non-store retail spending fell. Shopping online is going to return to the normal trend when COVID-19 goes away which means it will lose market share. This isn’t priced in.

Capex Intentions Improve

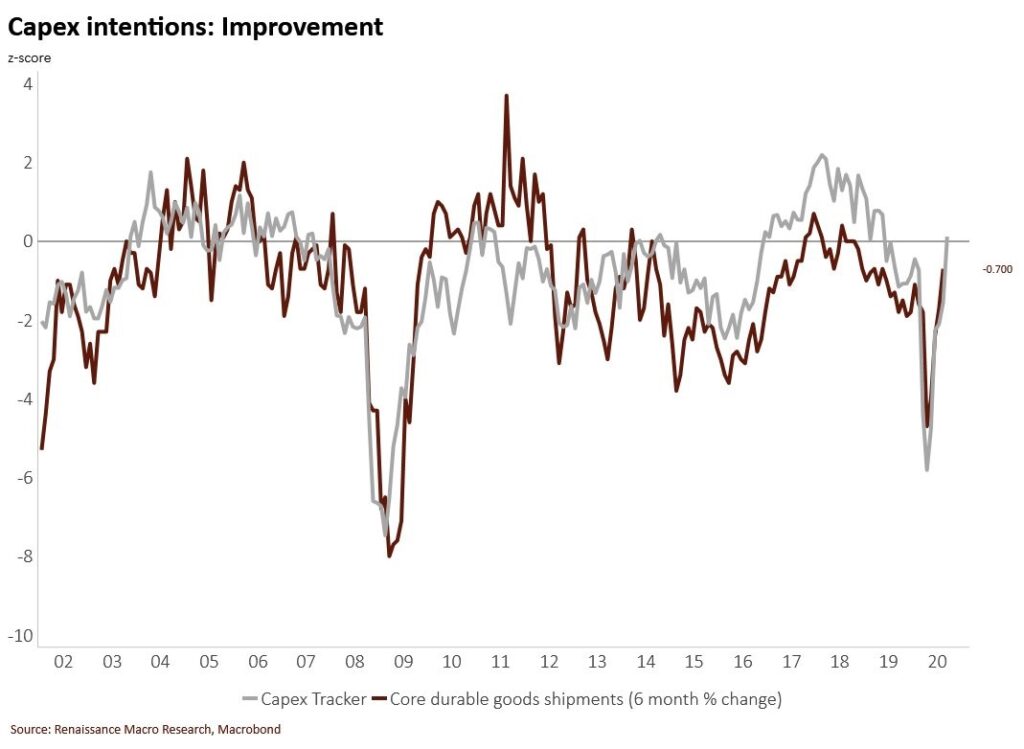

As you can see from the chart below, the z-score of capex intentions from the regional Fed manufacturing reports improved. That makes sense because most of the regional Fed indexes went up. This tracker leads the 6 month change in core durable goods shipments. It means new orders should be strong in the next couple months which will flow through to industrial production and manufacturing soon. Manufacturing will likely be strong on an absolute basis in Q4.

We could actually be looking at a cyclical peak in the manufacturing sector in the middle of next year if everything goes well. A potential catalyst for weakness in mid-2021 would be COVID-19 going away, causing people to spend more on services.

A potential catalyst of strength would be a big spike in oil prices. We could see oil getting to the $80s by the end of next year as more people travel. Investment in new production has been severely limited in the past 2 years which means supply wouldn’t catch up to the increase in demand.

Dallas Fed manufacturing index rose from 8 to 13.6 which beat estimates for 8.5. That’s a 2 year high. By now economists should know the manufacturing sector had a good month. It will be interesting to see how the ISM manufacturing PMI turns out next week. Some investors don’t follow the regional indexes, so they might be shocked by the coming strong PMI.

Dallas Fed new orders index was up 4.9 points to 14.7 and the production index was up 9.2 points to 22.3. The company outlook index fell from 8.2 to 6.7. On the other hand, the forward 6 months production index was up 4.8 points to 47.8. New orders index was up 6.8 points to 49.3. Forward 6 months business activity index was up 7.6 points to 28.

COVID-19 Cases Increasing Rapidly In Europe

A seeming spike in COVID-19 cases in Europe has filtered its way to sell side research which is now being shared by journalists. It’s a little late as most stocks impacted by the new restrictions in Europe have already sold off. This news is already priced in.

Some American stocks that are helped by the economy reopening sold off in sympathy because some investors think America could see a similar sized spike. We will be getting a large spike in testing in the next few weeks along with data on phase 3 trials from vaccines as well as new results on COVID-19 treatments. Even if cases increase in America, that good news could drown out the bad news.

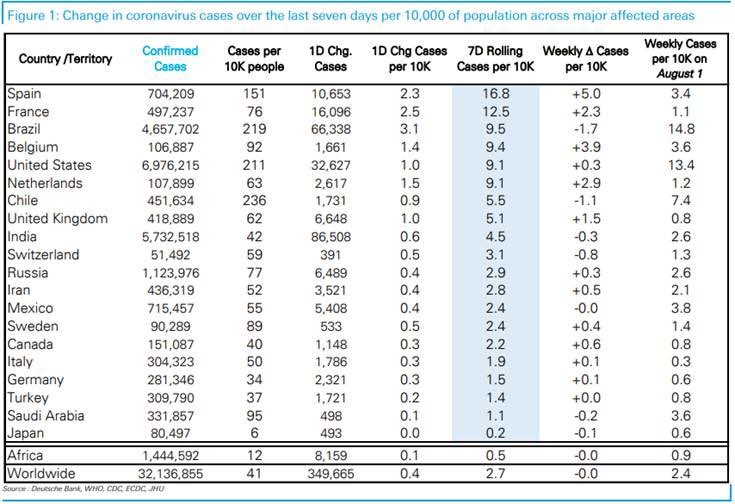

As you can see from the table above, Spain had the biggest increase in cases, with Belgium and France close behind. A spike in cases is almost finished because of the recent new actions to curb the virus. 37 areas in Madrid are in lockdown. Social gatherings were limited to 6 people, public parks were shut down, and businesses need to close by 10 PM.

Members of the armed forces and police have been deployed to help test, trace, and enforce restrictions. By now, the government has gotten good at clamping down on the virus. People also know how to act. We’ve already seen the virus suppressed this spring in Europe.

This could be Europe’s 2nd wave like we had in America in July. There’s a new narrative that COVID-19 is spreading in America, but I it goes too far. Much of the small spike in cases was due to more testing. States with the biggest spikes in hospitalizations are Wisconsin and the Dakotas.

It seems like every area that hasn’t dealt with the virus eventually does. We'd all be worried if New York and New Jersey saw another spike because they were hit the hardest. That would imply, it can come back anywhere else. It’s unlikely to come back though there though because New York still has relatively high restrictions.

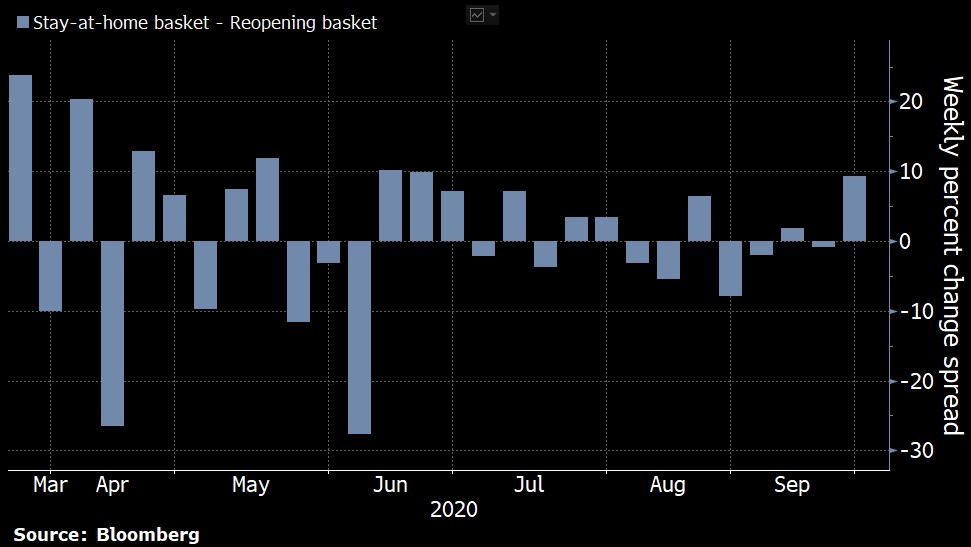

Again, the market has already priced in the spike in cases in Europe. It’s all priced in. As you can see from the chart below, the stay at home stocks like Zoom outperformed the reopening stocks like airlines last week by the most since late June. A stay at home rally in the 2nd half of June predicted the spike in cases in the hotspots in America in July.

Last week’s action fully priced in Europe’s outbreak. However, we could have another 2 weeks where the stay at home stocks win like in June if there is another outbreak in America. On the other hand, good news on vaccines, testing, and treatment could cause reopening stocks to win like they did in the first week of June when some thought the virus was going away and wasn’t coming back.