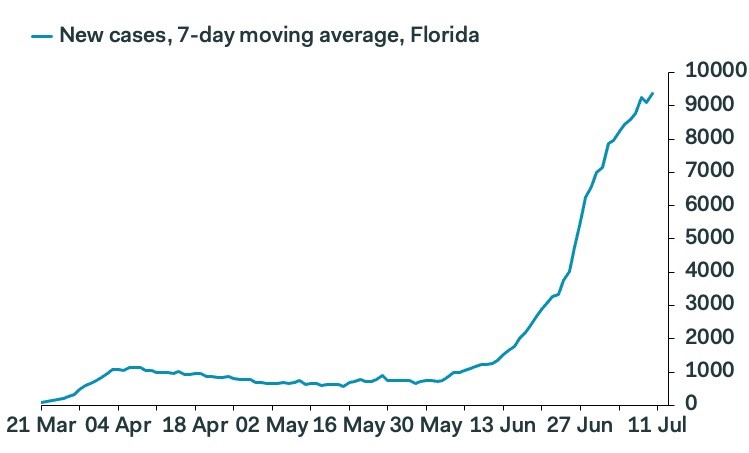

Record New COVID-19 Cases

Unfortunately, even though it seemed like the number of new COVID-19 cases per day was starting to show slower growth, that gave off false hope as the number of new cases lurched to a new record by far on Friday, increasing to 71,787 from 61,067. The likelihood of a complete shutdown in the south is increasing. The chart below shows the huge spike in cases in Florida as there were 11,433 on Friday.

7 day average of national tests that came back positive increased to 8.7% which is the highest reading since May 10th. We all keep expecting that percentage to fall, but it doesn’t. There were 51,544 new hospitalizations which was the highest since May 2nd. 7 day average of daily deaths increased to 657 which is the highest since June 19th. It’s very clear my projection for 750 will be hit.

There is a potential false narrative that because the cases are among young people and care has gotten better, this spike in cases isn’t a big deal. That may be the wrong context. If older people were getting this and the care didn’t get better, it would be one of the biggest catastrophes in American history.

Instead we have a stubborn problem which is forcing the economy to slow and more people to die from other reasons than the virus. It’s still very bad news. Optimism from May and early June was incorrect which is why most stocks are below their June 8th high. The market is increasingly being driven by a few speculative large cap stocks that aren’t trading on fundamentals.

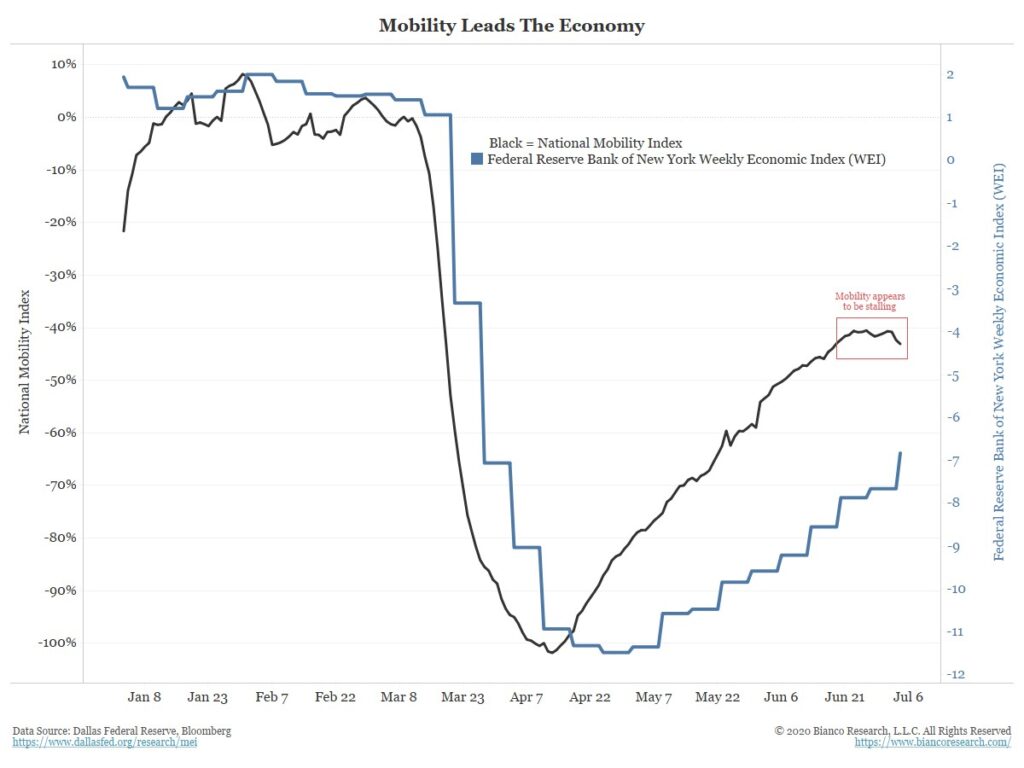

Mobility Takes A Hit

Because COVID-19 is the main reason the economy slowed in February, March, and April, and its decline is the main reason growth recovered in May and June, mobility is a leading indicator for the economy. It leads the NY Fed’s weekly leading indicator as you can see from the chart below.

And it’s not a surprise in the least bit that fewer people are traveling. It’s good for the long term if fewer people travel because that will slow the spread of COVID-19. Once COVID-19 is fully combatted, the economy can get back on track. We could have a strong recovery in 2021.

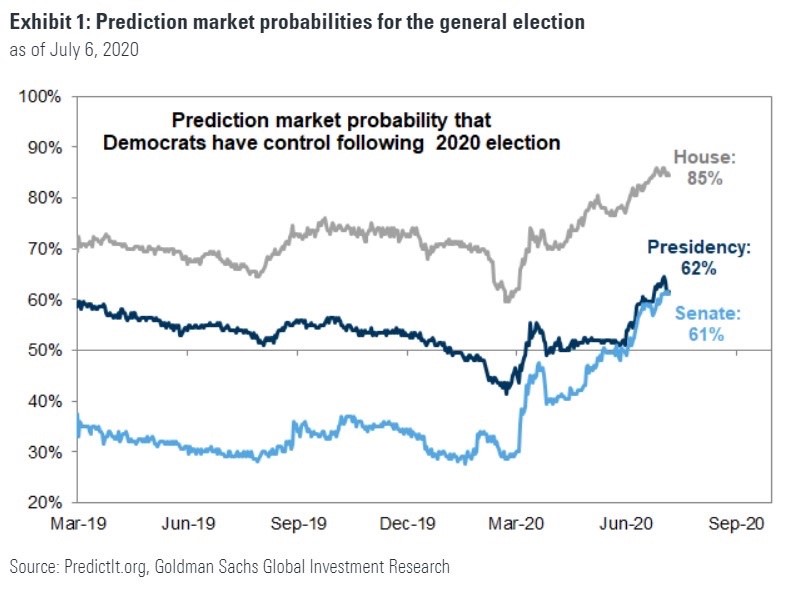

Some Prediction Markets See Democratic Victory

Investing isn’t about expressing political views. You express those views when you vote. When you invest, you measure risk regardless of who you support. A spike in COVID-19 cases seems to have boosted the odds Democrats could win Congress and some even think the presidency in November. Not only is the S&P 500 rallying in the face of COVID-19 and the economy getting worse, stocks are also doing well in the face of higher taxes and higher anti-trust issues.

Specifically, a few betting markets on July 6th said there was a 61% chance the Democrats would win the Senate. The Senate is the main sticking point. Some believe the Democrats will win both the House and the Presidency. An issue with separating odds is usually elections go one way. It's uncommon for many people split their ticket, which is voting for Biden and a GOP Senate or vice versa. But it has happened in the past.

JP Morgan’s election EPS analysis mentioned how the Democrats could lower tariffs on China, but they ignored the possibility of increased restrictions on the top internet names which increasingly control the market. If they all fall, the S&P 500 will collapse.

In previous years, investors have stated these tech stocks weren’t in a bubble and couldn’t crash the stock market. Everything has changed in the past 3 months as they have rallied enormously. Top 5 companies make up 25% of the S&P 500 and have catalyzed most of the gains in the past few months.

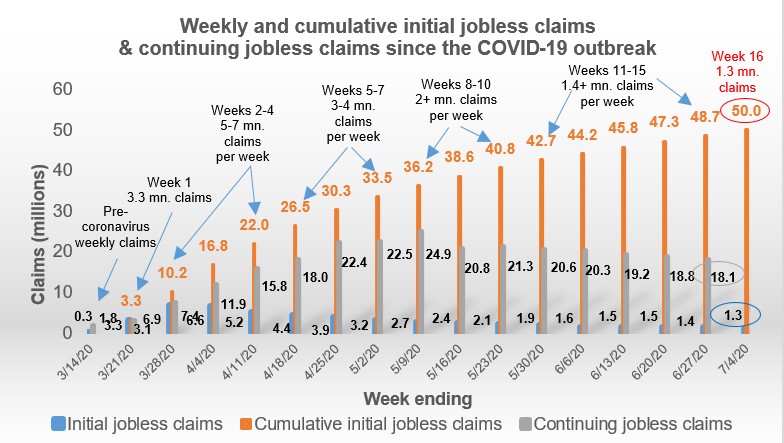

Jobless Claims Were Still Problematic

Headline initial claims figure improved in the week of July 4th, but the all in total of jobless claims stayed elevated. Labor market is still in a bind. This is not a good time for the economy to stop improving. A rally in the Nasdaq does basically nothing to help the real economy.

Specifically, initial jobless claims in the prior week were revised lower from 1.427 million to 1.413 million. They fell in this report to 1.314 million which was below the consensus of 1.375 million. That’s actually a much improved number. Claims fell 7% after the previous week was downwardly revised. This 7% drop is the largest decline since June 6th. If the economy continues at this pace, we could get below 1 million claims around the end of the summer.

As you can see from the chart above, there were 18.062 million continued claims in the week of June 27th which was down from 18.76 million. This was a 3.7% decline which was the largest in 2 weeks. Since continued claims make up the bulk of all claims, you can start to get the idea of why all in claims barely fell.

There were 42,000 more PUA claims which brought the total to 1.04 million. There were 2.4 million total claims which was down 3% from last week. The prior 4 weeks of data show a 1% decrease, a 5% and 6% increase, and now a 3% decline. That’s collectively almost no change in 4 weeks which is bad because the unemployment rate is in the low double digits.

Implied insured unemployment rate is 12.4% which is slightly above the June misclassified rate of 12.1%. We don’t have a good tell of what the July reading will be yet, but it’s certain that there will be fewer jobs created than there were in June because even if the economy kept improving, it would have likely been lower. There are fewer people who can easily go back to work.

PUA claims as a percentage of total claims keep increasing. An obvious elephant in the room is that the extra $600 in weekly benefits will go away on July 25th. There is now almost no chance they will be extended. There’s always a chance another stimulus is added especially if the economy sags further. A rise in the stock market unfortunately is making it look like the economy doesn’t need a stimulus even though workers will need help.