September PCE Shows Better Income Growth

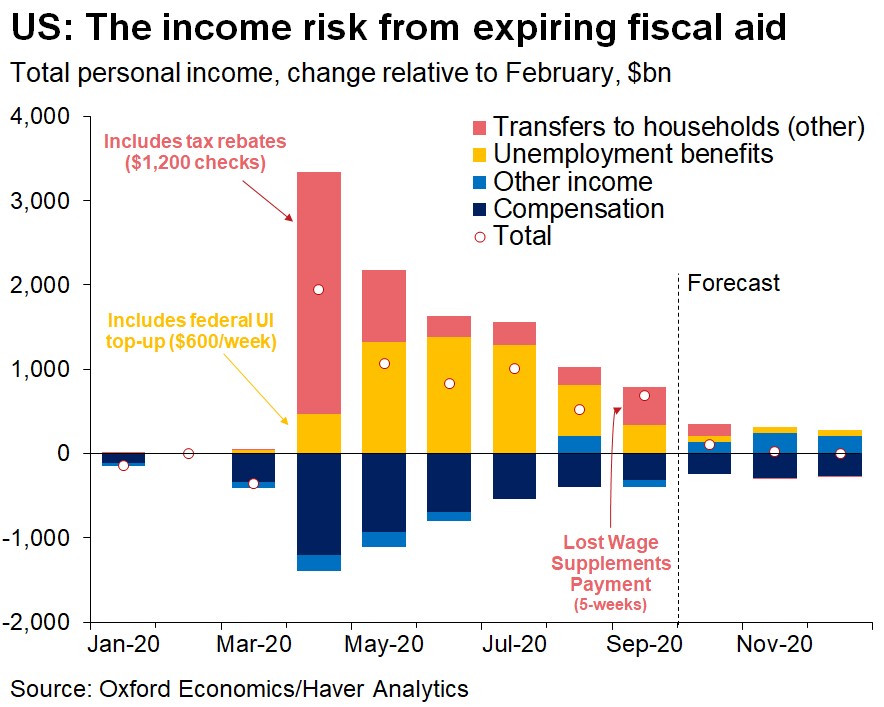

Monthly personal income growth in September was 0.9% which beat estimates for 0.3%. This was a good reading because the comp was revised higher by 2 ticks to -2.5%. Obviously, the comp was still easy. Yearly personal income growth rose from 5.5% to 6.2%.

One problem with this reading is it was generated by the lost wage supplement payments. Also, the $300 in weekly unemployment benefits went out all at once in September. Getting four $300 checks in September is literally the same as getting a $1,200 stimulus check. This money only went to the unemployed, so the total benefit to consumers was way less than the stimulus in April.

As you can see from the chart below, transfer payments spiked in September. This was like an accidental stimulus. It’s amazing because when the plan was first unveiled, many didn’t even think people would get money. It’s slowness in August caused a boom in September. Problem is that there won’t be another stimulus in the next few months. Obviously, October is already over; it looks unlikely that we will get one in November.

Good news is as stocks fall, the odds of a stimulus increase. The election is just about behind us. If there is a clear winner, we should get a stimulus if the S&P 500 falls another 5%. Some investors don’t support waiting for stocks to fall to help people, but that’s reality.

Declines are good in the short term. As you can see, the current forecast without any help pushes growth along the flatline. It's unlikely that we can anticipate a vaccine helping the economy by the end of the year either, so it might be accurate.

PCE Growth Also Beats Estimates

It’s no surprise that with income growth being boosted by government spending PCE spending growth also beat estimates. Monthly growth was 1.4% which rose from 1% and beat estimates for 1%. Remember, August’s reading was unsustainable as income fell and spending rose.

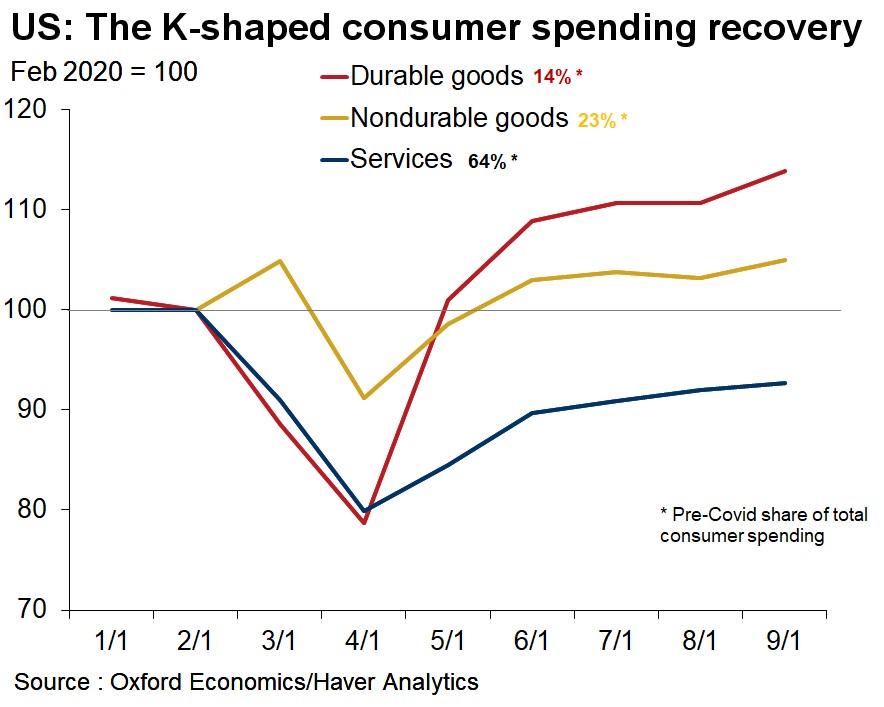

Yearly PCE growth improved from -1.9% to -0.6%. This shows spending hasn’t fully rebounded to where it was before COVID-19, but we are close. As you can see from the chart below, durable and non-durable goods have fully recovered while spending on services hasn’t.

Real consumer spending was up 1.2%. Spending on durable goods rose 2.9%, spending on non-durable goods rose 1.7%, and spending on services was up 0.8%. As you can see from the chart above, the share of spending in each category shifted sharply.

Services were 64% of spending, so essentially 2/3rds of consumer spending is still weak. That shows how powerful the uptick in spending on (durable & non-durable) goods was. Goods spending is up 7.8% from before COVID-19 and services spending is down 7.3% since then.

Quite frankly, even if consumers get stimulus checks, most can’t see how they replicate this spending on durable goods as their homes are stocked with new refrigerators and washer/dryers. Home improvements usually last a long time. If a household improved their kitchen, they won’t be doing it again in 2021.

In a scenario where we need social distance in 2021, people will save more money. Speaking of savings, in September, the savings rate fell from 14.8% to 14.3%. It’s still extremely high as incomes are weak, people are relying on the government, there is uncertainty, and spending options on services are more limited.

Reverse Of Conference Board

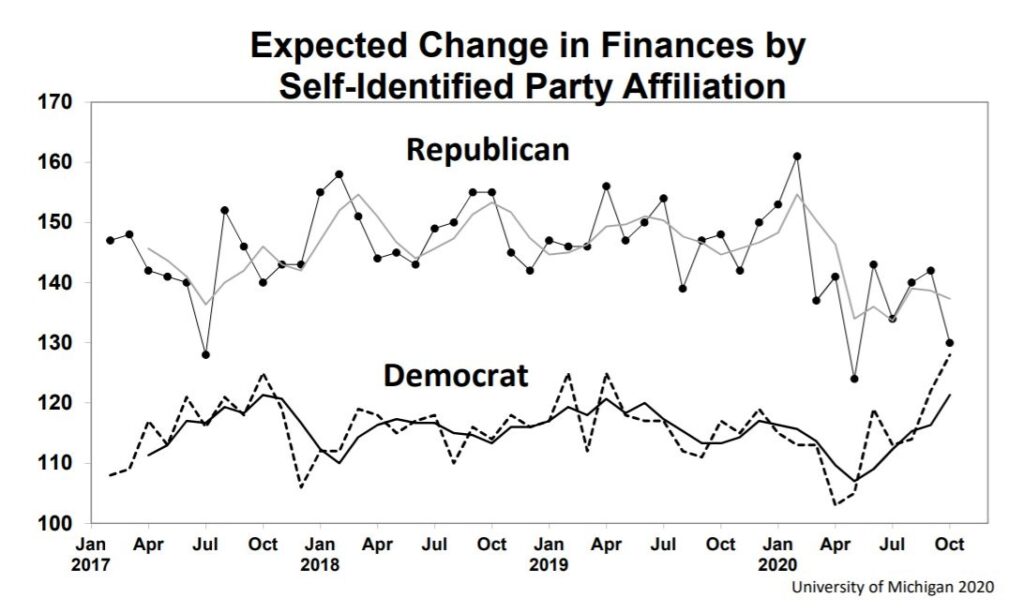

University of Michigan consumer sentiment reading was the exact opposite of the Conference Board survey since current conditions fell and expectations rose. That’s weird, but keep in mind these are small changes. Overall index rose from 80.4 to 81.8 in October even though the news is very scary. The stock market has been weak and COVID-19 cases are exploding in the Midwest and Western Europe.

Current conditions index was down from 87.8 to 859 and the expectations index was up from 75.6 to 79.2. Expectations were up because of optimism. As you can see from the chart above, Republicans seemed to have become less optimistic about their future finances and Democrats became more optimistic. A stimulus would help finances, but it won’t be enough to make up for income losses unless the $600 in weekly unemployment benefits comes back.

October Spending

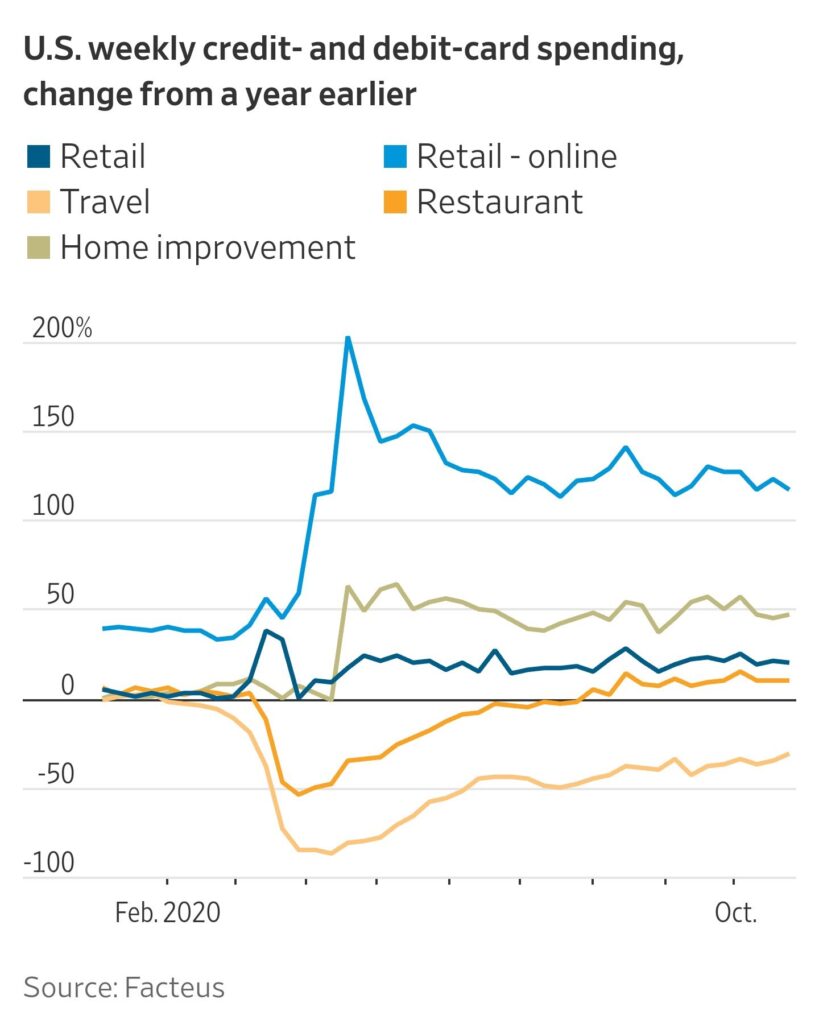

PCE report was from September because it is always a month behind. As you can see from the chart below, yearly spending growth didn’t change much in these select industries. Biggest improvement was in travel spending growth, but this industry isn’t jumping for joy because it’s still down over 30% and the renewed outbreak is going to reverse this trend.

3rd Wave Is Exploding

We must be open to the possibility of the 3rd wave being worse than the prior 2. It’s still not a base case, but each day it looks more likely. There were 97,080 new cases on Friday which was a record high. Of course, there are more tests than the summer and about 12 times the number of tests as in the spring. There are now 1.225 million tests per day.

That’s almost exactly at my prediction of 1.25 million. Next goal we can set is 2 million tests per day by the end of the year. Clearly, these tests aren’t doing anything to stop the spread though.

Hospitalizations increased to 46,688 which means it looks likely that we will pass the summer high of about 60,000. We don’t know the spring high because many states didn’t report the numbers. It could have been above 80,000. Deaths are becoming more important to look at because they accurately depict how bad the outbreak was in the spring.

This wave has been in place for over 1 month which means enough time has passed for the spike to lead to deaths. So far, it isn’t a disaster yet as the 7 day average of deaths is 799. That’s over 20% lower than the summer spike. It would be a huge victory if the 7 day average stays below 1,000 throughout November.