Consumer Sentiment and Spending

Consumer Sentiment - As online shopping gets close to the double digits as a percentage of overall retail sales, the fate of online shopping becomes the fate of the overall market. Since online shopping is growing faster than physical stores, its importance to growth is larger than its share.

On a seasonally adjusted annual run rate, ecommerce sales were up 3.9% in Q2 which is the same as the original growth rate reported in Q1, but 0.3% better than the revised Q1 number. Online sales in Q2 were 9.6% of total sales which is an increase of 0.2%.

The preliminary University of Michigan consumer sentiment report missed estimates. It came in at 95.3 which missed the consensus and the prior report which were both 97.9. It was below the lowest estimate which was 96.

This was the weakest report since September. It is starting to show signs of why the ECRI index is so weak. It’s discouraging to see consumers becoming less optimistic when the stock market is near its record high and the labor market still is strong.

There was no change in the expectations index which was at 87.3. The current conditions index fell about 7 points to 107.8. Much has been made about the relative strength in the current index versus the future index as this differential was similar prior to the last recession.

Consumer Sentiment - The worst case scenario is for the current index to fall just like it did during the last recession.

This weakness in the current index is a bad sign for August consumer spending, but I wouldn’t start worrying about a recession yet. I would be worried about a pull back in stocks since they are near their all time high. The 1 year outlook for inflation was flat at 2.9% and the 5 year expected inflation was up 0.1% to 2.5%.

The weakness in this report was the catalyzed by the bottom third of the income distribution. This makes sense because the top 50% of people own stocks, so they are feeling good as stocks are near their records.

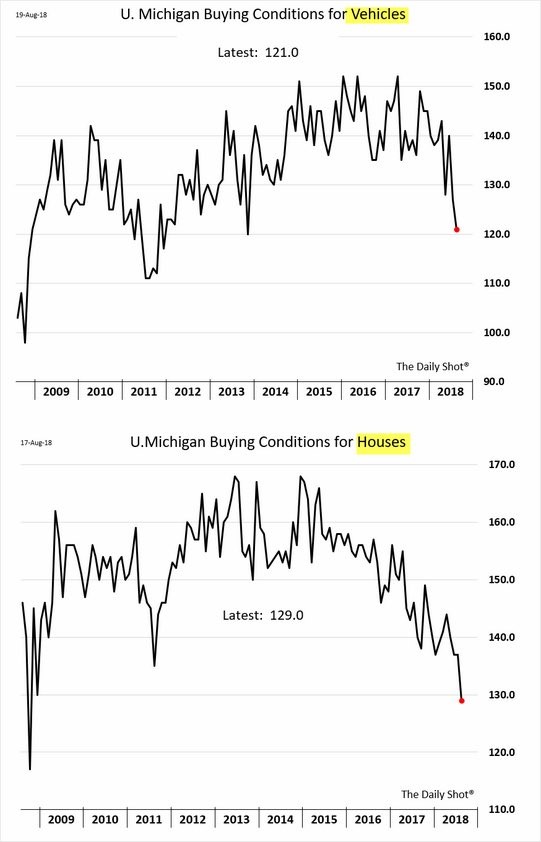

There was a huge decline in the buying conditions for houses and cars. Since these are the biggest purchases people make, they determine the fate of the economy. Buying conditions for large household durables is at a 4 year low and pricing perceptions are at a 10 year high.

This is what happens when it is a sellers’ market for too long.

As you can see from the top chart above, buying conditions for vehicles hit a 4 year low. Pricing perceptions were the lowest since 1984. The bottom chart below shows the buying conditions for houses are even worse as they are the lowest since 2008.

There’s no question this weakness won’t lead to the same size declines in the housing market as last cycle, but strength certainly isn’t on the horizon unless prices come down.

Consumer Sentiment - Disappointing Philly Fed Index

The Philly Fed manufacturing index was 11.9 which missed estimates for 22.5. It was way below the lowest estimate which was 20 and below the prior month which was 25.7. This is the lowest reading in 2 years and is the opposite of the positive report from the Empire Fed.

The new orders index fell very sharply from 31.4 to 9.9 which is its lowest reading in 2 years. Pretty much everything about the current report is bad. The only saving grace is that the future diffusion index increased from 29 to 38.8.

Every single sub index fell except inventories, which means sales were slow so products available for sale increased. The good news is that inflation fell as the prices received index fell from 36.3 to 33.2 and the prices paid index fell from 62.9 to 55.0.

The bad news is inflation isn’t high to begin with even though the regional Fed indexes have had it at near records this year. The calibration is way off since year over year CPI was only 2.9% in July.

Commodity prices aren’t high and wage growth isn’t off the charts. Even though overall inflation isn’t near record high levels, it’s good to see the manufacturing firms in the mid-Atlantic eliminating the capacity constraints they have been under.

It’s important to point out that the Philly Fed index was the first to show signs of improvement in 2016 when the economy was beginning to recover.

It’s bad news to see this leader falling. As I mentioned, the 6 month expectations index increased sharply. The new orders expectations index was up from 28.3 to 38.1. One slightly negative part of the expectations index was capital expenditures fell from 31.4 to 27.1.

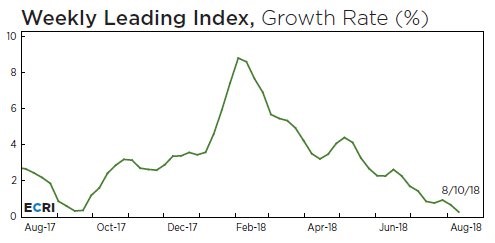

Consumer Sentiment - Leading Index Versus ECRI

The leading indicators are very strong, while the ECRI leading index is very weak. The leading indicators for July, released last Thursday, saw 0.6% a month over month increase.

This beat the consensus for 0.4% growth; the prior month had 0.5% growth. As you can see from the chart below, the year over year growth rate is 6.3%. The year over year leading indicators turned negative prior to every recession since the 1970s.

It looks like the leading indicators may be in the process of peaking, but a slowdown would probably take at least a year before it fell to negative growth. The economy moves slowly.

Consumer Sentiment - The ECRI leading index is following the expectations implicit in the 10 year bond yield.

As you can see, the growth rate fell to 0.3%. Negative growth doesn’t mean a recession is here. However, the year over year growth rate being at a 47 week low certainly isn’t a positive.

The year over year comparisons will be getting easier in late August and September. I don’t expect it to go negative soon.

If it does go negative, the growth rate will likely plummet in October when the comparisons are tougher. An economic slowdown should be obvious by the 4th quarter. The lower it goes, the more likely there will be a recession.