Apple - Stocks Fall Slightly As Most Important Week Continues

S&P 500 fell 0.15% and the Russell 2000 fell 0.14%. The first 2 days of the most important week of the year have been duds.

That’s no surprise. Earnings guidance has been weak, and stocks were very overbought starting the week. The Nasdaq fell 0.81% as it was dragged down by Nvidia which fell 4.64%.

That’s much better than how it looked after hours on Monday. It managed to stay above its 52 week low it set on Christmas Eve.

A 1.38% increase in the VIX didn’t move the CNN fear and greed index as it stayed at 55 which is neutral. I still think the market is overbought.

Stocks have fallen on the past 7 of Powell’s Fed statement days, so we might have a 3 day losing streak. A little more weakness would take us away from overbought territory. But I wouldn’t be bullish with the intermediate term time horizon. Earnings estimates have been cratering.

On Tuesday, the worst two sectors were communication services and tech. Verizon pulled down the communication services sector as it fell 3.29%.

It is very close to its Christmas Eve low. Its earnings were hurt by the restructuring of Oath. The acquisitions of AOL and Yahoo weren’t the best ideas. The best two sectors were industrials and materials. Caterpillar stock rallied 1.77% after cratering on weak earnings on Monday.

Apple Beats Lowered Estimates. Yay?!?

Apple beat EPS and revenue estimates. But this beat is weak because it lowered guidance earlier in the year.

Even though Apple’s beat was manufactured, the stock still rallied 5.7% after hours. I don’t care if Apple came into the report oversold. I still wouldn’t buy it.

Specifically, Apple had EPS of $4.18 which beat estimates by one penny. Revenues were $84.3 billion which beat estimates for $83.97 million. Services revenues were $10.9 billion which beat estimates by $30 million.

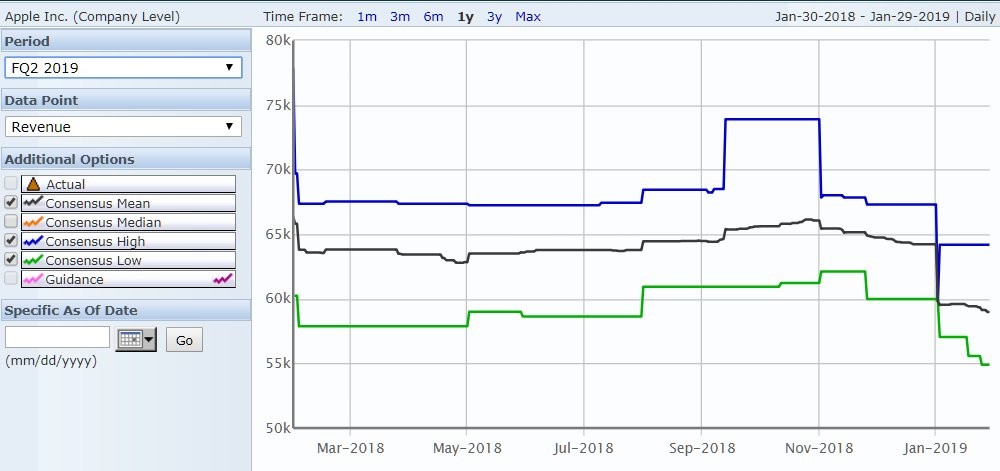

Apple expects Q2 revenues to be between $55 billion and $59 billion. That midpoint is below analysts’ estimates for $58.83 billion.

As you can see from the chart below, analysts lowered their revenue estimates for Q2 after Apple guided lower earlier in the year. The new guidance couldn’t even beat lowered estimates. It wouldn’t be a surprise if Apple beats its latest guidance. But it still likely won’t beat the November consensus for above $65 billion in revenues.

Apple - iPhones Still Matter: Ignore Misdirection

As Apple announced in November, this is the first quarter with its new reporting metrics. Apple is now giving out gross margin numbers for its services and products segments and withholding sales for its most popular products such as iPhones.

Apple wants you to watch its strong services segment and ignore the lack of growth from iPhones. Unfortunately, investors aren’t buying into this concept as they have sold the stock heavily since November. Apple withholding information on iPhone sales is a signal the device won’t be a long term growth driver.

This means Apple won’t be a growth company either.

Apple - Specifics Of The Quarter

I wasn’t being overly harsh in saying Apple isn’t a growth company. The firm’s total sales were down 5% which was the first decline during a holiday season quarter since 2001.

Imagine how bad the results would have been if the consumer had a weak holiday shopping season. Apple is guiding for about -3% revenue growth next quarter. If it beats guidance, growth will be about flat.

A next potential growth driver is the new iPhone releases this fall. The problem is smartphone sales have peaked and Apple won’t be able to raise prices in back to back years.

Apple’s best bet is to add additional features to its high end devices to get people to buy more expensive devices.

Revenue from Mac was up 9%, wearables, home, and accessories revenue was up 33%, and iPhone revenue fell 15%. To be clear, iPhone is still by fall the biggest part of the company. It had $51.98 billion in sales. iPad, Mac, and Wearables, Home, and Accessories had $21.46 billion in revenues.

Revenues from China were down 27%. Apple was hurt much more by China than Caterpillar and Starbucks were. China is definitely weak, but it appears Apple lost share as well. A report by Canalys stated smartphone sales on China fell 15% in Q4.

Apple - Services Had Weak Revenue Growth

Services revenue growth was 19% which is near the low end of where it has grown recently.

It’s disheartening to see the division Apple wants to highlight have relatively slow revenue growth. Apple obviously needs to increase the revenues it garners from each user since total device growth will be low. Services had 62.8% gross profit margins.

A year ago those margins were 58.3%. There are 900 million iPhones in use and 1.4 billion total Apple devices worldwide. Apple plans to squeeze every penny it can out of users by selling them services like Music and iCloud storage.

Apple plans to surpass 500 million paid subscriptions in 2020.

So much for the idea of Apple buying Netflix. The only reason journalists write articles about what firms Apple will buy with its now $130 billion cash hoard is to generate clicks. That might be true of all articles, but this type of article is based on pure speculation which is why these articles aren’t useful.

If Apple hasn’t bought Netflix yet, there is no way it will buy the company now. The one company I can guarantee you Apple will buy is itself as it will be using its cash to buy back shares.

Apple - Conclusion

Earnings are coming fast and furious. As of Tuesday, 135 firms have reported results. 72% have beaten EPS estimates and 60% have beaten sales estimates.

Apple is one of those firms that beat estimates, but the beat was tainted by the negative pre-announcement. It's no longer a growth firm which is why I recommend saying away from the stock this year.

Apple is smart to pivot towards services as it is a more sustainable business. However, its main growth engines that were iPhone unit sales and iPhone ASPs will be limited in the future.