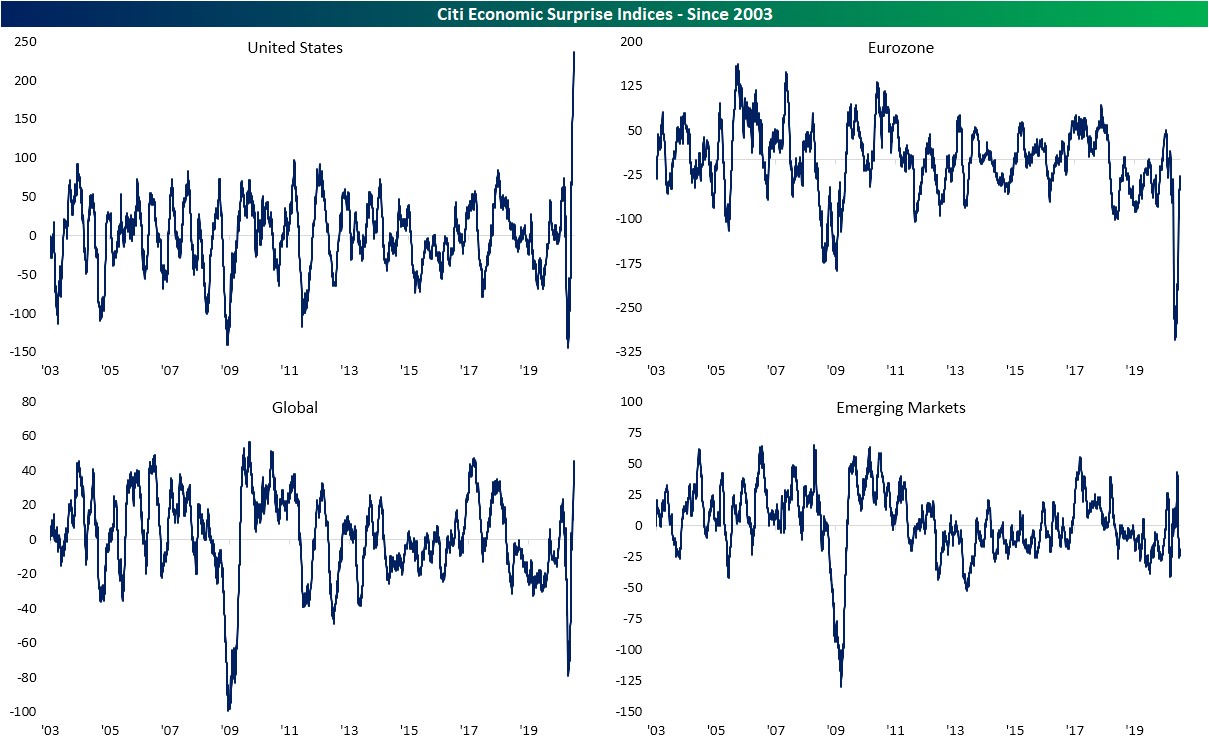

Economic Surprise Indexes Are Still High

Citi Economic Surprise index for America is at a record high as the chart on the top left shows. Some have been calling for it to drop for a couple weeks now. At first, we thought it would drop because expectations would match the improvement. We need 2-4 weeks to see what happens.

It’s also possible that because America hasn’t dealt with COVID-19 as well as most other countries, the expectations are lower for the recovery. Even though Europe has dealt with the virus much better than America, the Eurozone still has a negative surprise index as the chart on the top right shows.

Maybe those countries dealt with the virus better, but reopened slower which hurt them in the short run. Emerging markets are in between the two as their Citi surprise index is solidly positive.

There are all sorts of theories on markets because the rally in U.S. stocks this summer has confounded the economic data and the virus. Some believe that large caps have rallied because of their international exposure. Big internet companies are global, meaning they get most of their sales from outside of the country. That ties in with the large caps outperforming the small caps which are domestic.

It’s counterintuitive to bet on the global economy by buying U.S. stocks. American markets outperforming the rest of the world because the rest of the world is doing well probably isn’t how many people view this. This many not be the correct outlook, but it’s not commonly discussed.

Earnings season is getting started this week with the banks releasing results. Next 2 weeks will be the meat of the reporting season. So far, 26 S&P 500 firms have reported results. 77% have beaten EPS estimates with growth of -44.87%. That’s the deadly drop the stock market forecasted back in February and March. This rally is forecasting an improvement in 2021.

We will need to wait and see how that prognosis turns out. 73% beat sales estimates with -6.68% growth. This recessionary earnings season has had a massive decline in margins. Blended estimate for Q2 EPS growth is now -44.11%.

Redbook & Chase Data

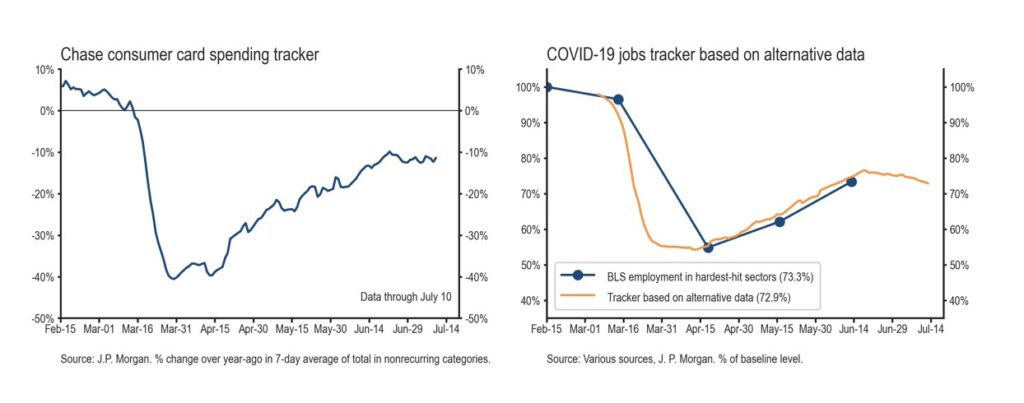

It seems over the last several weeks that the consumer has turned negative. Redbook report from the week of July 11th showed some improvement. Growth went from -6.9% to -5.5%. There is unlikely now an improving trend, but that might occur later in the month. We have 3 factors in play.

First is the potential for COVID-19 to improve in the next few weeks. Second is the July 25th end date for the extra $600 in weekly unemployment benefits. Third is the potential for another stimulus. There isn’t one about to be voted on though.

Can the labor market make up for the lack of benefits? As you can see from the chart on the right, alternative labor market data, which has successfully predicted the hardest hit sectors in the BLS report, has weakened in the past month. Maybe, if the south and western states fully reopen in August or September, we can see the recovery pick up again. The stock market is certainly starting to project that with the tech stocks underperforming this week.

Retail (industry) investors haven’t ignored the stagnation in consumer card spending growth. TJX stock has fallen 10.2% since June 16th. Maybe it’s pricing in weakness from the ending of the unemployment benefits. If more news reports on vaccine trials going well come out, consumer sentiment might perk up, following the overall stock market.

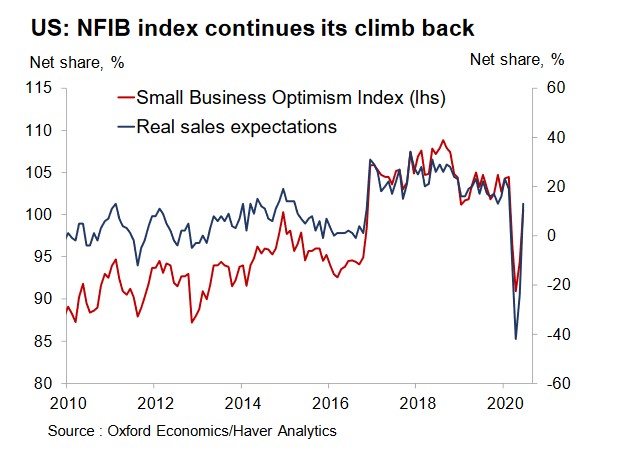

Small Business Confidence

NFIB small business confidence index has had a V shaped recovery. June reading rose from 94.4 to 100.6 which beat estimates for 96.7. We are still looking at backward looking data that doesn’t account for the spike in COVID-19 cases. Investors are expecting the July sentiment reading to weaken. That being said, we must review what we have.

As you can see from the chart below, the net expectation for real sales to be higher had a massive 37 point jump. On the other hand, the earnings trends index fell 9 points to -35%. On the positive side, the net percentage saying now is a good time to expand and the net saying there will be more job openings rose 8 points and 9 points to 13% and 32%.

COVID-19 Green Shoots

Just as predicted, the 7 day average of new deaths per day got above 750 on the 13th. On Tuesday, it fell from 752 to 743. Many people have been predicting a big spike in deaths because of the spike in cases in June. So far, we have only seen a minor blip. If we don’t see a further increase in the next week, we can write off a major burst occurring. No one was predicting a new high, but they were predicting more of an increase than this.

Obviously, it’s good news that the worst fears haven’t come true. Other good news is it looks like the number of new cases per day in Florida has peaked like we said would occur. Following the 15,300 data dump, there were 12,624 on Monday and 9,194 on Tuesday. At this rate, the 7 day average will start to come down in a couple days.

It’s not all good news though as there were 11,060 new cases on Tuesday in Texas which was slightly below the record of 11,394 on July 9th. An emerging story had been that Arizona was successfully dealing with COVID-19 as the number of new cases had been falling. However, there was a spike to 4,273 on Tuesday which was the 3rd highest ever.

All the latest news on cases and deaths might be less relevant if the news on a vaccine continues to show promise. News on Tuesday was that Moderna’s vaccine showed all 45 recipients produced antibodies to fight the virus which furthered the excitement. Moderna’s stock rose 16% after hours on this news.