Great Q1 Earnings: Potential Headwinds

Q1 2018 earnings growth was 24.68%. As I have documented for the past few weeks, this quarter has been unlike the historical average as growth estimates improved dramatically and the heightened expectations were beat. EPS estimates were raised heading into this quarter for the first time in 7 years. Therefore, I didn’t know what to expect before earnings were released. The beats make me optimistic about growth for the rest of the year although the recently strong dollar could damper hope of a similar beat rate. Furthermore, energy sector earnings suddenly look precarious as oil prices have crashed in the past few days. As I’ll get to in another article, the Italian political uncertainty could weaken the European economy which is already seeing decelerating growth. These are all headwinds which can impact growth. There are always headwinds; it’s up to investors to determine if they are enough to push down stocks.

As for now, we get to admire the great Q1 results. They haven’t pushed the stock market to record highs yet, but that doesn’t mean they weren’t impressive. Instead of complaining about how stocks haven’t moved up, we can take it as a gift because they have moved towards historically average multiples. Although some have compared this market to the 1990s bubble, multiples aren’t close to where they were then. The cheaper the market starts a recession at, the less it will fall. Earnings weakness during recessions is temporary, so stocks become a buy even if they fall less than earnings.

Problems With Analysts’ Projections

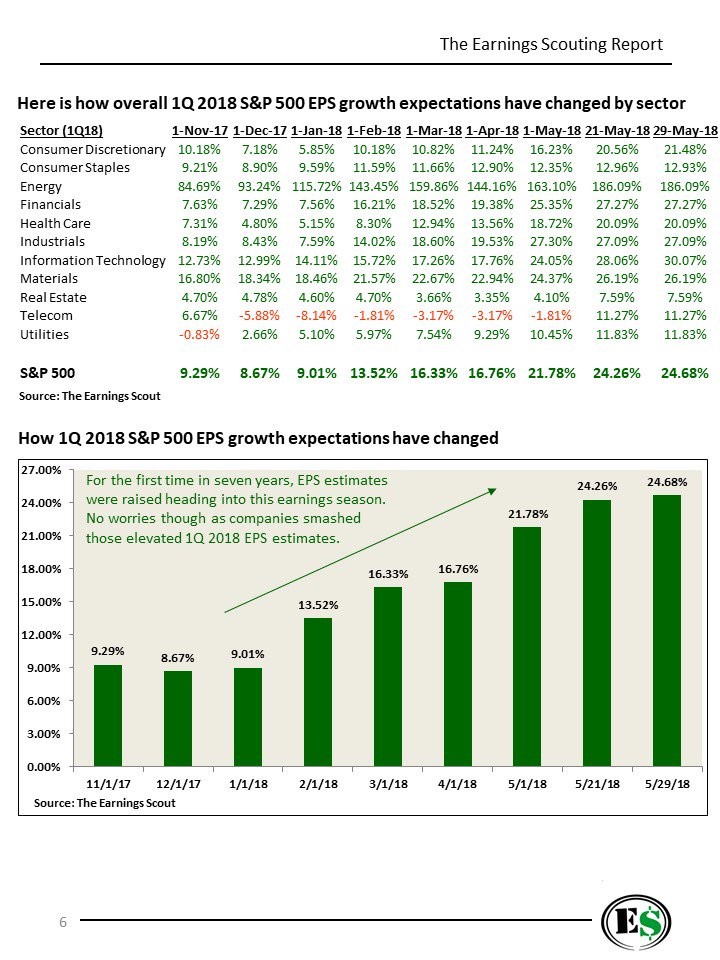

As you can see from the chart below, the expected Q1 earnings growth on November 1st, 2017 was 9.29%. I don’t think it’s fair to criticize analysts for being wrong with these estimates because they couldn’t have included the tax cuts in their numbers until the legislation was passed. The bulls will obviously be more likely to criticize analysts in this case because they were too pessimistic. Analysts are usually pessimistic following recessions; the tax cuts provided a new reason for an improvement to initial estimates.

I think it’s fairer to criticize analysts during the average quarter where they cut estimates right before earnings season. The biggest problem with analysts is they just focus on company guidance instead of coming up with their own research based on changes to the industry, changes in the economy, and changes in commodity prices. To be clear, analysts are capable of doing great research as seen in the sell side reports; it’s just that they are biased towards pushing up stocks. That can be shown by the fact that there are much more buy recommendations than sell recommendations, there are overly optimistic estimates for the long term future, and the fact that estimates are lowered right before the quarterly results allowing firms to easily beat estimates.

Sector By Sector Estimate Changes

It’s interesting to review the individual sector estimate changes. As you can see, energy went from 84.69% to 186.09% growth. There were expectations for a sharp deceleration in earnings growth as the comparisons got tougher. However, the comparisons don’t look as tough with oil in the low $70s. With oil falling recently, the estimates for future quarters might fall. Prior to the tax cuts being put in the estimates, it was said that tech would benefit the least from them. However, many tech firms like Apple have utilized the repatriation tax holiday. As you can see, the fear that tech wouldn’t see an earning boost from the tax plan was unwarranted. However, tech will be hurt the most by the rising dollar because the sector derives a majority of its revenues from international markets. The industrials sector probably improved the most because of cyclical growth as manufacturing has done well. I’m looking for an even better economic backdrop in Q2 as the regional Fed reports for May were strong and the April industrial production report was solid.

Future Earnings Expectations

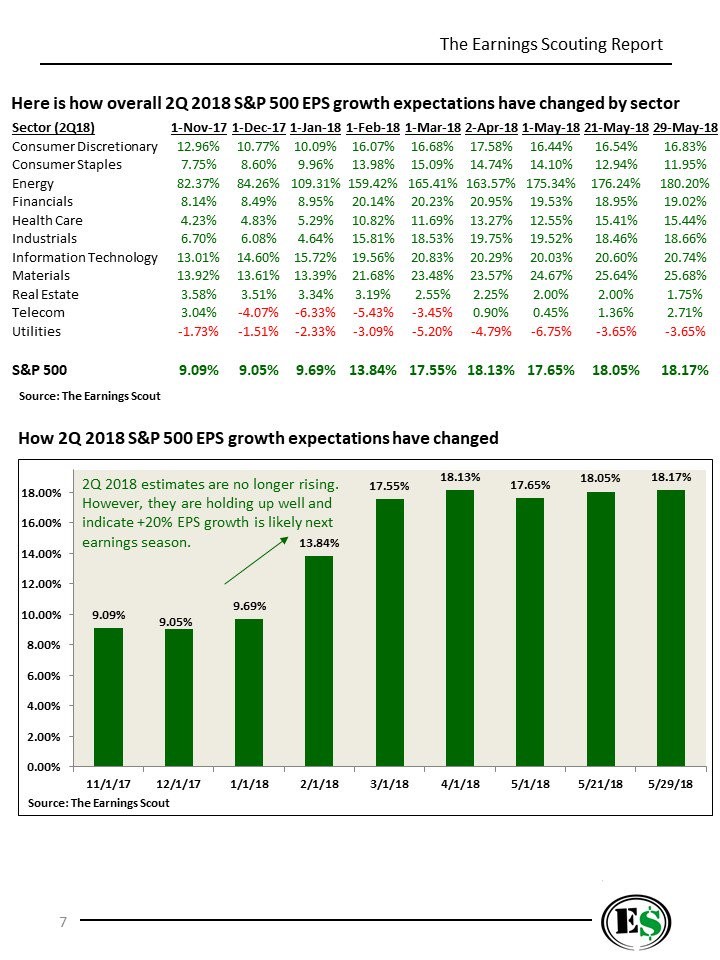

I discussed my thoughts on some of the sectors’ future earnings growth outlooks. The table below shows the current estimates as of May 29th. As you can see, there has been a similar improvement since the tax cuts. The latest growth rate is near where the first quarter reached before the results came out. The 18.17% expected growth rate explains why The Earnings Scout believes there is a 90% chance the earnings growth will be between 20% and 25%. The earnings estimates stopped rising after the Q1 earnings results started coming out. While that sounds bad, the main reason for the stabilization is the tax cuts became fully included in the analysts’ models. Even stabilization is good news when growth is expected to be in the high teens.

The recent rise in the dollar probably isn’t reflected in the tech sector earnings estimates since the 20.74% earnings growth estimate is the highest ever. The decline in oil definitely isn’t in the numbers as it started a few days ago. The estimates call for a 180.2% rise in energy sector earnings. This decline in oil will be great for most other sectors. Usually oil price declines are considered a negative signal for the economy, but if the decline is mostly supply based like in 2014, then there’s not much for investors focused on America to worry about. The reason I say the decline is mostly supply based and not completely supply based is because the global economy weakened in 2015 and 2016. Furthermore, America looks like the only market with solid prospects to accelerate GDP growth in 2018. For the first time in a long time, firms with high international exposure might not have dramatically higher revenue growth than the domestically oriented ones.

Conclusion

We could be headed for a repeat of the 2011-2012 period when there was political strife in Europe. This time the strife in Europe is worse, but American growth looks very strong. The stocks with international exposure could underperform the domestically exposed ones. That being said, even with international weakness, S&P 500 earnings growth should be above 20%. Therefore, if you’re looking at whether to buy the index on dips which occur because of international politics and international economic weakness, I think it makes sense to buy. America could receive huge capital inflows because it is the only game in town.