September PCE Inflation Low Again

Inflation isn’t a worry in yet another report. September PCE reading showed headline inflation rose from 1.3% to 1.4% which missed estimates for 1.5%. Core PCE inflation was up from 1.4% to 1.5% which missed estimates for 1.7%. While inflation wasn’t an issue in this report, the market is looking past this. The economy in September has the potential to be completely different from the economy in April 2021 because life could go back to normal.

Labor market could tighten back up and demand for commodities will increase. This is worth keeping in mind because you don’t want to let your guard down on inflation just because we had low inflation in September and it has been low since the recession started.

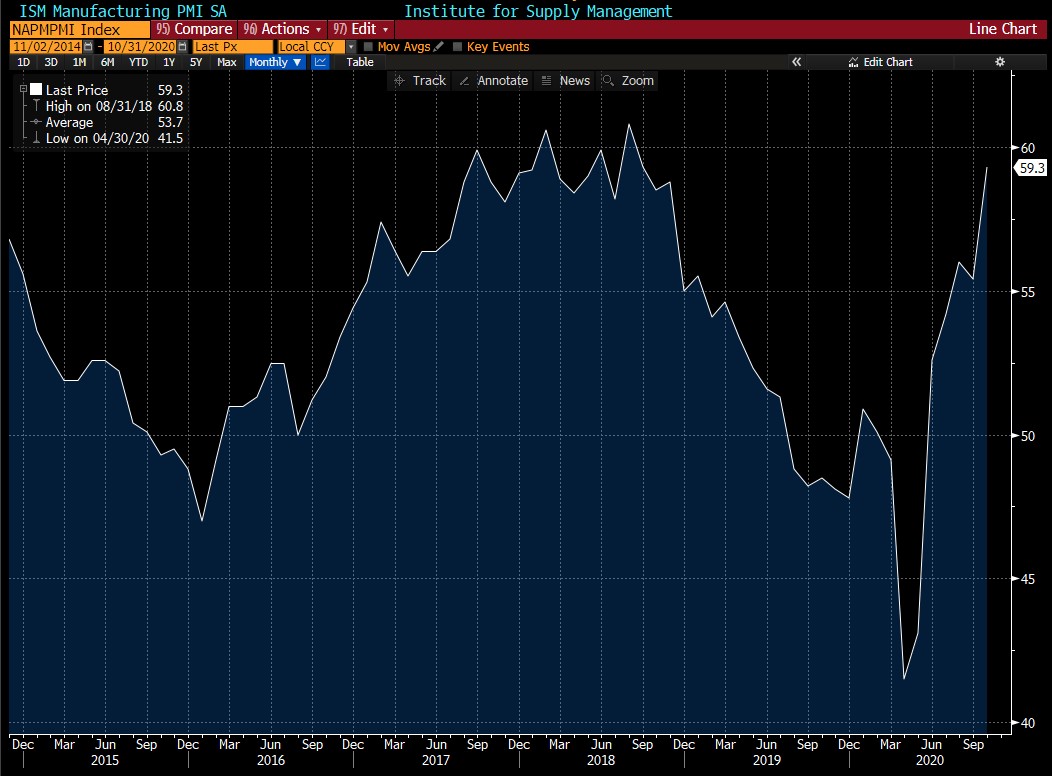

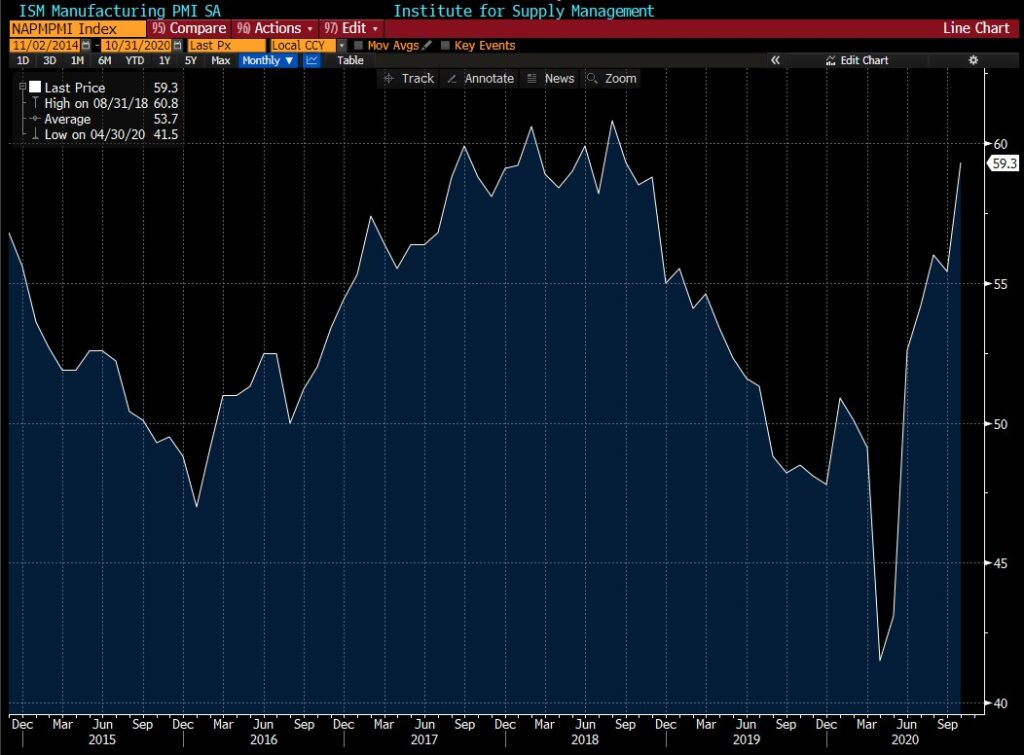

ISM Manufacturing PMI Destroys Estimates

In the past couple weeks, we have seen investors turn negative on the economy. October ISM PMI report was like a slap in the face to these scared investors. PMI rose from 55.4 to 59.3 which beat estimates for 55.7 and the highest estimate which was 57. As you can see from the chart below, it hit a 2 year high. New orders index exploded 7.7 points to 67.9.

Production was up 2 points to 63. Employment was up 3.6 points to 53.2. This report is consistent with 4.8% GDP growth. Obviously, that doesn’t mean exactly that amount of growth will occur. It just signals the industrial production report can rebound this month. Atlanta Fed GDP Nowcast expects 3.2% growth. On the other hand, because of the lockdowns, Goldman lowered its 2020 Q4 Euro area GDP growth forecast from -2.3% to -4.5%.

Prices paid index was up 2.7 points to 65.5. As you can see from the chart below, the prices index is hitting new highs while energy prices are still low. Either this means energy prices are set to recover or they have officially decoupled from the economy because of supply issues. This supply glut is temporary.

In the long term, investment cuts will eat into supply. ExxonMobil prides itself in investing when the cycle is troughing, but even it has pulled back. It has been selling assets to help pay for its dividend.

Within this report, 16 of 18 industries reported new order growth. The only industry in decline was textile mills. All commodities had higher prices except caustic soda. It's interesting that lumber is listed as a commodity that hid its price increase when it crashed recently. Lumber is down 20.3% in the past month.

Since the quantitative data was so strong, it’s no surprise the comments were positive. Firms see a cyclical recovery like me. A miscellaneous manufacturing firm stated, “Business levels have just about returned to pre-COVID-19 levels. Our company is remaining conservative with fixed-cost spending, knowing the uncertainties that lie ahead with COVID-19 and its potential impact globally.”

Obviously, the spike in COVID-19 cases and shutdowns in Europe will temporarily slow the recovery, but the manufacturing sector will be in better shape 6 months from now than it will be in late 2020. Maybe we see a little weakness in November and December, before global growth recovers.

This report was very positive. There were few, if any, negatives. However, we can see the shutdowns coming ourselves. That will have a moderate impact on the sector.

Less Impressive Markit PMI

Markit manufacturing PMI was better than expected, but wasn’t as impressive as the ISM reading. October final reading rose from 53.1 to 53.4 which beat estimates by a tick. Even still, this was the best PMI since January 2019. Prices index was the strongest since the start of 2019 similar to the ISM report.

Chief economist at Markit stated, “It’s inevitable that the pace of economic expansion will weaken after the surge seen in the third quarter, but the strength of the PMI hints at a recovery for which the underlying trend continues to strengthen at the start of the fourth quarter.”

Obviously, the quarter over quarter comp is tough for Q4 and last quarter had insane quarterly growth. However, investors already know this. A key is to sustain the recovery. Chief business economist mentioned the obvious which is that the recovery depends on whether the economy can stay open.

Manufacturing has beaten out services in this recovery because it is essential. Industrial production is being hurt by the energy industry which is in its worst downturn ever. That will reverse course next year when prices rise. Global manufacturing PMI also was strong as it increased from 52.4 to 53 which is a 29 month high.

Housing Is Getting Expensive

September construction spending report showed weaker growth than last month. Total spending was up 0.3% which missed estimates for 1% and last month’s 0.8%. August’s reading was revised down from 1.4% growth. Private residential construction was up 2.8% as you’d expect since the housing market had a great summer.

Private non-residential spending was down 1.5% and public spending was down 1.7% which makes sense because we are in a medical emergency; there isn’t extra money for infrastructure projects.

One negative on housing is prices are growing too fast. That will weaken demand even if rates don’t rise. If rates rise, the industry is in for a world of hurt. As you can see from the chart above, house price growth is much higher than per capita income growth.

It’s way higher than rent inflation and CPI excluding shelter. Coming price growth weakness in the next few months will look more like the decline in the mid-2010s than the late 2000s.

Price comps will be impossibly difficult next year. Current comps are modestly easy, but the main reason why housing is so strong is the decline in interest rates. Long term trend towards single family housing is aging millennials and the short term trend is people moving out of cities. Housing was particularly strong in the summer because sales from March were delayed due to the pandemic.