US and European bourses got off to a rocky start on Monday after a largely positive session overnight in Asia.

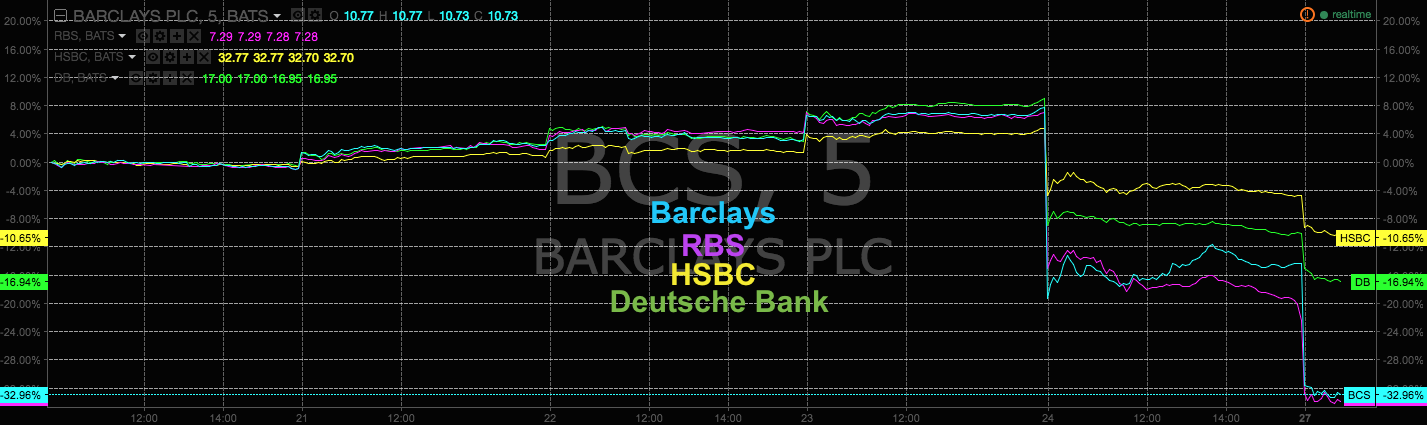

You’ll want to watch financials here, both in the US and (especially) in Europe. Needless to say, markets were already questioning the solvency of some European banks and now, post-Brexit, we’ve got a real problem. Here’s a look at how a few selected names have held up (or, more appropriately, “haven’t held up”) since the vote:

Right. So that’s an absolute, unmitigated disaster. Have a look at the cost of insuring baskets of European financial institution debt:

Note that the scariest thing about that chart is that even after the spike (far right hand side) we’re not even back to wides hit in February. In other words, this likely isn’t even close to being priced in.

This comes as the pound continues to slide. Oil is of course struggling to find its footing and gold continues to outperform on safe haven flows.

Now if you’re purely a trader, all of this isn’t necessarily a bad thing. Nothing like some volatility to create opportunities, right?

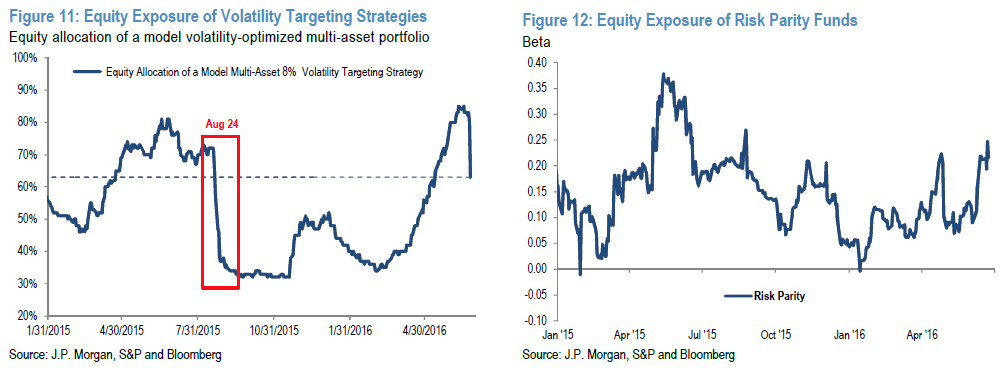

But the problem is, credit markets haven’t begun to price in what just happened and neither have stocks. Sure, the choppy waters will afford you some great trades, but you should be aware that this could get very ugly. Consider, for instance, the following two charts from JPMorgan’s quant team which depict equity exposure of vol. targeting and risk parity strategies going into Brexit:

(Charts: JPMorgan)

Ok, so what in the world does that mean? Well, those are systematic strategies which, in a nutshell, means they are going to be forced to adjust and that means paring down that equity exposure. For their part, JPMorgan says you should expect at least another $100 billion in selling.

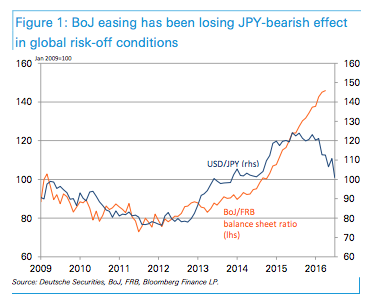

Meanwhile, the Japanese are restless about the yen. Here’s why:

That is an absolute catastrophe for Prime Minister Shinzo Abe and the prospects for Japanese exporters. Markets are expecting an emergency Bank of Japan meeting at which governor Kuroda will announce further easing. But it likely won’t matter. Here’s Deutsche Bank:

“We do not feel that either forex market intervention by Japan or a BoJ easing would have any sustainable weakening impact on the yen. The focus for now will be whether the initial market turbulence calms while the USD/JPY remains above ¥100 on government and BoJ efforts.”

(Chart: Deutsche Bank)

That chart should make you chuckle. What it shows is that BoJ QE has come completely untethered from the yen. In other words: QE is now having the opposite of its intended effect. It’s actually pushing the yen higher. In a sign of the times, Barclays says the currency may shoot to 83 by 2017. And yes, there’s an ETF for that if you’re not into FX trading (it’s ticker FXY).

So that’s where we stand to start the week. US stocks are down meaningfully early on as investors try to digest all of the above. Take advantage of the volatility but please, be careful out there. These are “unique” times we trade in.