Update On ECB Bond Buying

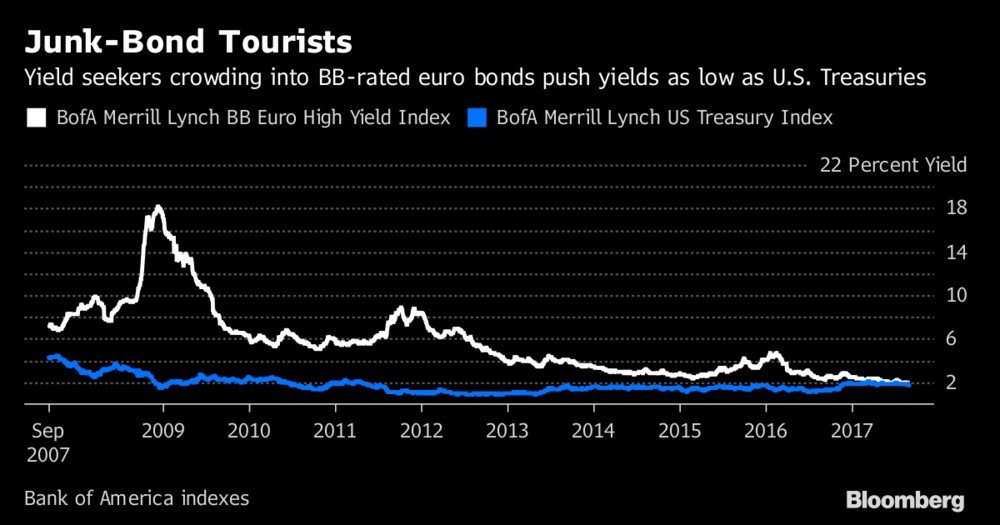

A new milestone is about to be reached in the ECB’s bond buying program. There have now been 998 bonds bought by the ECB. You can see the effects in the chart below. The BB rated euro high yield bond index is now at almost the same yield as the U.S. treasuries. That means there is no risk premium for junk debt. The unthinkable could happen in the next few weeks which would be junk bonds going below treasuries. Normally, investors would assign risk to lower grade bonds because they have default risk. We’re in a situation where defaults are low which shrinks the risk premium. The ECB’s buying puts it over the edge. This buying also keeps a lid on U.S. treasuries as investors are surprisingly seeking yield in what is considered to be the least risky bonds in the world.

The chart below gives a close in look at the effect the ECB bond buying has had on the spread between high yield and high grade debt. It’s not surprising that $10s of billions of bond buying has lowered junk yields. The spread has fallen by about 1.5% in the past 12 months. If this pace were to keep up in the next 12 months, there would be no spread at all.

Earnings Looking Vulnerable

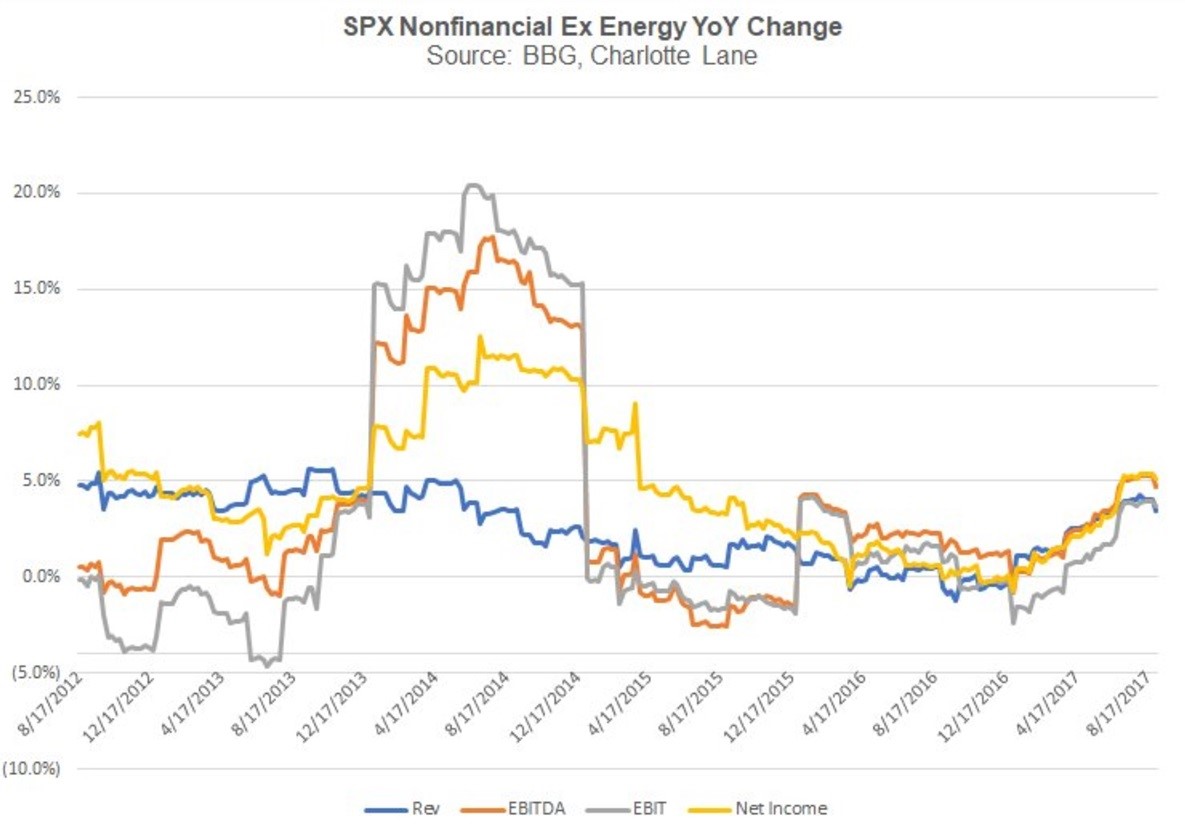

Now let’s look at the S&P 500 earnings to get a better picture on how stocks will do in 2018. The chart below shows the EBIT, revenues, net income, and EBITDA excluding energy and financials on a year over year basis. It makes the 2015-2016 earnings recession look less bad when you exclude energy since energy was responsible for the weakness because oil prices cratered. The latest decline might be muted in this chart because it excludes financials which will be seeing weakness and have been seeing some weakness already because of the flattening of the yield curve. Even though the big 5 technology firms don’t have an above average influence on the indices, they still have a huge impact on these earnings growth results. Technology is also one of the cheapest sectors compared to its historical levels. Excluding technology, the stock market is near the most overvalued level ever. Looking at technology alone, the sector is near the historical average value. Therefore, the big tech names may not have an unusual impact on the market, but they have an unusual impact on valuations.

Facebook And Apple Could Be Inflated

It’s weird to think that technology isn’t expensive because most of the top firms are in the tech sector. Currently, we are in a reversal of the 1990s. In the 1990s, it was only tech in a bubble and now it’s everything else in a bubble. The only way technology is overvalued is if the current earnings are unsustainable. While you can make that argument for individual names like Apple and Facebook have unsustainable earnings, there’s no reason to think the entire sector is about to crater. To be clear, Apple earnings could fall because consumer electronics has historically been a low margin business. The cheap Android phones are getting better than ever; this could take a slice out of Apple’s profits as some of these great phones are only $200. Facebook earnings could fall if ad buyers start to question what they are getting with Facebook. There have been a few stories where Facebook is claiming its reach is larger than the entire population of American teens and subsets of Australia. This comes on the heels of Facebook inflating its video views by counting views which auto-play in the news feed. The question investors need to decide is if these reasonable bears cases are enough to take down the sector. Personally, I don’t think two companies could do that.

Weekly GDP Estimate Recap

Let’s get an updated look at the GDP forecasts from the various district banks in the Federal Reserve system. The chart below shows the NY Fed’s update. The NY Fed has always been bearish on Q3 GDP and this refresh is no exception. As you can see, the projected GDP growth fell from 2.17% to 2.06%. There weren’t many economic reports which contributed to changes in the calculation this week. The ISM non-manufacturing report didn’t have an impact because the report met expectations. If every report meets expectations for the next 6 weeks and the NY Fed has the correct weightings on each metric that contributes to GDP growth, then the economy will grow at 2.06%. That’s almost a guarantee to not be the case as the economic indicators have yet to show the effects from hurricane Harvey and hurricane Irma. These hurricanes will hurt GDP growth in Q3 and potentially help it in Q4 as the rebuilding takes place. The current forecast for Q4 GDP growth is 2.62%.

GDP Now has been updated to show 3% growth. It increased from 2.9% growth because the forecast of the contribution of inventory investment to Q3 GDP increased from 0.87% to 0.94% because of the wholesale trade report. The wholesale trade report, which was released on Friday, showed a 0.6% month over month change in inventories which beat the consensus of 0.4% growth. This stockpiling of inventories implies businesses are optimistic about future demand. The blue chip estimate for GDP growth remained at 2.7%. The St. Louis Fed remains a very optimistic outlier as it forecasts GDP growth to be 3.69%.

Conclusion

It will be interesting to see how the hurricanes effect the iPhone sales. Although I might be overemphasizing the effect of the storms, my reasoning for concern is twofold. First, the cities of Houston, which has 2 million people, and Miami, which has 440,000 people, are at a standstill. These people are worried about necessities, not a new phone. Secondly, the new iPhone announcement won’t dominate the news cycle because of the coverage of hurricane Irma. Currently the noaa.gov website is the 158th most popular website in the country. The hurricane will dominate the news after it makes landfall on the 10th. If I was Apple, I would push the event back a week to September 19th and give a big donation to those in need. That would make the company look good and grant it the limelight it craves.