Disappointing Thursday

At first glance, it looks like the stock market had a nice day after a solid jobs report. However, the stock market’s reaction was weak because the jobs report is old news. The economy has slowed since the survey week of the BLS report. While the stock market extended its winning streak to 4 days, it only rose 0.45% which is weak considering it was up more than that in the futures market before the report came out.

If you consider the hype lead into it, this reaction was negative. It should have been negative because jobless claims were weak. Updated data in the 2nd half of June has been worse than the first half of the month. Once the July monthly reports start coming out, we will see clear weakness.

It’s incredibly dumb to say the market has already priced this weakness in. The market is near its record high without any sign of this recent trend reversing. When the stock market ignores real risk, it’s called euphoria. You can argue, the non-momentum stocks aren’t ignoring risk. However, the internet names now dominate the index. Software ate the world this year.

Sentiment Readings

The stock market is on a 4 day winning streak, but the CNN fear and greed index is at 50 which is neutral. AAII survey showed investors are bearish again, but less so. Percentage of bears fell 3 points to 45.9%. And percentage of bulls also fell. It was down 2% to 22.2%. There are 15.8% fewer bulls than average and 15.4% more bears than average.

This survey is very confusing because investors are clearly optimistic. They wouldn’t be buying stocks if they were bearish. NAAIM exposure index fell from 76.57 to 71.47 which still signals fund managers are long, but they aren’t close to exhibiting euphoria.

It will be very exciting to see the Bank of America fund manager survey for July because it will likely show how overexposed managers are to tech. It’s not as if this survey will change my position, but it's good to see specific data. It’s very likely to support that perspective. Last month showed managers were overweight tech and since then tech stocks have increased.

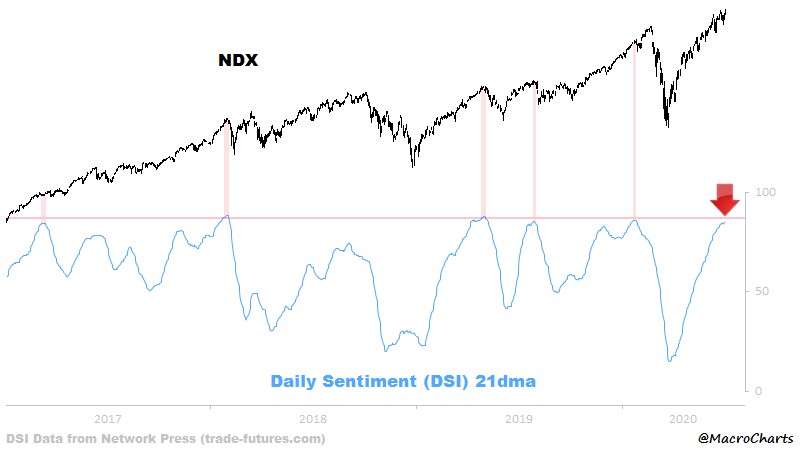

As you can see from the chart below, the 21 day moving average of the Nasdaq’s daily sentiment index is very high. It’s actually in the top 3% of overbought days in the past 20 years. That chart doesn’t include Thursday’s modest rally, so the sentiment index is probably slightly higher now.

Nasdaq Is Too High

It's unlikeliy that Nasdaq will fall 78% like it did after the 2000 dot com bust, but we do see at least a 15% decline coming this summer. It will feel the worst for the most heated momentum stocks like Shopify which was up another 1.3% on Thursday.

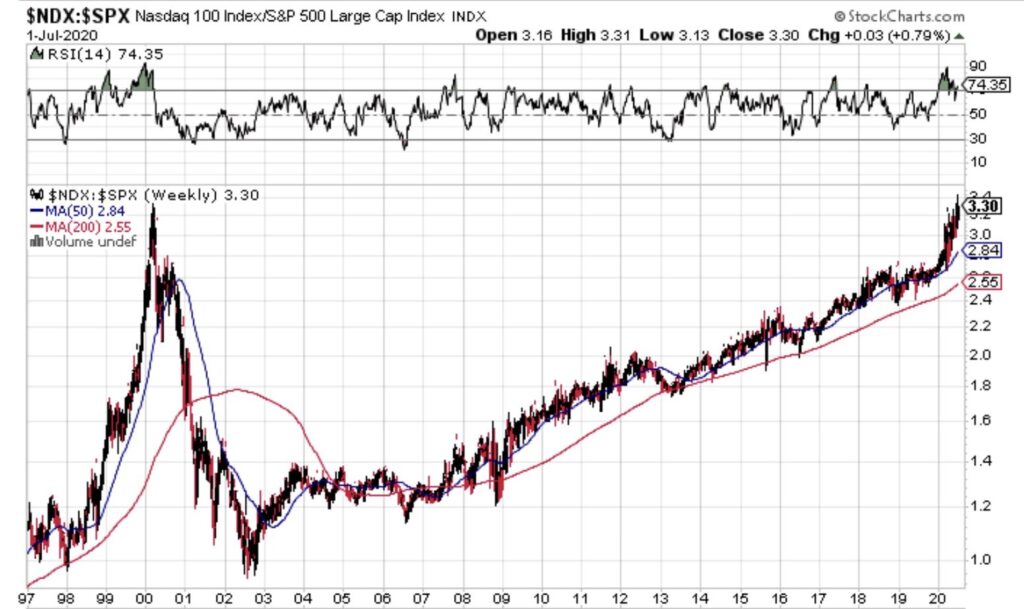

As you can see from the chart below, the Nasdaq 100 in relation to the S&P 500 has surpassed its peak in March 2000. A rally in this ratio started below 1 in 1998 and reached its peak 2 years later. That’s much different from the recent rally as it bottomed at 1998 levels in 2002 and took until 2020 to get to the peak in 2000.

This has been a long term trend. It only started going vertical this year. Fact that tech has done so well for almost 20 years has made some speculators think this isn’t a bubble. It’s not as big of a bubble, but the overvaluation is extreme in many of the cloud names.

14 day RSI of this ratio is 74.35 which is the same level it peaked at in 2000. Don’t think that just because ServiceNow stock has done well for 8 years that it can’t have a major correction. Its 22 price to sales multiple is near its record high.

Tesla Is About To Be In The S&P 500

If Tesla is profitable this quarter, it will be added to the S&P 500. It would be highly unusual to add a company with a market cap of over $200 billion. As you can see from the table below, it’s going to have a 1.36% weighting in the index. If the stock keeps ramping, it could be even bigger. That means there will be even more forced buying from index funds, which could increase the weighting even further. This is a snowball effect. It’s creating a massive bubble.

Tesla’s stock was up 7.95% on Thursday because it reported better than expected deliveries in Q2. The firm delivered 90,650 cars in Q2 which beat estimates for 72,000. Deliveries fell 4.8% from last year which is pretty great considering the huge decline in auto sales due to the pandemic. Tesla gained market share in Q2. There were 80,050 deliveries of Model 3 and Y, showing the strong demand for Model Y. There were 10,600 deliveries for Model S and X.

Investors noticed extreme euphoria among Tesla watchers as the stock hit a record high. People are acting as if the company has now cemented its success even though VW sells 30 times the cars Tesla does. The stock doing well doesn’t mean the company has reached success. The company is at least a few years away from gaining significant market share in the auto industry.

Apparently, the stock price is simply ahead of the business. It’s notable that the euphoric observers weren’t necessarily Tesla shareholders. They just enjoy poking fun at the short sellers. Tesla has easily been the worst trade shorts have made in the past 20 years.

Tesla shorts have lost far more money that the company has made in its history. Elon Musk taunted the SEC in a tweet on Thursday. This type of reaction makes many avoid the stock. Apparently, not enough people are avoiding it because it is up 181% year to date. It’s a big bubble even if you believe in the company’s future.