First Q2 GDP Revision

The Q2 GDP revision was very interesting even though headline growth barely changed. Specifically, real quarter over quarter growth fell from 2.1% to 2% which met estimates. Real consumer spending growth, which was already very strong, was revised even higher. It went from 4.3% to 4.7% which beat estimates 4.3%. Core price growth fell from 2.4% to 2.3% and overall price growth stayed at 2.4% which met estimates.

Government spending growth was 4.5%. This was the one part of this report which made private sector growth look stronger than it was. Non-residential fixed investment fell 6.1% which is consistent with the decline in business sentiment. Residential fixed investment was down 2.9% which marks its 6th straight negative quarter. The positive June new home sales revision wasn’t enough to help this index. I think this streak of declines will end very soon because housing is more affordable. Interest rates are saving the day even though in June house price growth was higher than average weekly wage growth. As of August 29th, the average 30 year fixed mortgage rate increased 3 basis points from last week to 3.58%, but it’s still very low. I see rates falling below 3.4% in September because treasury yields have fallen so severely.

Net exports brought GDP growth down by 0.71%. Inventories hurt growth by 0.91%. Inventory investment might not have as negative of an impact in Q3 if the consumer stays strong. That’s why I see GDP growth potentially coming in slightly above estimates.

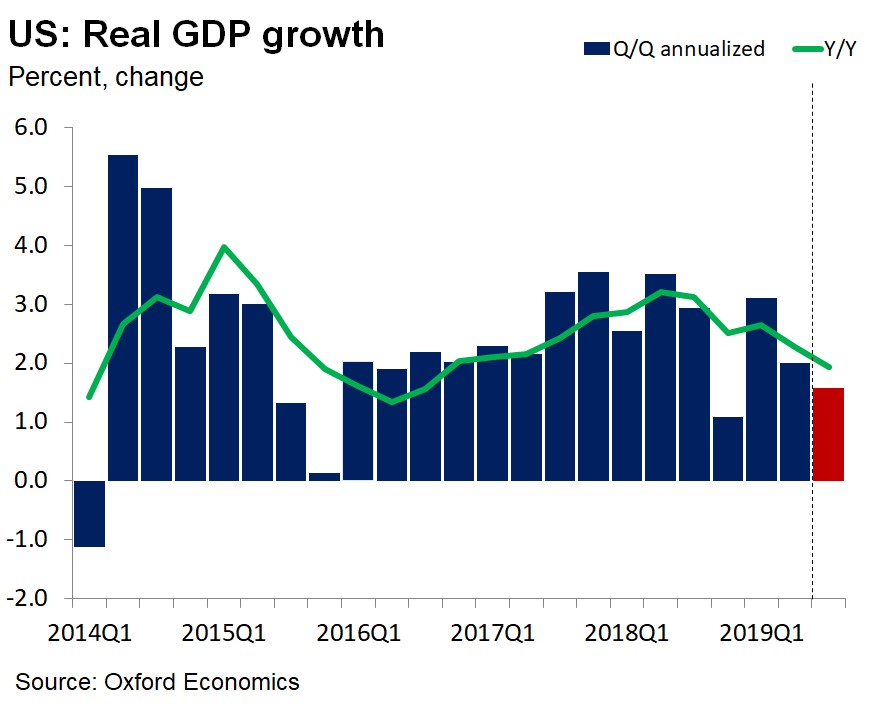

Now let’s quickly review yearly growth. Yearly GDP growth was 2.3% which was down from Q2 2018’s growth rate of 3.2% which was the recent peak. That means on a yearly basis the comps will get easier. On the other hand, the chart below shows the economy is mired in a cyclical slowdown. This slowdown explains why the tariffs can have a big impact. If consumption growth had a 2 handle, Q2 GDP growth would have caused economists to warn about a coming recession.

The main reason why recession talks exist now is the inverted yield curve as the economic data doesn’t show the economy is near a recession. Recessions are dynamic, making them tough to predict. However, it’s easy to tell an economy in a slowdown won’t deal well with a negative catalyst. The next round of tariffs will hurt the one part of the economy that’s doing really well (consumption growth). Yearly consumption growth was 2.7% which is down from the peak of 3.4% in Q3 2018. Business investment growth was 2.6% yearly which is down from 6.9% growth in Q2 2018. Finally, residential investment growth was -3.2%.

Oxford Economics sees Q3 growth coming in at 2%. The CNBC median estimate for Q3 GDP growth is 2%. As of August 23rd, the GDP Now Atlanta Fed projection is for 2.3% growth. The durable goods report caused the estimate of non-residential equipment investment’s contribution to GDP growth to rise 4 basis points to 0.3%. The impact of inventory investment is expected to be -0.47% which is down 3 basis points from the previous estimate. As you can see, even with a negative impact from inventory investment, the Atlanta Fed Nowcast has an estimate above the consensus.

Jobless Claims Are Steady

In the week of August 24th, jobless claims increased 4,000 to 215,000 which was above the consensus of 213,000. The 4 week moving average fell 500 to 214,500. Continuing claims were up 22,000. However, the 4 week average fell slightly to 1.697 million. The bears keep wondering how consumer spending can keep the economy growing. The answer is very simple: the labor market is solid. The decline in job creation growth doesn’t hurt consumers if the number of jobs added still matches population growth. Jobless claims and the unemployment rate are still low. The decline in nominal wage growth doesn’t hurt consumers if inflation also falls.

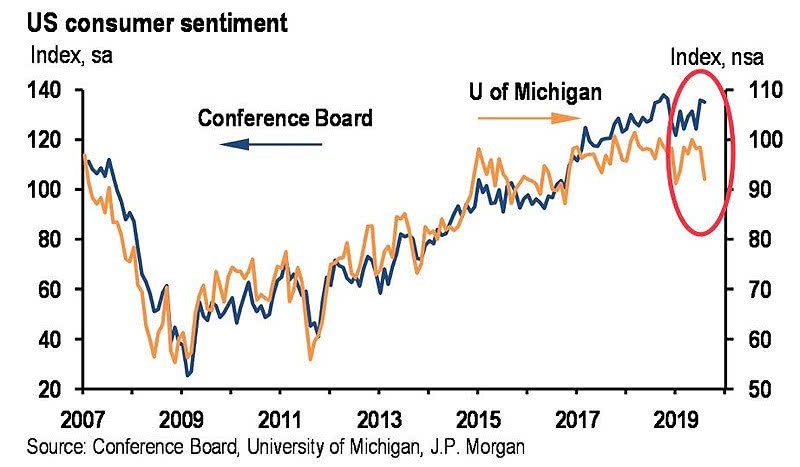

The chart below shows the recent bifurcation in the University of Michigan consumer sentiment index and the Conference Board index. The University of Michigan index is more sensitive to financial markets which is why the preliminary August reading fell. The final reading, which comes out on Friday, will likely show similar weakness especially because stocks have stayed in this mini correction channel. Obviously, the rally in stocks on Thursday wasn’t counted in this final reading. The cutoff day was earlier.

The Conference Board index is more related to labor market conditions where are strong as I just mentioned. This explains why the University of Michigan sentiment index leads the Conference Board index lower when there is a recession. The stock market usually falls before recessions as investors anticipate the downturn.

If this is the case, I trust the Conference Board index more. The consumers know more about the labor market than anything else. I can study the stock market myself. I would rather fade consumers’ opinions on stocks than follow them. On the other hand, I usually look at what consumers think of the labor market in every consumer survey. This perspective on what each metric is sensitive to explains why the Fed’s July rate cut hurt the University of Michigan index significantly.

Trade Deficit Decreases Slightly

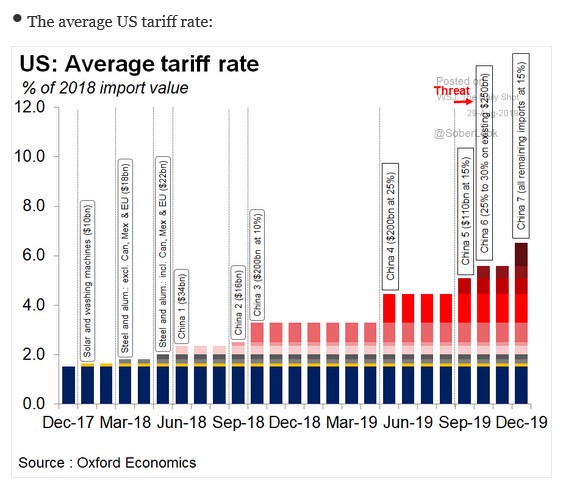

In July, the trade deficit fell from $74.2 billion to $72.3 billion. Exports were up 0.7% and imports fell 0.4%. As I recently mentioned, net exports hurt GDP growth in Q2. The situation might not be as bad in Q3 based on this report. We still have 2 months of data to go in the quarter though. Despite the goal of the trade war being to reduce the trade deficit, it’s still high. The chart below shows the average tariff rate since the end of 2017. As you can see, the trade war will increase the average tariff rate to above 6% by December which is triple where it was two years prior.

Conclusion

There is still no evidence of a recession as Q3 GDP growth is set to be about 2%. Jobless claims are still low and real wage growth is likely positive. Given the fact we’ve recently seen terrible revisions to old data, the 0.1% decline in Q2 headline GDP growth from the initial reading isn’t bad. This revision reiterates how important the consumer is to the economy as quarter over quarter consumption growth was revised to a scalding rate of 4.7%.