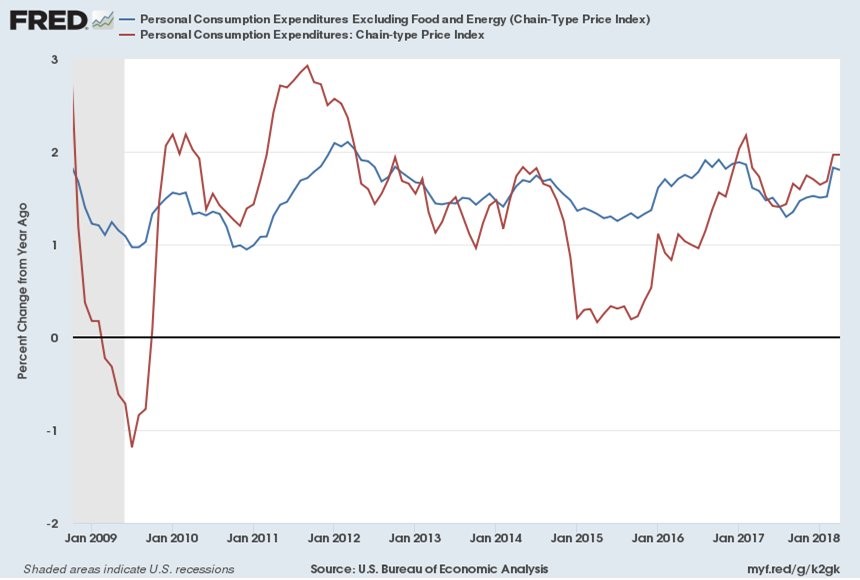

Inflation Stays Moderate

On Wednesday, the Fed’s Beige Book said inflation was moderate in most districts. That was a reflection of past data. I mention this because the latest Personal Income and Outlays report shows the previous trends have continued. As you can see from the chart below, the year over year PCE was 2% which met expectations and was the same as last month. PCE was up 0.2% month over month which also met expectations and was 2 tenths higher than last month. Core PCE was up 0.2% month over month which was the same as March and beat expectations for an increase of 1 tenth. I wouldn’t say this is much to worry about as year over year core inflation was 1.8% which met expectations. March’s report was revised lower from 1.9% to 1.8%. March’s report had been above my expectations, but now we’re seeing inflation wasn’t that high. The April report was slightly below my estimate of core inflation. It strongly reinforces the notion that the Fed shouldn’t raise rates much more this year.

Fed Policy Response To Moderate Inflation

The rate hike odds didn’t move much in response to this report, but that’s not a surprise because the Fed funds futures have become very dovish in the past few days which cancelled out weeks of hawkish movement. Once again, there’s about the same chance that the Fed raises rates 2 times this year as there is the chance the Fed raises rates 4 times. Predicting future Fed policy requires knowing where inflation will be and where the dollar will be. The Fed recently mentioned it would allow inflation to go above 2%. Now that proclamation looks silly because inflation is staying below 2% for the time being. It’s like a playoff team saying who it wants to face in the next round before finishing this round.

If the Fed were to accelerate rate hikes after inflation got above 2%, then I’d say there’s a 50/50 chance the Fed raises rates 3 times versus 4 times. Now that the Fed has prematurely pulled back from that policy and inflation is moderating, it doesn’t look like 4 hikes are going to happen. As I mentioned, forecasting where the dollar index will be is important because we’ve already seen problems in emerging markets due to the rising dollar. The Fed can and should avoid hiking rates if they hurt emerging markets too severely. Regardless of whether the Italian political crisis causes more issues, the E.U. economy is slowing. It will be difficult for America to stay above the fray while emerging markets and European growth decelerate.

Inflation Breakdown

Inflation moderation has occurred for the past few months ever since the January scare. Initially the stock market correction in February was caused by the unwind of the short VIX trade and the scare heightened hourly earnings growth would cause inflation to spike. Both of those issues have been resolved, but new issues cropping up prevented stocks from making new highs. The situation of moderating inflation actually looks better than it is because procyclical inflation is falling and acyclical inflation is rising. The theory is that acyclical inflation is less reliable since it doesn’t correlate with the economic cycle which now signals inflation should be rising based on the low unemployment rate.

The fact that procyclical inflation is falling either signals the indicator isn’t valuable or the economy simply isn’t in an inflationary mode. I think the indicator remains valuable. The reason it might be decelerating is because there is still slack in the labor market and economic growth hasn’t been consistently high for a long enough period. For instance, GDP growth was 2.2% in Q1 and its expected to be above 3% in Q2. If GDP growth stayed above 3% every quarter for a year and the job market remained strong, I’d expect procyclical inflation to accelerate. For now, it looks like if the acyclical inflation starts to fall, the overall inflation will not get above 2% this year.

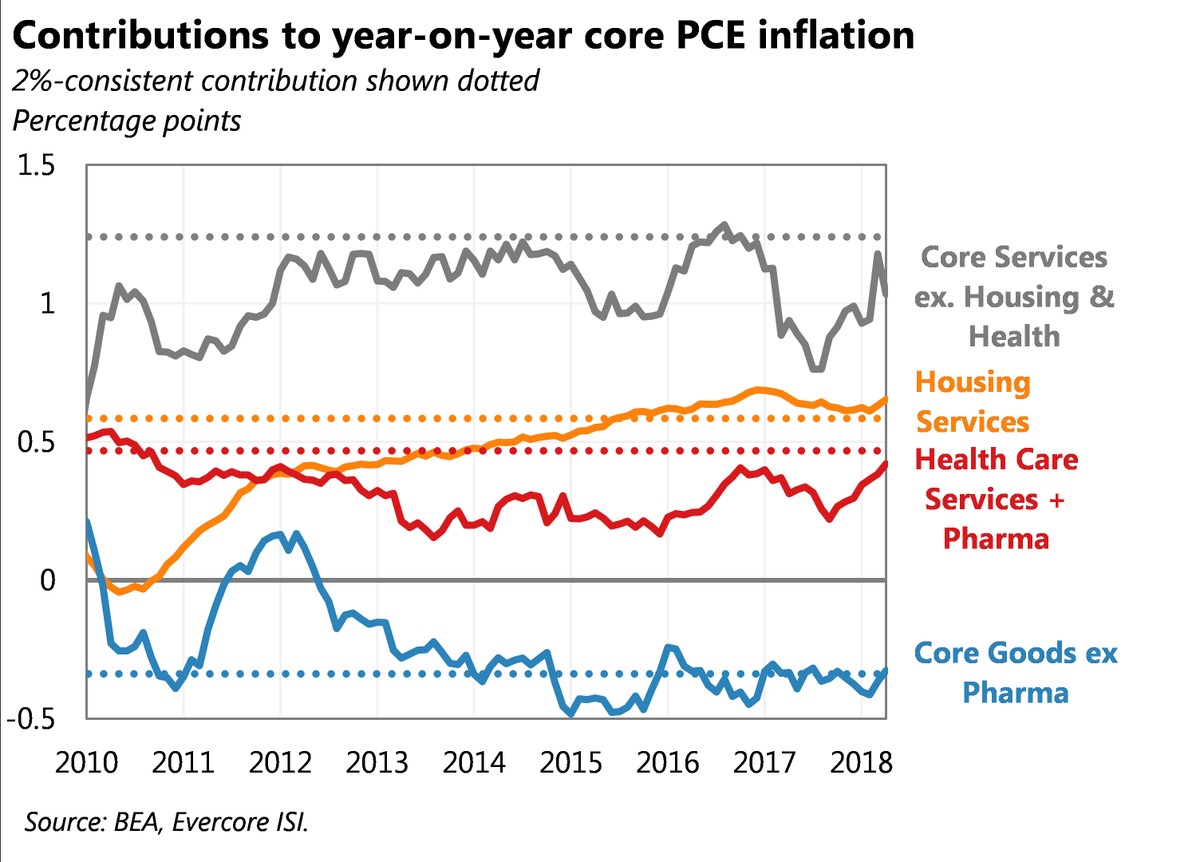

The chart above breaks down the contributions to core inflation since 2010. As you can see, the housing services and healthcare have been the main drivers of inflation in the past few months while core services have recently decelerated. The dotted lines show the inflation rates in each category that are consistent with 2% overall inflation. As you can see, only housing has been consistently above its dotted line for the past two years. Even though the Fed has claimed inflation would come from a labor market that was so tight, wage growth would spike, the only reason core inflation is close to its target is because housing has gotten more expensive.

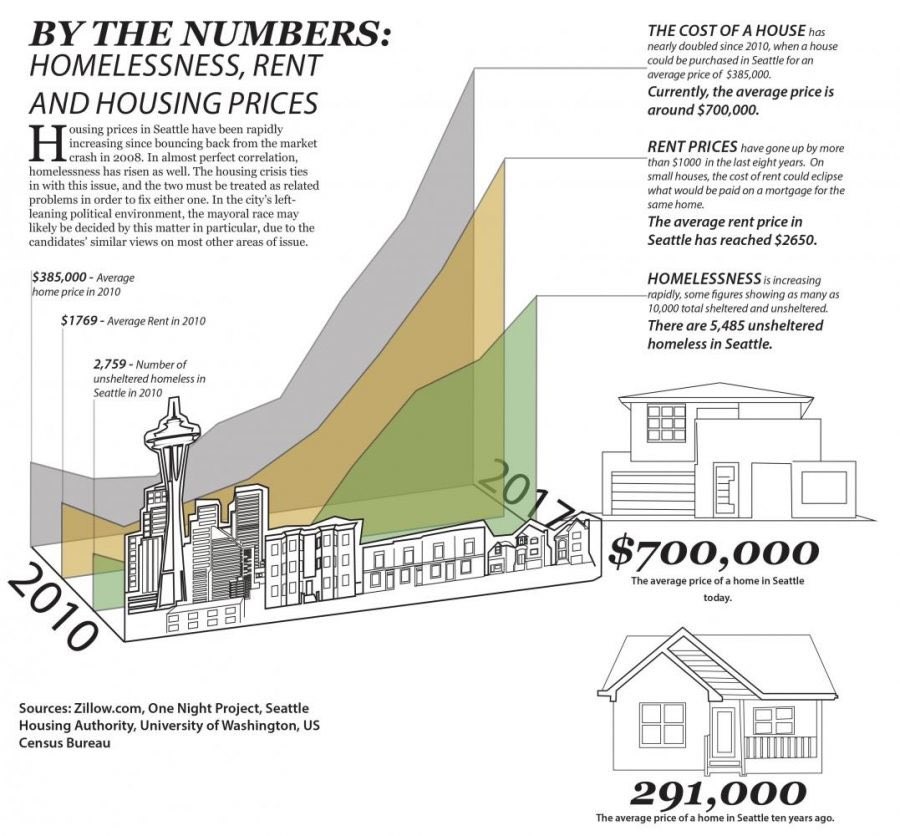

Housing Costs Have Spurred Homelessness

The Fed isn’t in a great position because in a sense it is rooting for higher housing prices because that will get inflation to its 2% target. The number of homeless people has soared in the major American cities. As you can see from the chart below, the average price of houses has increased from $385,000 to $700,000 in Seattle from 2010 to 2017. The price of rent has increased from $1,769 to $2,650 in the same period. Therefore, the number of unsheltered homeless people has increased from 2,759 to 5,485. To be clear, I’m not saying monetary policy is the principle reason for rising costs. The restrictive zoning laws have caused housing prices to increase. It’s especially problematic in Seattle because it is dealing with a population boom which strains resources. While the Fed isn’t the main reason there is a homeless crisis, it’s disconcerting that in order to get to the Fed’s 2% PCE target, it needs to see housing prices increase further which increases homelessness.

Conclusion

In terms of asset prices, low inflation is good for stocks as the Fed probably won’t be raising rates as much as was expected in early May. The Fed is in a tough position to deal with the home affordability issues because it’s a local one. This is a point Neel Kashkari has made. This hearkens back to earlier in this expansion where the Fed had to do more stimulus because fiscal policy action wasn’t taken. Just because the Fed isn’t in charge of local zoning doesn’t mean the issues don’t affect monetary policy decision making.