Small Cap Value Tanks

The stock market fell again on Monday. It started as a broad based decline, but then morphed into a huge decline for small cap value and a very large reversal for large cap value. For much of this correction in September, small cap value has outperformed. It gave up all that outperformance in a few hours as some worries about COVID-19 in Europe crept up.

It's unclear not what put the market over the edge because COVID-19 cases have been increasing in Europe for a few weeks. In France, the current 7 day average of new cases is 10,116. A spike in cases started in August. In fact, there was a record high in new cases in late August. We're not sure why it took 3 weeks to cause a decline in U.S. stocks.

Also, keep in mind U.S. small caps aren’t big international players. This will only hurt them if COVID-19 comes back to America. We still don’t have a perfect grasp on the situation. There is fear of another wave in America this winter. Some are not big believers in seasons having a big impact on this virus because it got bad in America in July. 7 day average of deaths is falling slowly as it’s now at 768 which is near the low end of the range this year.

Two things are interesting here. Firstly, there are times when the market doesn’t care at all about another wave of cases this winter. Other times it cares deeply. People change their tune when stocks change direction. Secondly, it's confusing why some say a vaccine is the only solution when doctors are also working on better treatment and firms are working on mass fast testing.

A vaccine could be over a year away, but rapid testing is coming in October. Rapid testing is being ignored probably because we haven’t gotten any substantial updates since August 26th when the FDA approved Abbott’s test.

Long Term Trend Change?

There are 2 reasons why the stock market keeps having major factor days in which small cap value and large cap growth diverge by such a large amount. First is COVID-19 is uncertain. Worst case scenario was taken away this spring when we realized the death rate wouldn’t be catastrophic.

Outcomes still vary widely though. Worst case scenario now would be another wave this winter along with future waves without a vaccine. Rapid testing may prevent future waves, but that’s just an optimistic opinion.

Obviously, we know that value stocks do well when COVID-19 is seen to be going away and growth stocks do well when optimism on COVID-19 is weak. That’s why the stock market rises on bad news. In Monday’s case, pessimism almost managed to get the Nasdaq positive.

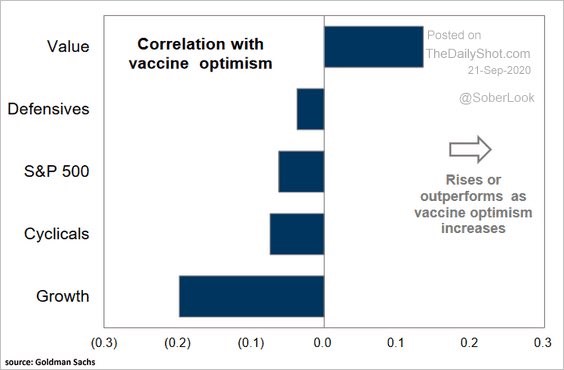

As you can see from the chart below, value is correlated with vaccine optimism. There have been 2 patients with issues in AstraZeneca’s phase 3 trial. Other factors are negatively correlated, with growth being the most negative. S&P 500 is negative because value stocks have a very small weighting compared to growth. Facebook is worth more than all of the energy stocks combined and it’s not even the biggest growth stock.

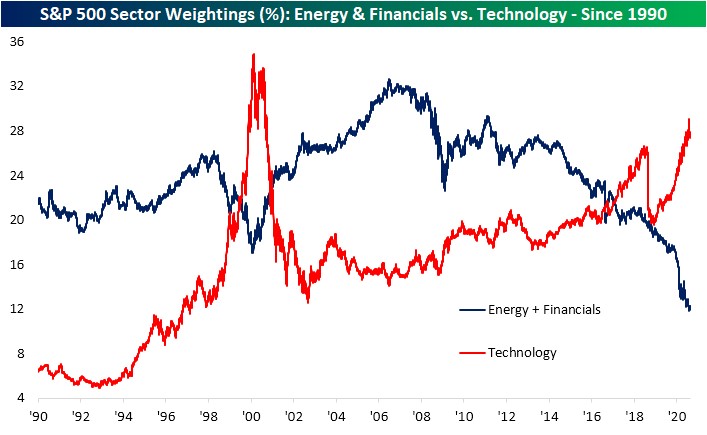

A second reason we have had crazy factor days so often this summer is because the movement has gotten so extreme. We are near the end of a 10 year period where growth has mostly beaten value. COVID-19 accelerated the previous trend to extreme levels. As you can see from the chart below, the tech sector only was a larger portion of the S&P 500 at the peak in the 1990s tech bubble.

Conversely, energy and financials are a smaller part of the market than at any point in the past 30 years. That’s because the internet stocks aren’t just in the tech sector. Furthermore, oil prices and interest rates are low. What would you expect from the banks with interest rates at the lowest point in history and a flattish yield curve?

What would you expect from fracking companies with oil prices in the high 30s per barrel? Fracking can’t exist at these prices which is why EOG stock fell 4.7% to $38.81. It’s down 37.5% since June 8th.

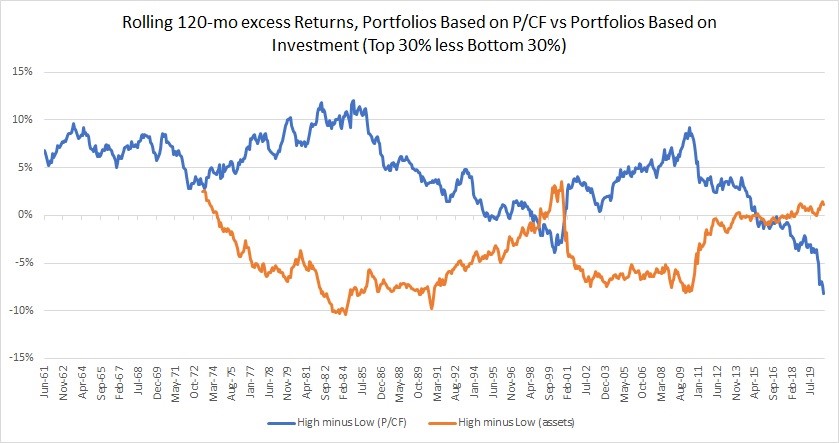

The chart below shows similar information gathered in a different way. As you can see, the rolling 120 month excess returns of stocks with high cash flow yields minus firms with low cash flow yields has gone deeply negative. It’s the worst ever.

Companies growing assets minus those not growing them have great excess returns, but it’s not as good as the 1970s peak or the 2000 peak. Not being as high as the other peaks could be related to the growth in asset light business models.

Review Of Monday’s Action

S&P 500 was down 1.2%, but it was much worse in the morning. There was a 1.6% rally off the low. The market is still down 8.4% from the top though. It hit correction territory briefly during the day. Nasdaq only fell 13 basis points, while the Russell 2000 fell 3.35%. That’s a massive difference.

Banks and small cap value did terribly, while cloud and the Nasdaq 100 were fine after being weak all month. Regional banks fell a massive 4.7% and small cap value fell 4.3%. This was the worst decline since June 11th for small cap value.

Nasdaq 100 was actually up 53 basis points and the cloud index rose a massive 2.1%. That’s 6.8% outperformance over regional banks in 1 day. A big catalyst of cloud stocks was the notion that COVID-19 is getting much worse in Europe as Zoom stock was up 6.8%. It’s now at a record high again. The stock is up 33.5% since September 8th. Is it possible that the cloud stocks have another rally in them?

Tesla helped the Nasdaq 100 as it was up 1.6% because investors are excited for Battery Day. However, the stock fell 5.9% after hours when Musk said the battery technology unveiled won’t be in serious high volume until 2022. Musk is usually late for deadlines. If he’s already pushing it back now, imagine how long it will actually take to produce these batteries. It could take years. Finally, Nikola’s chairman resigned which caused the stock to fall 19.3% because he is the enthusiastic founder.