Since the “COVID Crash” of 2020 the market has generally been vertical with minimal volatility. Ironically, the VIX has remained relatively high, and the high skew reflects the guarded nature of institutional investors. This has made it difficult to apply hedges without increased of out-of-pocket cost, which will be a drag on performance. Here is an introduction to Don Kaufman’s Inflection Point Spread (IPS). This trade represents a zero cost way to turn the negatives of high skew into a positive.

For more on the history of skew and vertical pricing check out this post, Skew and Verticals: You’re Either with Me or Against Me.

What is Skew?

Implied volatility skew is when the call implied volatility falls as you move out-of-the-money and the put implied volatility rises. This reflects that potential downside crash risk of major market indices. It’s caused by institutional traders buying puts for protection and selling calls to help pay for it.

The issue of high skew is that the OTM puts are really expensive. Buying a put can be an important part of a hedging strategy. However, they would generally be ITM and be used during a sell-off. The hard part is balancing the need for a hedge during an unexpected sell-off while not significantly reducing your return. This is where the Inflection Point Spread shines.

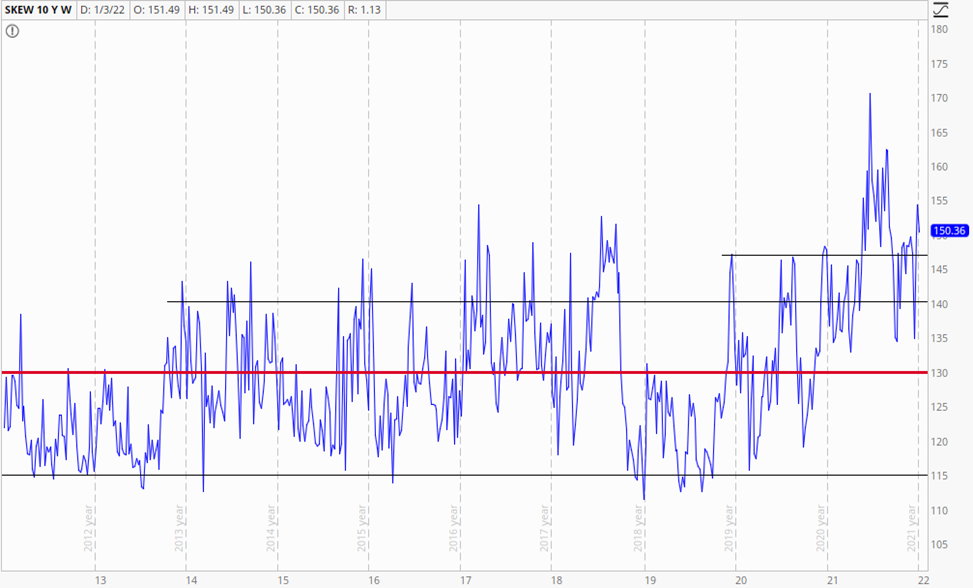

Just to show you how historically high the skew is for the S&P 500, let’s take a look at a chart of the CBOE Skew Index (SKEW).

A SKEW value above 100 represents the higher probability of a large decline in the S&P 500 that is priced into the puts. This chart goes back about 10yrs, but the CBOE shows data going back much longer. Historically, the highs were near 130 and occasionally reached around 146. You’ll notice that SKEW has been above historic levels since the Federal Reserve began tightening in 2014 and spiked much higher in middle of 2021. The current value of 150 reflects a degree of hedging that we have just never seen. Coupled with VIX levels around 16 and it creates havoc for many hedging strategies.

Inflection Point Spread Solution to Skew

When constructing a trade, the general idea is to buy the lower implied volatility option and sell the higher implied volatility option. When building a hedge, the idea is to remain premium neutral to minimize the cost of a hedge that is deployed to protect against a potential sell-off. The Inflection Point Spread checks both boxes.

The IPS is made of up of two different pieces. The first is a long put vertical and the second piece involves selling a put.

Long put verticals help reduce the cost of the hedge through buying a higher strike price and selling a lower strike for the same expiration. That means that you’re buying the lower implied volatility option and selling the higher volatility option. As a result, the cost is greatly reduced but is still significant.

The short put is added at a much lower strike price and is used to offset the cost of the long put vertical. That means the trade is put on for around zero cost.

Inflection Point Spread Example

Here is an example of the trade that Don introduced yesterday:

Trade 1: Buy Spread 16.75 Debit

- /MES BUY 1 18 FEB 22 4660 PUT

- /MES SELL -1 18 FEB 22 4560 PUT

Trade 2: Sell Put 17.50 Credit

- /MES SELL -1 31 MAR 22 3750 PUT

When placing a trade like this, you’ll likely need to break it up into two components. You’ll want to fill on the long put vertical first and then sell the put second.

One thing to point out is that selling a put is a bullish trade but notice the strike that is selected. This is a way OTM put that has about a 4% probability of expiring in-the-money. That means you enter the trade with no out-of-pocket cost, and you have the chance to make money on the vertical and the short put at the same time.

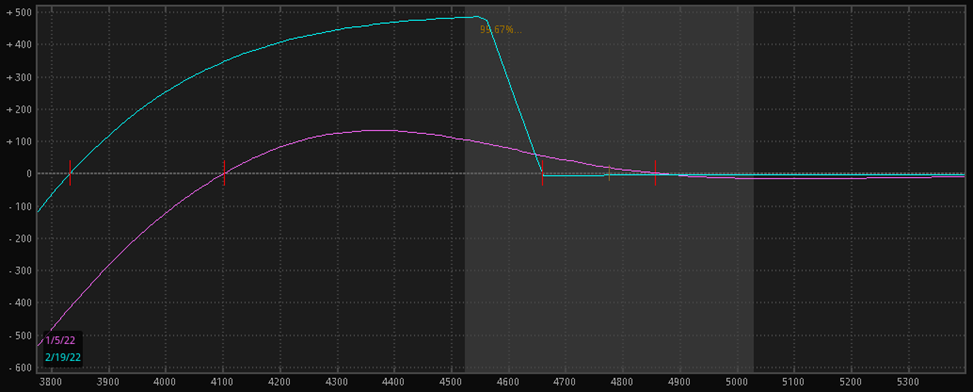

Inflection Point Spread Risk Profile

Here is a risk profile chart of the IPS spread. The purple line represents the P/L today and the blue line represents the P/L at the February expiration.

Since the trade involves a vertical, there is a maximum potential payout of around $500 if the price is below $4560. The initial margin is relatively small at a little over $200. That being said, you’ll need to have some space for the margin expand if the price falls and the margin on the short put expands. As a result, you may want to have about three times the initial margin in cash.

Conclusion

The Inflection Point Spread (IPS) is great way to begin building an inventory and checks the boxes for a preemptive trade or hedge against a market decline. The zero cost nature allows you to wait it out if the market advances as there isn’t any upside risk. However, it's locked and loaded if the market declines. Don Kaufman, TheoTrade co-founder, is preparing a three-hour class for next month to expand on this trade and we invite you to join him!

See how unlocking the Vomma Zone can help you better understand when volatility is about to rise.

Want learn more about how to work with me? Check out Trader by Your Side!

Not a subscriber? Become a TheoTrade member

5 Comments

Jimmy Mac

January 5, 2022Thanks for the written summary of this new and timely hedging strategy.

Brandon Chapman

January 5, 2022Thanks! It was great timing that Don discussed it yesterday heading into the Fed minutes today.

Willyp

January 12, 2022Thanks Brandon, great written explanation of the strategy.

Stephen Hueners

January 14, 2022Very interested in learning more about this strategy. You've called out the 4% level for short put in trade 1 -- how about levels for trade 2?

thx!

John

January 15, 2022What is the exit strategy if the market does decline? Do you close it all at once, at the inflection point? Take profit on the spread and keep the short put? Is there a time deadline?