Fed To Buy Individual Corporate Bonds

On Monday afternoon, the Fed announced it would buy individual corporate bonds to create a portfolio based on a broad diversified market index of corporate bonds. This caused stocks to rally about 1% on Monday which was weird because nothing was added to the stimulus.

To some, it looked like stocks were already in rally mode; this was just an excuse for stocks to go even higher. It’s worth reviewing this announcement because it’s not enough to just listen to the market’s reaction and assume it was a new stimulus.

This was a modest adjustment in the way the Fed plans to carry out the process. It’s not as if the Fed didn’t like the Thursday stock market correction and decided to buy a few firms’ corporate bonds to juice the market. It wouldn’t be surprising if the Fed was surprised to see this boost in stocks because it’s just doing what it said it would do. This is similar to a stock rallying because the firm announced the details of its annual meeting.

Fed is creating its own index, so it doesn’t need to rely on an index like the HYG which might trade at a premium to net asset value because traders know the Fed is buying it. Fed will be able to buy a few more bonds than it otherwise would. It’s more transparent. Plus, the market doesn’t need to start guessing which firms will be in and out of the ETF. The Fed is covering itself for when it gets questioned by Congress why it bought certain bonds.

Let’s look at the qualifications which are similar to the announcement months ago. Eligible bonds must have been at least BBB- rated by March 22nd. If they were downgraded subsequently, their rating can’t be worse than BB-. Maturity must be less than 5 years and no bank bonds are included.

Firms that aren’t headquartered in America or firms that got funds from the CARES act don’t qualify. Firms in the travel industry like airlines got money from the CARES act. They can’t be helped here. Fed won’t buy a fixed income ETF trading below its net asset value.

In summary, this latest Fed statement didn’t change anything. Stocks wanted to rally, so they did. We can never know what they would have done without this news, but it's likely they would have gone up. A gap up in the afternoon made it look like the Fed’s announcement was a big deal, but it wasn’t.

Data Beating Estimates

The stock market was in the perfect situation in late March and April as the economy began to recover. Once the market knew that the virus would rescind and the economy was about to recover, stocks ramped higher. Markets didn’t need to wait for improved data because we got improved COVID-19 data from Italy. That implied we would see a recovery too.

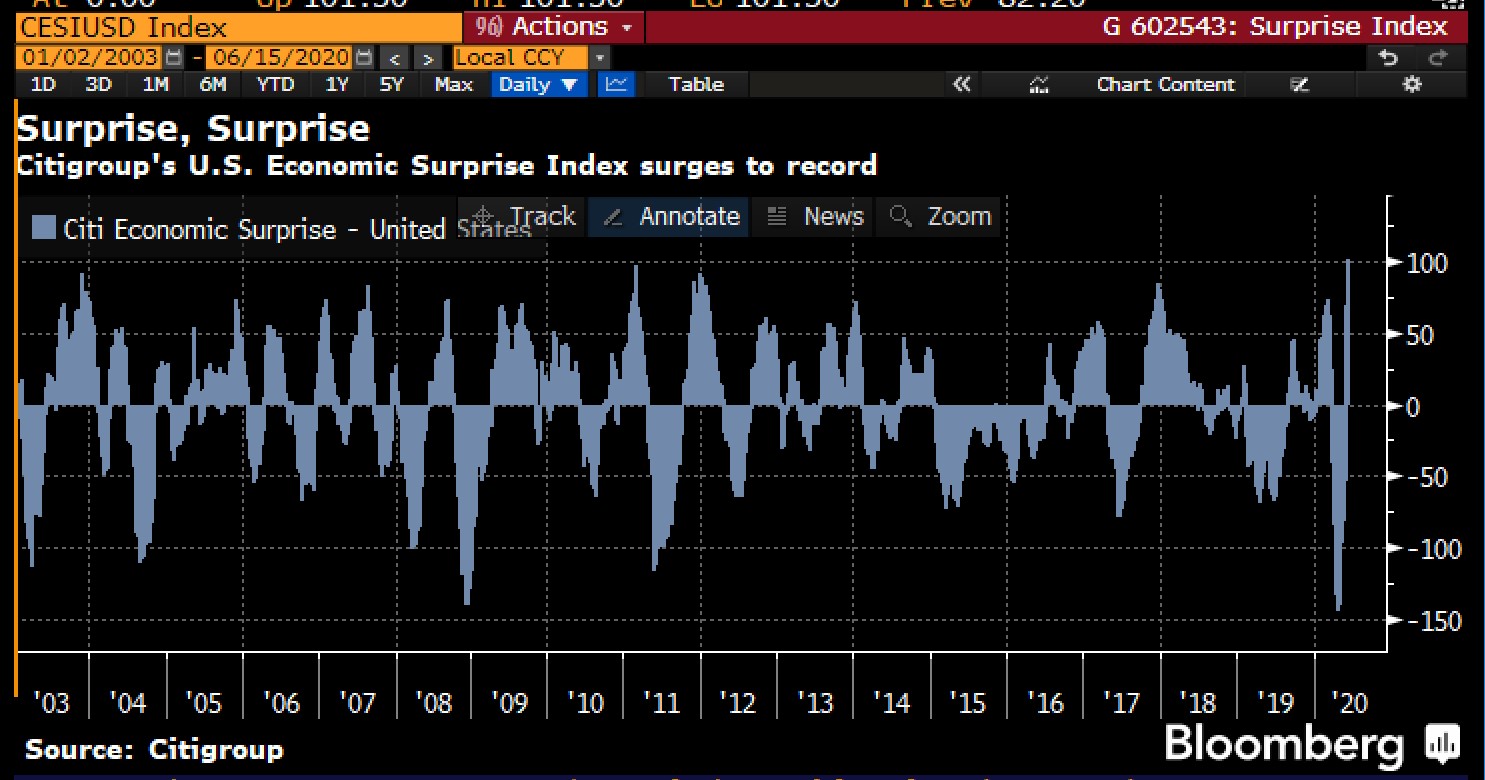

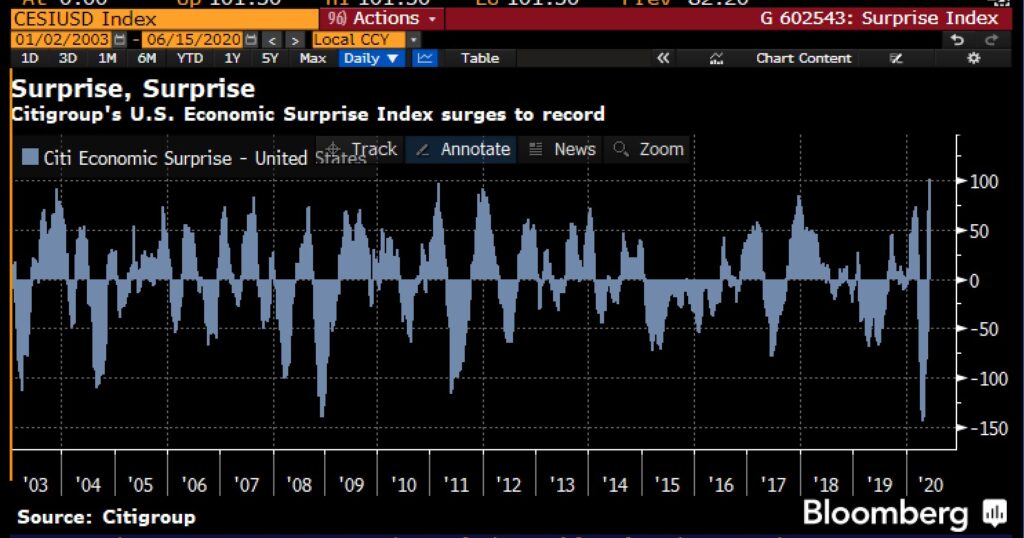

It’s amazing how long ago the market rallied; improved data is only starting to come out now. Traders front ran the improvement by a couple months. As you can see from the chart below, the Citi economic surprise index hit a record high. This indicator goes back to 2003, so that’s really impressive.

Starting in late May and early June, we were in a different situation because of how high stocks had gotten. Buy the hype, sell the event. Stocks bottomed as NYC shut down and now they may have topped as NYC reopens. Economic surprise index literally can’t get any better.

Economists will raise their projections for June which means data won’t beat estimates by as much or as often. This initial rally was so strong, we don’t see much intermediate term upside from that peak. Similar to how the January 2018 peak still is critical to the chartists. Don’t buy peak hype even if it doesn’t seem like a bear market is coming soon.

Consumer Looking Better

Yes, the consumer is doing well now, but if the unemployment benefits go away, that can change. Things are looking really good in rate of change terms, which is what the market likes. The best situation is when data goes from terrible to less bad. That’s what we have now. In the latest Gallup survey, the percentage of consumers saying the economy is excellent or good rose 1 point to 23%.

Frankly, we don’t get how 22% said the economy was excellent in May, when it was clearly in the toilet. You can never have a survey where everyone is negative. Percentage of consumers saying the economy is getting better rose 2 points to 33%. The low was 22%.

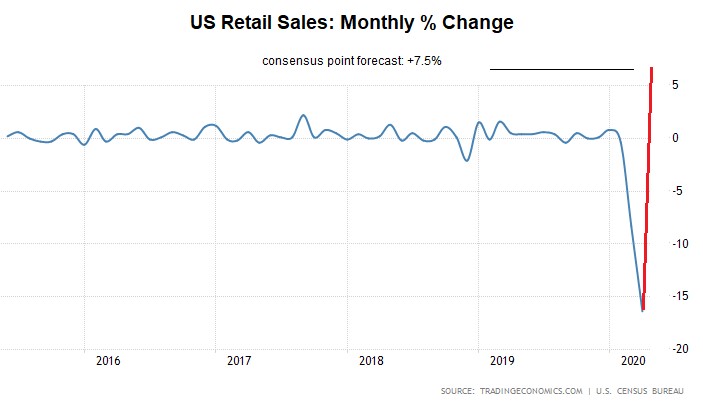

The chart below shows the expectations for a massive bump in monthly retail sales growth because of the easy comp. Growth is expected to spike from -16.4% to 7.5%. As you can see, the expectations are starting to get harder to beat. Stocks will fall if the data starts to consistently miss. At the least, data won’t beat estimates by as much as it has recently because it has never beaten estimates by more in 17 years.

Best & Worst Areas Of The Labor Market

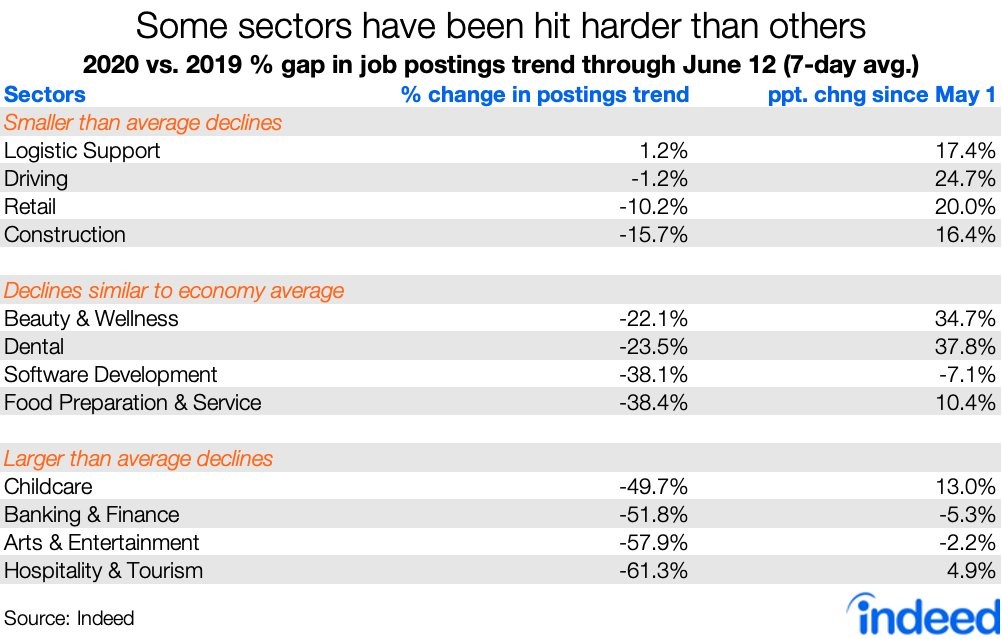

The table below shows the best and worst parts of the labor market. Logistic support had a 1.12% yearly gain in job posting through June 12th. That’s obviously because more people ordered goods online during the shutdown.

Gains in dental have been absurd as growth in postings since May 1st have been 37.8%. Dental gains were so strong in the BLS report, people didn’t think it was real. We're guessing the PPP money was put to great use.

On the negative side, the biggest decline in postings compared to last year was in hospitality and tourism. Even as the economy reopens, people are still limiting travel. Biggest decline since the start of May was in software development. That’s bad for overall wage growth because that’s a high paying industry. It’s amazing to see this weakness because of how well the cloud stocks have done.

1 Comment

Rami

June 17, 2020What about the elephant (debt) in the room? Whats the exit plan from all the landing? The market is loaded with risk naked and afraid...thanks