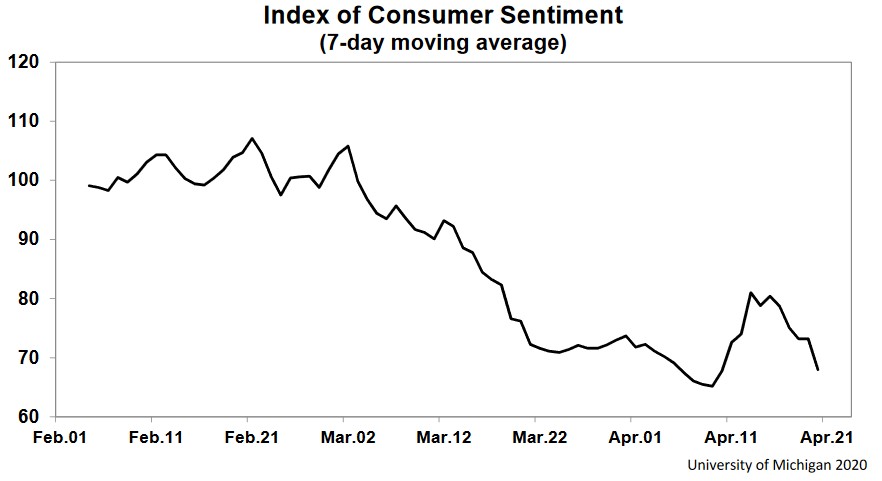

Consumer Sentiment Improved Slightly

As expected, consumer sentiment improved slightly in the second half of April. That’s because it already fell so much in the first half of the month and because stocks rallied. Bad news is the initial spike in mid-April has worn down. That’s probably because stocks stopped increasing at a quick pace and because people are realizing the spike in stocks doesn’t correlate with the economy in the near term. The labor market is the worst since the Great Depression.

Unless stocks have another spike like the one in late March and early April, which they won’t, the sentiment index will likely hit a new low. You can see in the chart below, the 7 day moving average has already begun to fall again. That being said, we are closer to a bottom than we are to the top. Just like how stocks can’t rise as quickly as they previously did, this index can’t fall as quickly as it has. It’s simply math. It would hit zero quickly.

Specifically, overall sentiment index was 0.8 higher than the preliminary reading. That means the index fell from 89.1 to 71.8. That’s still a record setting decline. Households with below median incomes expressed the same level of confidence as those with above median incomes. This virus is affecting everyone.

Usually, the poor are hurt more by recessions than the rich. But with the help of unemployment insurance, those making near the minimum wage are actually making more money than they would be if they were working. This merging of sentiments happened because those with above median incomes saw a 19.8 point decline which is more than the 14 point decline from those with below median incomes.

Working poor are actually making more money. People who are getting unemployment checks are saving more of the money than they usually would because of the current uncertainty. Plus, there are fewer ways to spend money with everything shutdown. There’s a possibility they won’t find a job before their benefits expire. If the majority of the labor market is still in trouble, the benefits will be extended.

However, individuals don’t know this. Plus, they could have a tough time finding a job even if the labor market improves. A gap between current and expected conditions fell from 22 points to 4.2 points. Consumers didn’t lose much optimism from March. Optimism in May will be determined by how quickly states reopen their economies and how well it goes.

Does Reopening Matter?

Reopening the economy matters, but there is no way to make the economy recover quicker because consumers and business owners are smart and cautious. There are already numerous Georgian business owners that have said they don’t plan to open when the state allows it.

Furthermore, the places that do open won’t see many customers. Adding a third layer to why the economy won’t improve much is that there are sharp restrictions on opening. Georgia has gotten a lot of criticism about reopening, but the reality is this is a “reopening in name only.”

If the state says it is reopening, but makes it tough to reopen and firms don’t want to do so anyway, nothing will happen. This is kabuki theater which is to say it’s fake. As you can see from the survey above, 71% of consumers said they wouldn’t go to a bar or restaurant if the restrictions are lifted. 85% said they wouldn’t get on a plane and 87% said they wouldn’t go to a large event.

Why would a business reopen if their customers aren’t coming, their employees are at risk, and there are extreme restrictions on how they operate? Answer is they won’t reopen. It's getting ahead of the game to not to expect such a weak response when New York opens. When New York opens the situation will be safer. It will be safer if you work under the assumption that opening 3-8 weeks later lowers the risk.

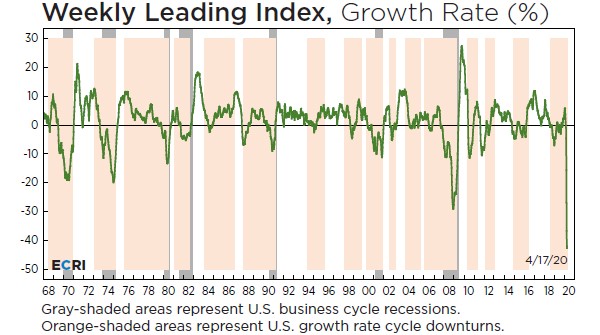

Weekly Leading Index Improves Again

ECRI weekly leading index improved again and the yearly growth rate improved for the first time. The chart below shows the terrible growth rate it’s still at which is far below the trough of the last recession. This recession is far deeper than the financial crisis and might even be deeper than the Great Depression.

However, growth is expected to rebound which is why stocks are higher. The stock market helped push this index up 2 weeks in a row. In the week of April 17th, the index went from 111.3 to 113.4. Yearly growth rate finally improved as it went from -42.5% to -41.9%. We can’t make any predictions about where this index is headed. It largely depends on markets. A minor decline in stocks could cause a new trough in the index.

Record Rate Cuts

Policymakers haven’t done a perfect job at dealing with this recession, but they have done a vastly superior job as compared to the 1930s. Plus, we already had a social safety net in place which prevented things from getting out of hand before the government stepped in. As you can see from the chart below, global central banks have cut rates even further than they did in response to the financial crisis.

Next Fed meeting is on Wednesday the 29th. Some are wondering if the Fed will cut rates to negative. Personally, I am 100% certain the Fed won’t do that because they have already explained it would be counterproductive. Fed seems willing to do whatever it takes.

Since markets have been calmer, Fed is unlikely to unveil any new programs. But it won’t take its foot off the gas pedal this week. Fed will support markets until coronavirus is under control. Personally, I think the Fed will be very dovish for at least the next 6 months. It will keep rates at zero for at least the next year. We can expect dovish language in April’s Fed statement and beyond.