Banks Underperform

The best two sectors were consumer discretionary and energy which increased 0.59% and 0.57%. The communication services index was up 9 basis points in its second day.

Worst sectors were utilities and consumer staples which fell 1.22% and 0.73%. This action is related to heightened interest rates. It’s interesting to see that the S&P 500 bank ETF has underperformed the S&P 500 in the past few months.

Financial sector was down 0.38% on Tuesday and is up 2.24% in the past 6 months. The S&P 500 is up an astounding 9.81% in the past 6 months.

Banks Underperform - S&P 500 Falls Again

Near term bearishness heading into the weak has proven accurate so far as the S&P 500 fell 0.13% and the Dow fell 0.26% on Tuesday.

On the positive side, the Nasdaq was up 0.18% and the Russell 2000 was up 0.2%.

The CNN Fear and Greed index fell 6 points to 64 which still signals greed.

Banks Underperform - Nike Falls After Hours On Revenue Miss

The biggest news on Wall Street was Nike’s earnings as the stock fell 3.52% after hours even though revenues were up 10% to $9.95 billion and profits were up 15% to $1.1 billion which beat estimates.

Revenues missed by a very minute $10 million and EPS beat estimates by 4 cents coming in at 67 cents.

Even though the revenue miss was small, the stock’s momentum heading into the report caused it to crater after hours. The stock was up 33.55% year to date.

Now that Nike has reported earnings, 9 out of 11 firms have beaten EPS estimates on 25.45% growth. 7 out of 11 firms beat sales estimates for 11.6% growth.

Even though more firms have recently beaten sales estimates, the overall growth rate declined slightly. These are great results, but they’re not enough to make a judgement on the overall market. It’s only about 2% of the index.

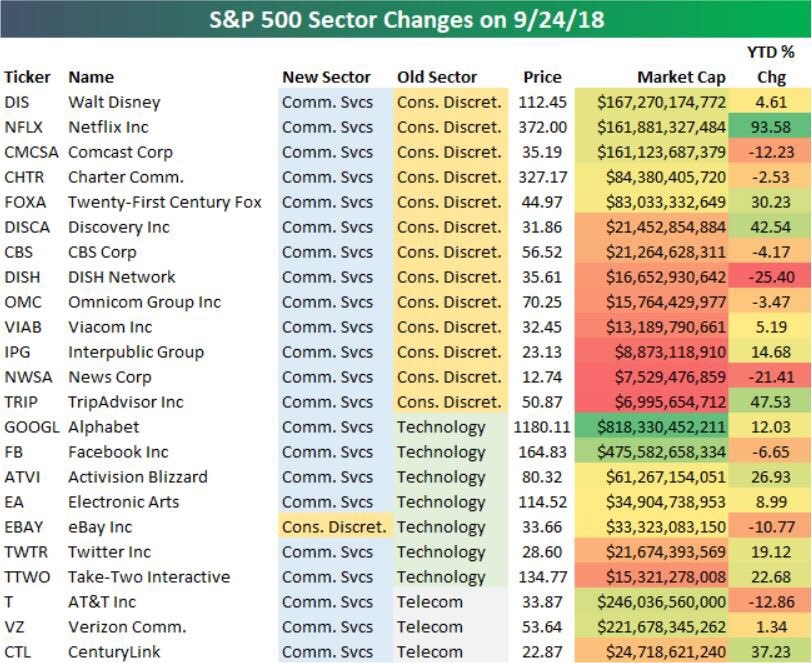

Banks Underperform - Sector Changes

As I mentioned, the new sector changes were implemented on Monday. The table below gives you a complete look at the changes.

It’s quite amazing to see Netflix has a higher market cap than Comcast. Comcast had $21.735 billion in revenues in Q2 and Netflix had $3.91 billion in revenues in the same quarter.

Investors are paying up for Netflix because of its growth potential. Netflix is a beloved brand while Comcast is hated. This gives Netflix an edge when it comes to releasing new services or expanding current ones.

CenturyLink was the biggest mover on this list as its stock fell 8.08%. This was because its CFO Sunit Patel left the company to oversee the T-Mobile Sprint merger.

Banks Underperform - Treasuries & Fed Decision Day

Neither the 10 year yield nor the 2 year yield moved on Tuesday as they are now at 3.09% and 2.83%, making for a 26 basis point difference.

The treasury market is especially important to watch this week because of the Wednesday Fed meeting. Current odds are for 100% chance of at least one hike and a 5% chance of 2 hikes.

Odds for at least 2 more hikes this year are 82.2%. I’m expecting a hawkish hike based on the futures market. If there is a dovish hike, the 2 year yield will fall.

I think stocks will have a very modest relief rally unless something unexpected, like 2 hikes or no hikes occurs. It will be interesting to see what the Fed says about the latest actions on the trade war front.

Banks Underperform - More Tough Trade Rhetoric

President Trump gave a speech on trade where he reiterated his position.

He highlighted the trade deals with South Korea and Mexico while mentioning the lack of fairness other countries such as China have shown to America.

He said America “will no longer tolerate abuse.” The chief market strategist at Prudential, Quincy Krosby stated, "This is going to be a long process. Until it is resolved, the market will continue to be drawn by headlines."

I find this interesting because the stock market has mostly ignored the trade rhetoric. It has done much better than this spring even though the fears expressed in the spring are mostly coming true.

As Krosby stated, the market could react to headlines on the negotiations with China. Now it seems the two nations aren’t close to getting anything done.

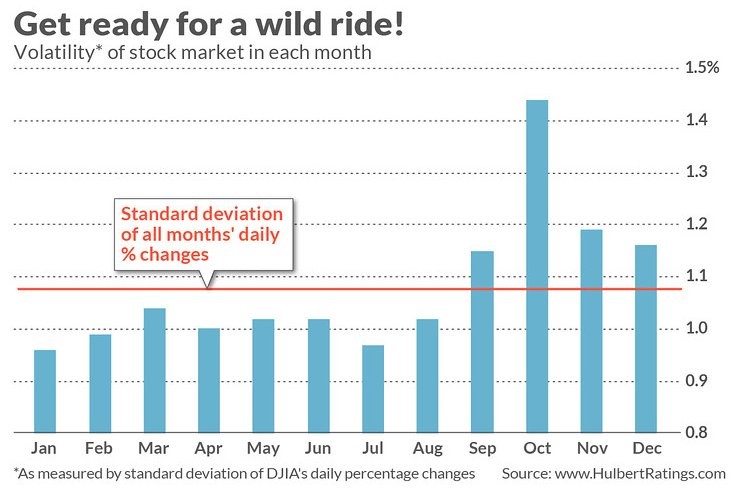

The stock market isn’t pricing in a long negotiation process which will have negative economic effects along the way. It’s intriguing that the market is entering the most volatile month of the year, just as the trade battle is heating up.

As you can see in the chart below, the standard deviation of daily changes is the highest by far in October. It is almost 50% higher than the year average.

Banks Underperform - Hard Data Shows Warning Sign

The optimistic GDP growth estimates are heavily influenced by survey data. It is the only information we have about the economy in September.

I’m not saying the estimates are all wrong. It’s more likely that they are too optimistic than too pessimistic. There has been a divergence between the economic surprise index which measures the survey data and the economic surprise index which excludes surveys. T

his was seen in manufacturing where the August manufacturing ISM PMI was very optimistic. However, the industrial production report only showed moderate growth.

A similar divergence occurred about 12 months ago, but there were no corrections in 2017. The correction occurred in January after the hard data surprise index rebounded.

This is why I don’t think this is an automatic sell signal. Rather, it proves some of the survey data is overly optimistic. This summarizes why investors shouldn’t be euphoric. I think the gains for 2018 are capped near where the market is now.

Since 2019 will have mid single digit earnings growth, I don’t expect it to be a great year for stocks.