How Is The Consumer Doing?

Data suggests that August was a mixed bag for the consumer despite the 6 year low in confidence. Frankly, a mixed bag is good when you consider most unemployed people lost $600 per week. That’s $2,400 on the month. Some people got their jobs back this month as continued claims fell. Unemployment rate definitely fell below 10%.

Plus, people in a few states started getting $300 or $400 in weekly benefits. Slowing growth improvement isn’t bad if you think spending is going to spike once Abbott’s testing allows people to go back to normal. We could see a massive economic expansion this fall. The market has started to price this in as the JETS airline ETF is up 5.8% in the past 2 days and 10% in the past week. You’ll know testing is going well if this ETF rises above its June 8th peak.

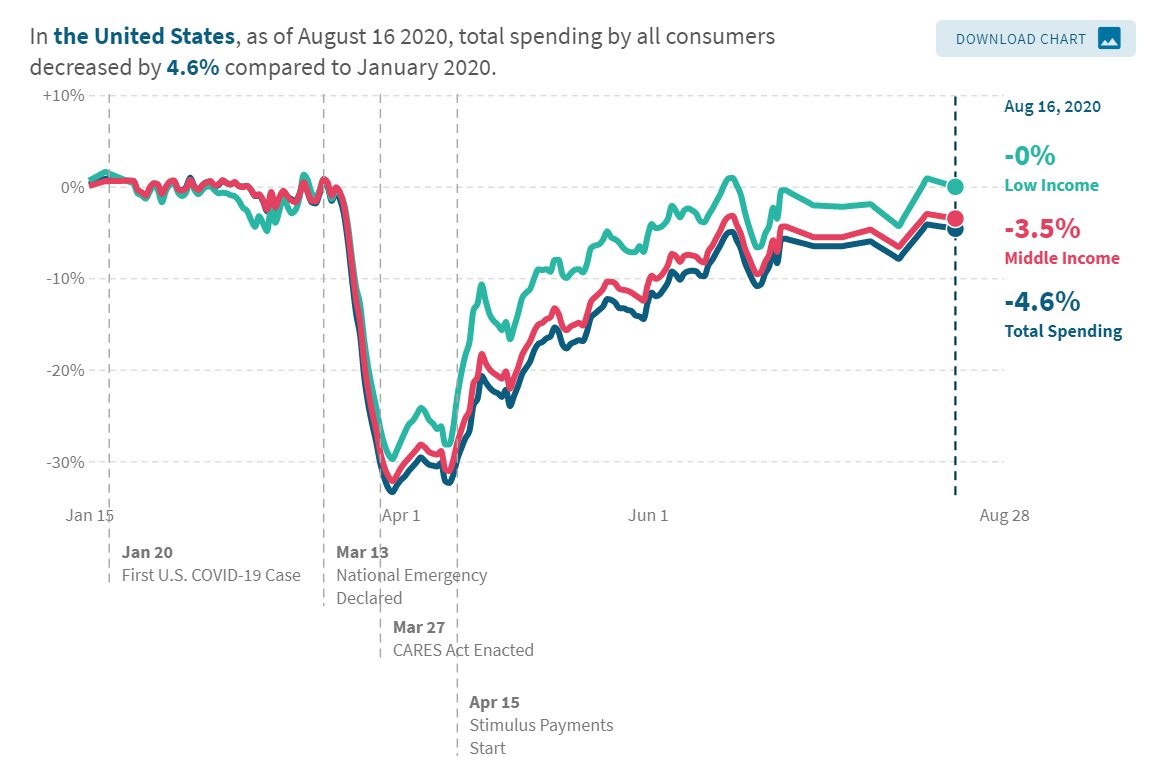

As you can see from the chart above, total spending by all consumers was down 4.6% in the week of August 16th as compared to January. Low income spending is back to the January level because low income unemployed people made more money not working. Lower income people also got the most stimulus money. Middle income spending is down 3.5% from January. That implies upper income spending is down over 5%.

Upper income people aren’t doing poorly. They are being helped by the record high stock market. Their spending has declined because a lot of what they spend money on hasn’t been safe such as flying and hotels. If the risk of COVID-19 diminishes significantly this fall, they can go back to spending like they used to. Only problem would be if a crash in tech stocks causes their net worth to fall. That would be a particular issue in Silicon Valley.

Consumer Sentiment Stays Weak

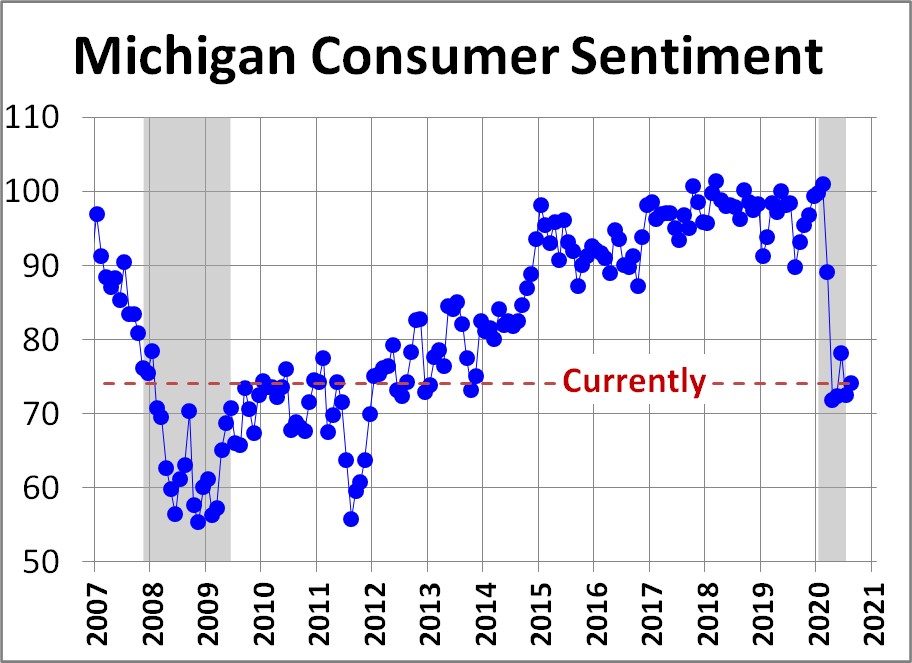

Since we just got a disappointing consumer confidence report, expectations for the consumer sentiment reading were low. This report beat the lowered estimates as the index rose from 72.8 to 74.1 which beat estimates for 72.8 and the highest estimate which was 73. As you can see from the chart below, this was still a weak reading as it’s in the range it was in from 2012 to 2014. It’s not as bad as the financial crisis because of the stimulus.

Specifically, current conditions rose 1 tenth to 82.9 which is a 21.3% decline from last year. Expectations rose from 65.9 to 68.5 which is a 14.3% decline from last year. 90% of consumers viewed the economy as being in a negative state in August. However, half of consumers anticipated an improvement in the economy. 62% said the economy was unfavorable.

The report stated, “Although strong gains in consumer spending from the 2nd quarter lows can be anticipated, those gains will significantly slow by year-end without some additional fiscal spending programs to diminish the hardships faced by unemployed workers, small businesses, as well as support for state and local governments.”

Some disagree with this because if increased testing in September allows people to go back to normal, many jobs will come back. We could have a major cyclical upswing sometime this fall even without more stimulus.

July Income & Consumption Update

July was a good PCE report because the consumer was less supported by the government and it still performed fine. A theory many economists have is by August and September, the consumer will be showing the negative impacts from the decline in stimulus. That depends on how COVID-19 testing goes. Before Abbott’s release, stimulus was needed badly. Now with the $300 in weekly benefits going out and a potential return to normalcy this year, a stimulus is less necessary.

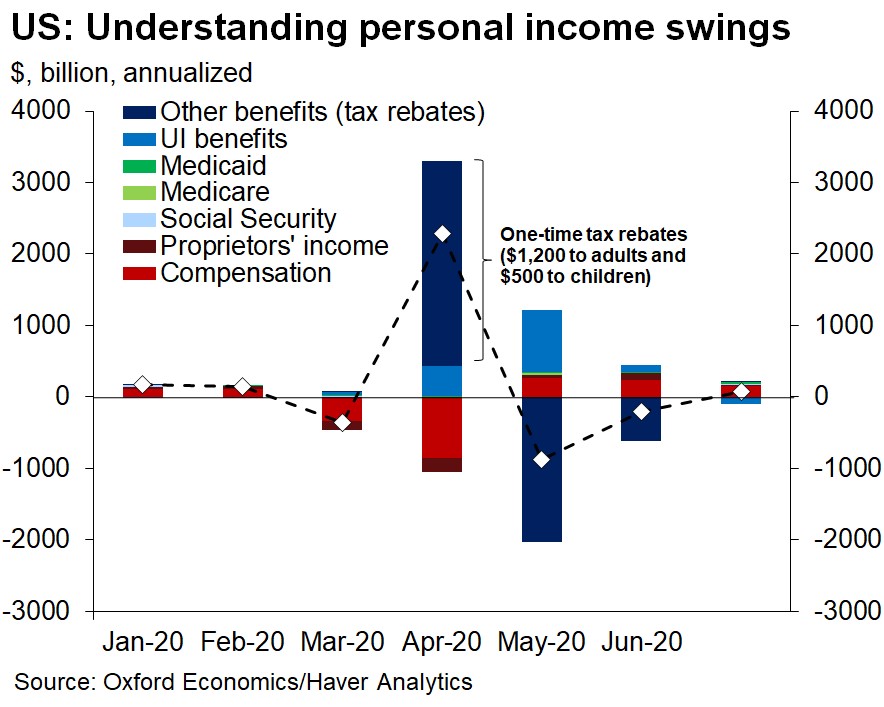

Specifically, income rose 0.4% as wages improved, offsetting the decline in unemployment benefits. Disposable income was up 0.2% as it’s still above pre-COVID-19 levels. Real disposable income was down 0.1%. To be clear, the $600 in benefits were given out in July, but less people got them because more were working. The chart below shows compensation was the biggest positive factor on income. That’s the way it needs to be for this recovery to have legs.

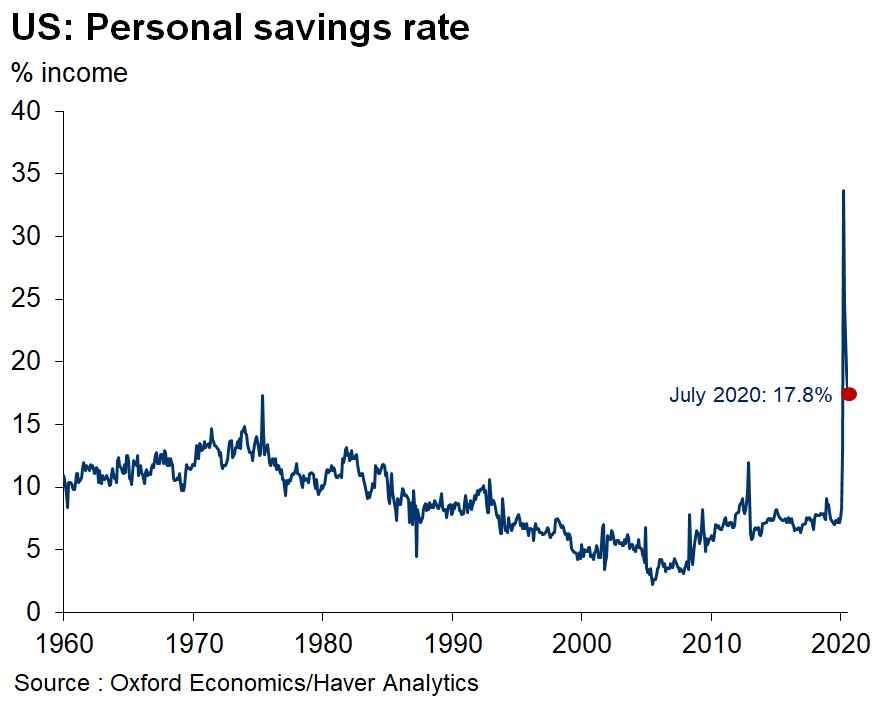

Consumer spending was up 1.9% and real spending was up 1.6%. As you can see from the chart below, the savings rate fell 1.4% to 17.8%. We want the savings rate to fall because consumers are confident, not because they can’t afford to save. When the money comes from the government, people generally save it at a higher rate than when they get paid from working.

As more people get their jobs back, the savings rate will fall. We need the economy to go back to normal for people to go back to spending money on vacations (flying & hotels). There are also small purchases that will increase again when things go back to normal such as perfume, office furniture, and breath mints.

Inflation Was Low Again

Headline PCE inflation was 1% which was up from 0.9%. Core PCE inflation was 1.3% which was up from 1.1%. That’s the highest rate since March. Fed talked about how it won’t raise rates for years, but inflation is still below its target anyway. It will be tougher to avoid hiking rates if inflation rises above 2% next year.

That being said, very easy comps next year will make above 2% inflation basically meaningless. The only way we will see guidance shift is if the unemployment rate falls significantly.

It would be interesting to see the Fed’s stance if Abbott’s testing gets the economy back to normal. In that case, we could have mid-single digit unemployment next year and heightened inflation. Fed is talking tough in terms of dovishness now, but the economy is still being held hostage by the virus.

If it goes away, the Fed should take back its statements. Labor market should recover from this recession faster than last cycle. Why keep rates at zero for 5 years if that’s the case? Bond market is starting to catch on to the recovery as the yield curve has been steepening.