Earnings Estimates Improve The Most In At Least 21 Years

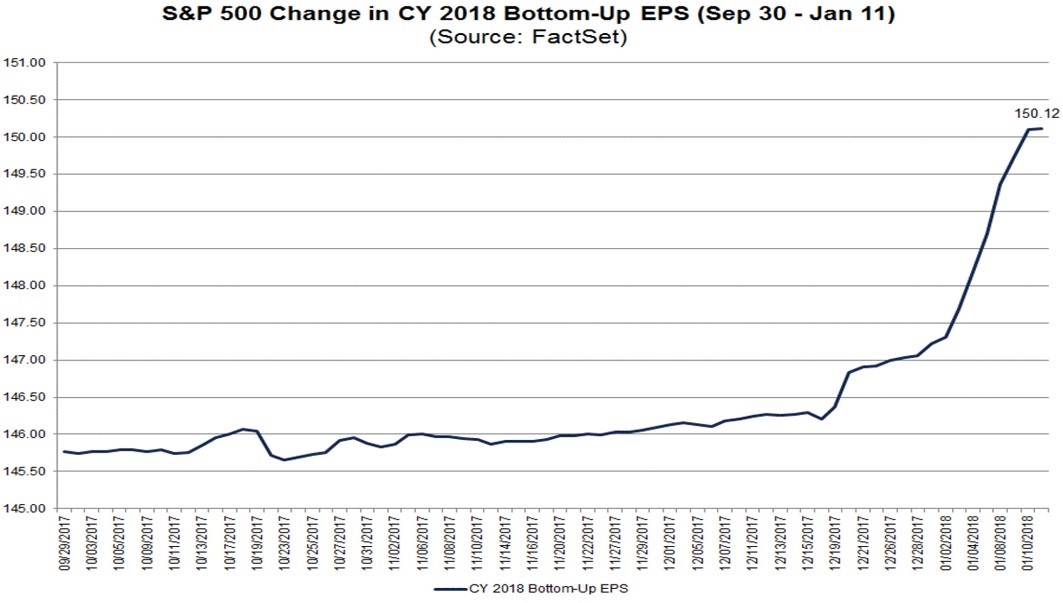

If you’re bullish on stocks because earnings are strong, you are sitting in the catbird’s seat because the estimates have been expanding at an unusual pace. As you can see from the chart below, the 2018 full year estimate has increased since December when the tax cut was passed. Obviously, my discussion about 2018 earnings being trouble in an article a few months ago was completely wrong. Firstly, the dollar has fallen, and oil prices have risen. Secondly, the tax cut has boosted numbers. Unless there’s an unknown negative geopolitical catalyst, I can’t see 2018 earnings being bad. The ultimate decision investors need to make now is if the current estimate for $150.12 in S&P 500 EPS for 2018 fully captures the effect of the tax cut. Generally, earnings estimates fall from here until 13 months from now when all the results are in. However, the final estimates on the effects of the tax cut may not be in. Secondly, positive guidance this earnings season can boost 2018 estimates.

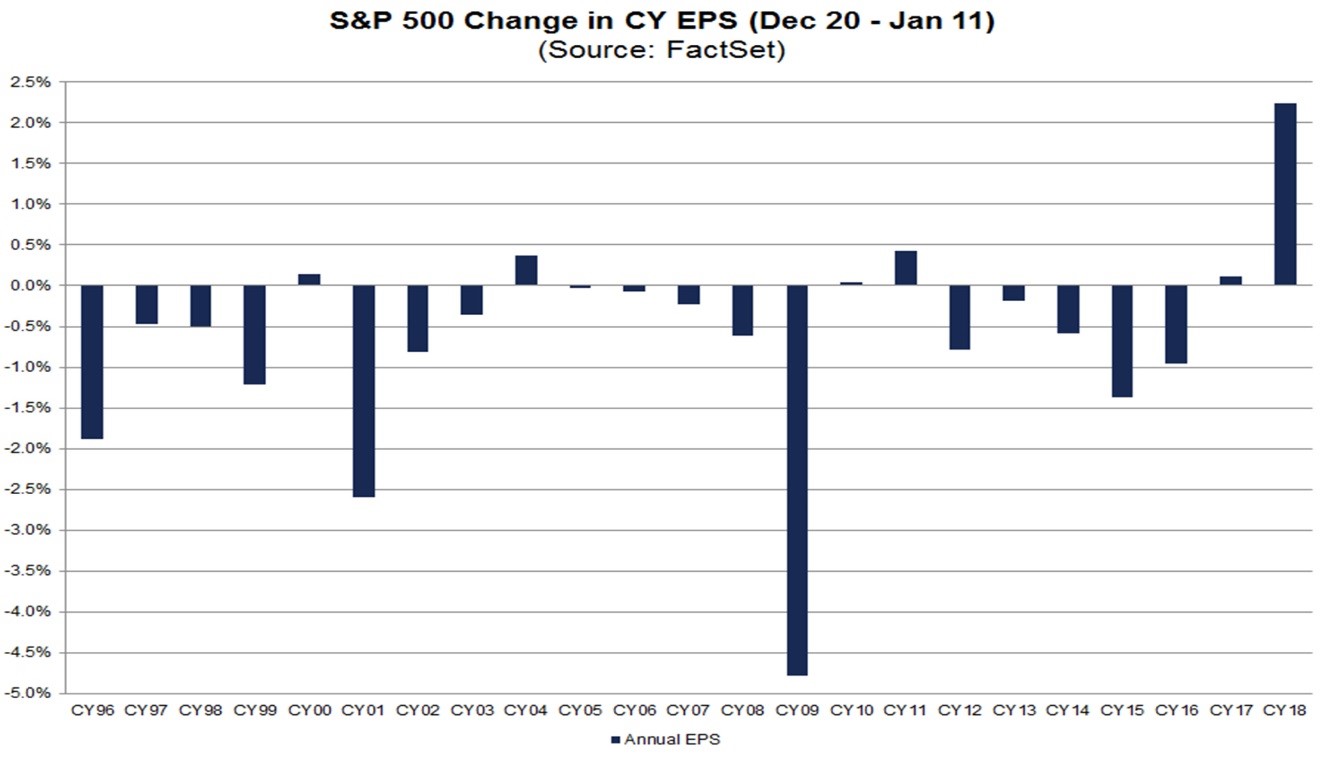

As I mentioned, the earnings estimates usually fall in this period leading up to the beginning of the year. The chart below shows the historical change in earnings estimates from December 20th to January 11th. It captures the period when they increased because of the tax cut passing. As you can see, they fell 17 years and rose 4 years. The highest increase was less than 0.5%, while this year estimates are up 2.2% from $146.83 to $150.12. It’s difficult to determine exactly which analysts, who updated their numbers recently, included the impact of the tax cut. The best way to determine if $150.12 is a good estimate is to come up with your own. One key indicator, which might signal earnings estimates are about to move higher in the next month, is that only 40% of analysts have confirmed or revised their 2018 earnings estimates for the firms in the Dow since December 20th.

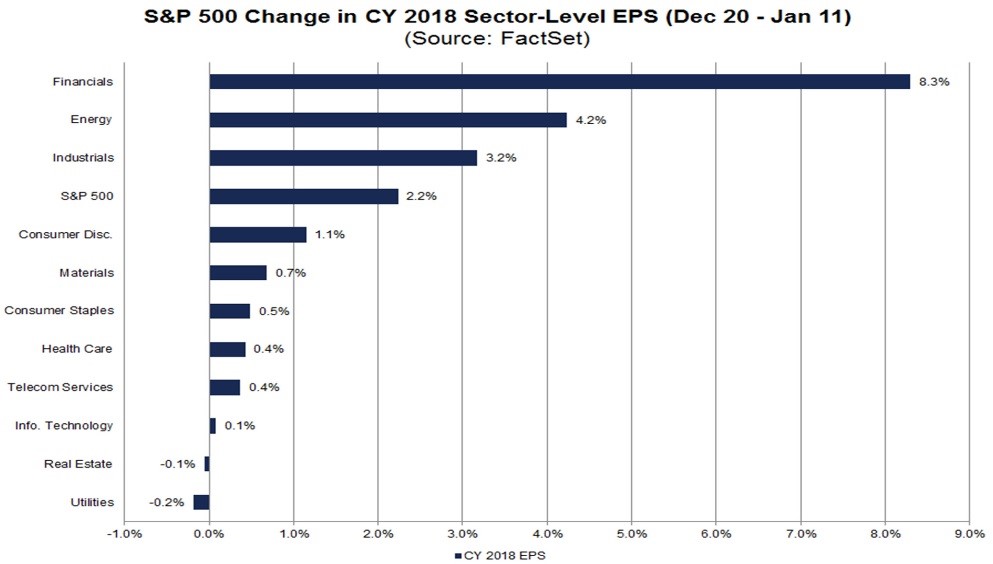

70% of analysts have updated their earnings estimates for American Express, JP Morgan Chase, Goldman Sachs, and Travelers. Those companies are in the Dow and S&P 500. It makes sense the financials’ earnings are being updated the quickest because the sector reports earnings at the beginning of earnings season. This explains the chart below which shows the sector breakdown of earnings estimate changes from December 20th to January 11th. As you can see, financials earnings estimates are up 8.3%. Based on this information, it’s safe to assume the other sectors will play catch-up, moving the S&P 500 earnings estimate towards the mid $150s. One aspect to keep in mind is that not all sectors are helped equally. Energy will be helped significantly, while tech isn’t expected to be helped. Anyone complaining about the tech stocks getting a large percentage of capital in 2017, will be pleased to see a more broad based rally in 2018.

Summary Of The Latest Results And Expectations

One other point, which I mentioned previously, is that investors will price in the results before the analysts get around to updating their numbers. Since the analysts haven’t finished updating their numbers, stocks may still have some room to rally on the tax cut. Although some complain that stocks have been going up based on the tax cut for weeks, the increases each day have been small which means they may not add up to fully pricing in the boost.

Let’s now review the latest updates on earnings. Besides 2018 earnings estimates increasing, 2019 estimates also went up. The latest average estimate is $165.50. That means with the S&P 500 at 2777.7, the S&P 500’s forward multiple is 16.78. At face value, that’s a very reasonable price, but I think you need to contextualize it if you want to estimate forward returns. Earnings won’t grow at this speed forever, meaning stocks should have a lower multiple during the time the tax cuts are being implemented. Secondly, the economy could falter, pushing down these estimates. Thirdly, in the next 10 years, I wouldn’t be so sure that the tax rate will stay this low. The Dems could easily win Congress and reverse future tax policy, raising corporate tax rates.

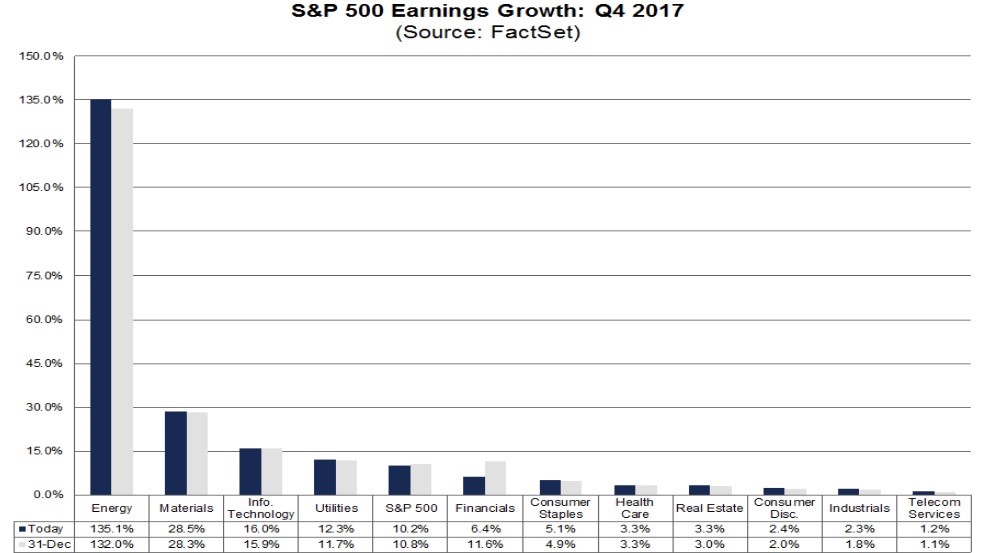

Not many firms have reported earnings. As of last week, 5% of S&P 500 firms have reported results. 69% of firms have beat earnings estimates and 19% have missed estimates. The average beat rate is -3.2% which shows why the blended estimate for Q4 earnings growth has fallen from 10.8% to 10.2% as you can see in the chart below. The biggest decline has come from financials with JP Morgan being the main reason estimate growth has fallen from 11.6% to 6.4%. On the bright side, the companies beating earnings have seen their stocks increase 1.4% 2 days after earnings. In some of the after earnings periods in 2017, good results have been punished.

JP Morgan & Wells Fargo Earnings

The reason why JP Morgan’s earnings results tanked the financial sector’s blended estimate is because FactSet used the actual results which included a $2.4 billion one time charge in the 4th quarter which was caused by the Tax Cut and Jobs Act. Adjusted EPS was $1.76 which beat estimates by 7 cents. Revenues were $25.45 billion which beat estimates by $300 million. Essentially, JP Morgan saw the pain of the tax cut in Q4 and will see the gains in 2018 and beyond. The banks’ workers will be getting some sort of pay increase which will be announced in the next few weeks. JP Morgan stock was up 1.65% on Friday after the report.

Wells Fargo was an unusual case as its Q4 earnings were helped by the tax cut. Adjusted earnings were $1.16 which beat estimates by 9 cents. Revenues were $22.05 billion which was $330 million below estimates. The tax bill allowed Wells Fargo to get a $3.35 billion after tax benefit. 3.89 billion of that gain was because of the reduction to net deferred income tax. Wells Fargo stock was down 0.73% on Friday.