Comical Economic Data

Eeconomic data is comical at this point. We keep getting good results in the midst of an abject panic from stock market investors. Clearly, the economy was in great shape in January. And it was even better that many thought it would be in February.

We are still waiting for the shoe to drop in March which faced the depths of the stock market decline and the cancelation of most group events. By the time the full panoply of data is out, most of the decline will be over. It will be up to the historians to determine if the economy fell into a recession.

Redbook yearly same store sales reading showed 6% growth in the week of March 7th which was up from 5.9% in the prior week. This supports my prediction that jobless claims won’t spike on Thursday. Energy sector doesn’t employ that many workers. Even if some of the smaller firms go bust and the larger firms lay off workers, it won’t be a big hit to the labor market.

Biggest worry should be restaurants. Billionaire Tilman Fertitta, the CEO of Laundry’s which owns and operates more than 600 restaurants worldwide, stated he’s losing $1 million per day on sales of $12 million. That was from 5 days ago. It's likely that sales are even worse now and losses are mounting.

Redbook sales report was probably strong because people are spending a lot on necessities at supermarkets. From the peak, Costco stock is down 8.22% which is less than half the market’s decline. This firm will have amazing same store sales growth.

As you can see from the chart above, the Citi Economic Surprise index has been spiking lately as it is very close to the peak at the end of 2017. Many expect the economic surprise index to crater in March and April. Analysts underestimate the weakness from COVID-19.

Then, when analysts start to mark down their numbers far enough in the following few months, economic reports will be able to beat those estimates without being great. This bottom in stocks will occur around when the reports start coming in badly. Although some think the best time to buy is when analysts have lowered the bar too much.

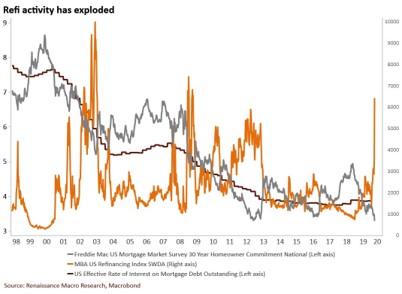

Refinance Activity Explodes

There is a lot of stimulus coming the economy’s way. You have a potential tax cut coming, lower gas prices, and lower rates which will let people refinance. Plus, there will be a natural stimulus which is people saving money in the near term by going out less. That extra cash that people are saving will get spent when COVID-19 blows over, assuming that they don’t lose their jobs. Refinancing activity has exploded in the past few weeks as rates are at record lows.

As you can see from the chart below, refinancing is up 480% from last year. An average borrower can save $275 per month on a 30 year fixed rate loan. To be clear, when rates rise, that low payment is locked in. If all borrowers saved $275 per month, which they obviously didn’t, it implies $3.5 billion per month in savings and $42 billion per year. That is 0.2% of U.S. GDP.

Personally, I think the housing market will have a rough spring even though rates have come down. It doesn’t make sense to go to an open house because you can catch COVID-19. So far, that prediction was wrong. Purchase applications were strong again in the week of March 6th. Weekly growth was 6%, on top of -3%. Yearly growth was 12%. We’ve seen the best yearly growth since 2016. Refinance index was up 79% weekly on top of 26% growth.

Low Oil Prices Aren’t Sustainable

Some people are saying the decline in oil prices will cause Occidental Petroleum to fail, giving us a ‘Lehman Moment’ for the oil patch. Occidental Petroleum stock is down 75% since January 15th. The firm recently cut its dividend for the first time in 30 years (86% cut).

And the company is vulnerable because of its $38 billion acquisition of Anadarko that was completed last year. That was disastrous timing as the company could have been worth at least 50% less had the deal happened a few quarters later.

This type of situation occurred in 2014 and 2015 when we were able to look back to deals from the prior few years and grimace. Since January 7th, EOG stock is down 56.5% which is shocking considering this is a low-cost producer which has low debt.

At the end of last year, it had a debt to equity ratio of 24%. Even at $40 oil the company can self-fund operations and internally generate cash flows. The stock obviously should be down because oil is in the $30s where it will face a cash flow deficit, but this price level is unsustainable. All the oil companies are pulling back capex and many will go bust.

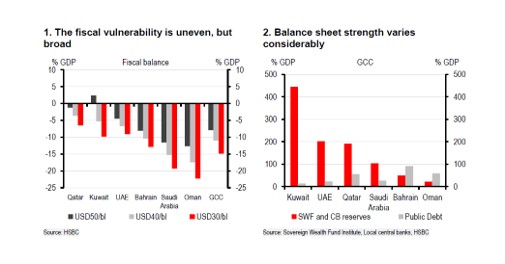

Middle Eastern oil has a much lower breakeven, but these countries need high oil prices to fund their budgets. Oil can literally go to any price in the near term, but in the long term, it will mostly stay above $40. As you can see from the charts below, Middle Eastern countries will have massive fiscal deficits at $30 oil.

Saudi Arabia’s fiscal deficit will be almost 20% of its entire economy. That will quickly be a disaster for the country. Plus, demand for oil will recover after COVID-19 passes.

Personally, I’m not an energy investor, but EOG Resources will be around for a long time as it can compete with Middle Eastern oil since they rely on oil to fund their expenditures. Even though EOG says it wants to keep paying the dividend, if oil prices stay in the $30s for a few months, it should consider cutting it.

Exxon Mobile should definitely cut its dividend. Its stock yields 8.29%. That high yield shows investors don’t believe it will be maintained. Why keep leveraging up to pay an outlandish dividend?