Bottom In Same Store Sales Growth?

Last week’s Redbook same store sales growth report could be an indicator of the bottom in growth or that the bottom might be reached in a couple weeks. Many are now predicting this week’s report to be the bottom in same store sales growth. We are slowly starting to see better economic numbers as the individual states that are reopening are partially resuming economic activity.

Specifically, the Redbook report from the week of May 2nd showed same store sales growth fell from -8.1% to -9.3%. We’ve heard from many firms that economic activity bottomed in April with a modest uptick in activity since then. We already know the April retail sales report is going to be a bloodbath. It’s disheartening that the numbers to start May were bad. Obviously, that week included some of the end of April.

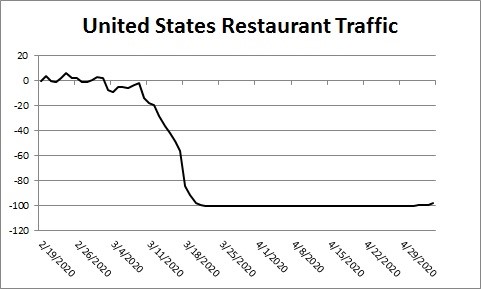

As you can see from the chart below, U.S. restaurant traffic is slowly starting to come back. Unfortunately, many restaurants are going to permanently closed. Restaurants that come back will be able to gain market share. Specifically, from May 1st to the 3rd, restaurant sales growth was -99% and on May 4th it was -98%. At least we can now look at the OpenTable data for improvements opposed to seeing it at -100% for weeks on end.

Another Weak PMI Disguised By Supplier Deliveries

April services ISM PMI was weak, but it would have been much worse if it wasn’t for the huge spike in the supplier deliveries index. As you can see from the chart below, the NSA supplier deliveries index hit a record high going back to the mid-1990s. When the index moves higher, it means deliveries were slower. In theory, when deliveries are slower, it means demand is so high suppliers can’t keep up.

However, in this case the supply chain is busted. The index spiked from 62.1 to 78.3. I’m guessing this will be the highest reading for decades because China has been rebounding and the economy is reopening. There would need to be another pandemic or a world war for this reading to be hit again. In fact, it’s possible that the economy improves in May, but the PMI falls because this category drops sharply.

Overall services PMI fell from 52.5 to 41.8 which beat estimates for 37.9. Economists still haven’t learned their lesson that the deliveries index positively manipulates the headline reading. This PMI is consistent with GDP growth of -2.3% which is laughably high. GDP growth is going to be way below -10%.

Once again, the Markit PMI has it right as the index fell from 39.6 to just 26.7; it was slightly below the flash reading of 27. This supports the point that the majority of the drop occurred by mid April. It’s interesting that the worst weakness in the economy occurred during the strongest part of the stock market rally.

Within the Markit report, the Chief Business Economist stated, “The slump in the business survey indicators to all-time lows in April indicates how the 4.8% rate of economic decline seen in the first quarter will likely be dwarfed by what’s to come in the second quarter.”

This was the worst Markit PMI ever, but the report started after the last recession, so that’s not impressive. It would likely be worse than the trough of the last recession, but we don’t know for sure.

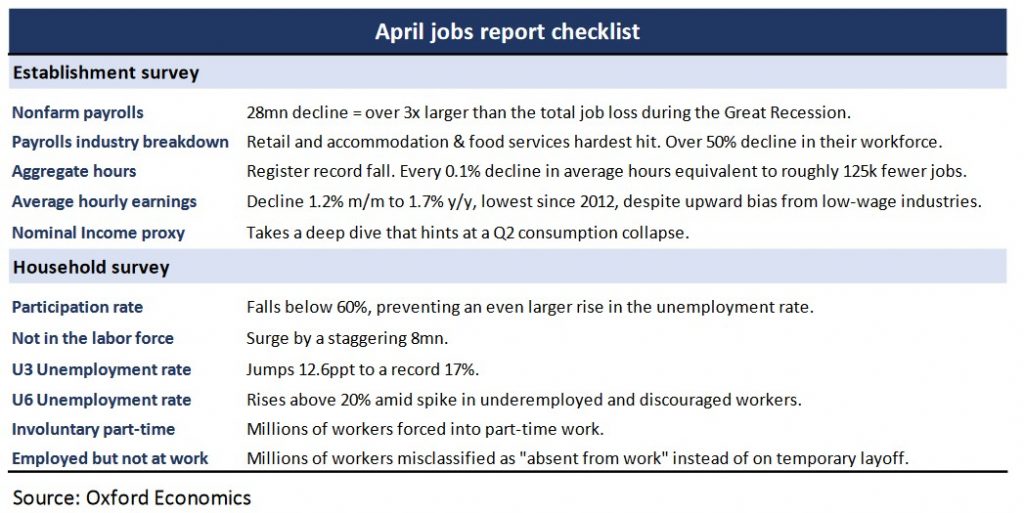

Getting back to the ISM report, the business activity index fell 22 points to 26 and the new orders index fell 20 points to 32.9. The employment index fell 17 points to 30. Unemployment report on Friday is expected to show the unemployment rate increase to 16.3% from 4.4%. It’s going to be the worst report on a rate of change basis ever by far. The table below previews the report.

As you can see, Oxford Economics predicts the unemployment rate will rise to 17% and the underemployment rate will rise above 20%. It expects retail and accommodation to have over a 50% decline in its workforce.

Prices index was up 5.1 points to 55.1 signaling higher inflation potentially because of shortages. Many firms are raising wages which isn’t typically what you see in recessions. Companies need to pay workers for working in these terrible conditions and they need to out-pay unemployment insurance. Only the finance and insurance industry reported an increase in business activity.

In the comments section of this report, there were 6 mentions of COVID-19 out of 10 statements. A management of companies and support services firm, “The oil exploration sector is very weak, with the record low price of oil and the country’s shutdown due to the COVID-19 threat. We are hopeful for a bump in activity once the country starts to reopen.”

Energy companies are in such a bad situation all they can do is hope. Their wishes have recently been granted as oil prices have risen 5 days in a row.

A healthcare and social assistance firm stated, “COVID-19 has halted much of our standard work to procure items for our organization. It’s halted much of the world, except for health care. Distributors were woefully unprepared for the spread of this pandemic, and many health-care systems/providers depend on them for inventory planning and availability.”

Hospitals are in dire financial straits. This comment went on for another few sentences saying how bad the situation is, the longest comment seen in an ISM report.

Conclusion

Redbook same store sales growth was terrible in the end of April and the beginning of May. Some restaurants are starting to reopen. The ISM services report was terrible. PMI was lifted because of the supplier deliveries index.

May labor report on Friday will show the unemployment rate is in the mid to high teens. ISM report included a long winded quote about how bad the healthcare industry is doing. Hospitals are in dire financial straits which can put them in a bad situation for years.