Solid Jobless Claims Report Again

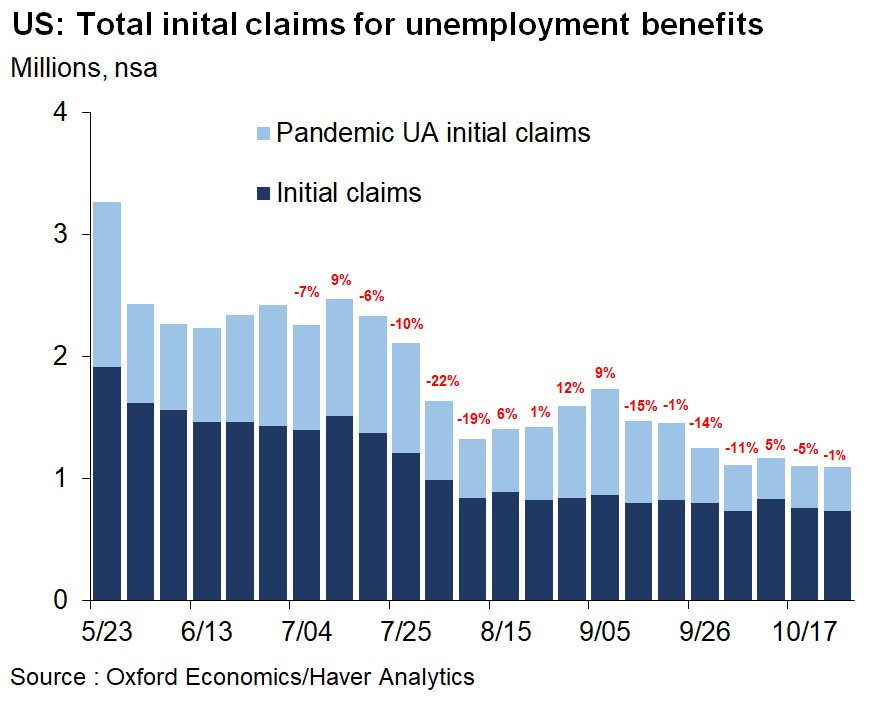

Even with all the COVID-19 mania and fears of a slowdown, the jobless claims report in the week of October 24th was good again. That’s 2 good weeks in a row. Seasonally adjusted initial claims fell from 791,000 to 751,000 which was below estimates for 758,000 and just 1,000 above the low end of the range.

Non-seasonally adjusted claims fell from 761,000 to 732,000 which is about 1,000 above the cycle trough 3 weeks ago. It seems like the spike in COVID-19 cases hasn’t hurt the labor market yet. That makes sense because the industries that are hurt the most by COVID-19 aren’t going to shed many new jobs. They already lost jobs and shuttered.

This latest outbreak just means the recovery will take longer to play out. Experts believe the economy will reopen next year. That’s when we will see the initial claims reading go back to normal expansionary levels.

As you can see from the chart above, the combination of PUAs and initial claims fell 1% which was the 6th decline in 7 weeks. PUA claims were up 15,000 to 360,000. PUAs don’t matter on a week to week basis because the data isn’t accurate. It wasn’t accurate this week either as PUAs in Nevada were up 45,000 to 58,000. Without that ridiculously large increase, national PUAs fell.

Adding to the good news, in the week of October 17th continued claims fell from 8.465 million to 7.756 million. On the one hand, that was the smallest decline since the week of September 12th. On the other hand, we are closing in on the May 2009 high of 6.635 million. This is becoming more of a normal recession.

Rate of decline in continued claims should fall in the next few weeks because there are fewer people left to leave it and because we are ending the period where the main swath of job losers will have their benefits expire. October is 6 months from April. There weren’t as many job losers in May as April, so fewer people will lose benefits.

A big negative catalyst no one is looking forward to is when the pandemic unemployment claims stop paying out at the end of the year. Government will likely extend them, but if they don’t, we could have a double dip recession. There are currently 3.68 million PEUCs.

There is no way a vaccine comes in time to get these people jobs by the time their benefits expire. It's likely there will be a vaccine by the end of the year. But by then it will only be given out to the most vulnerable. It will likely take until next spring to have the economy fully reopened.

In the week of October 10th, there was a 387,000 increase in PEUCs which actually isn’t terrible. There was a 510,000 increase the week before and an 823,000 increase the prior week. Remember, we want smaller increases. In the week of October 10th, non-seasonally adjusted continued claims fell 926,000 which means they fell more than PUECs increased. Labor market continued to heal.

Winners & Losers In Q3

Quarter over quarter annualized GDP growth was 33.1% in Q3 because of the very weak comp. This time it doesn’t make sense to look at the data like that. Instead we can say, GDP is down 3.5% from before COVID-19. Consumer spending was down 3.3%, and business investment was down 4.9%. Residential investment was up 5.1% as the housing market was strong. Exports fell 15.3%, and imports fell 7.1%. Federal government spending was up 2.6%, and state & local spending was down 1.9%.

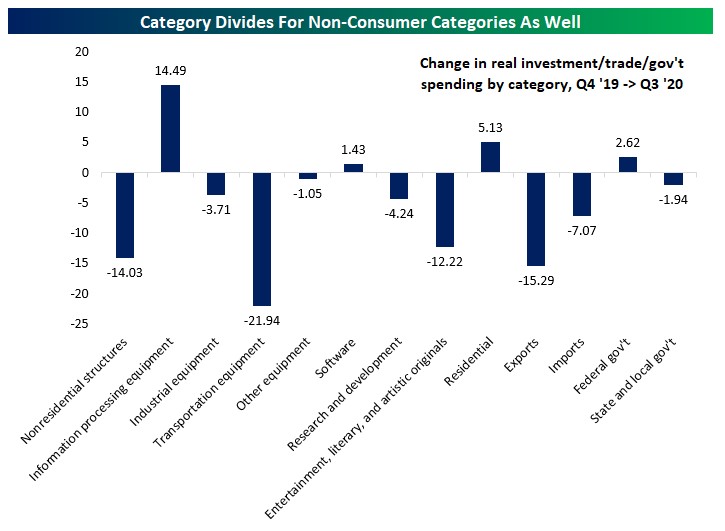

The chart below shows the changes in real growth from non-consumer categories. As you would expect, from Q4 2019 to Q3 2020, there was a 22% decline in transportation equipment investment and a 14.5% increase in spending on information processing equipment.

On the consumer side, using this same time span, there was a 21.3% increase in spending on recreational goods and vehicles and a 9.2% increase in furnishings and durable household equipment. People bought refrigerators and washer/dryers. Those goods aren’t going to be purchased again.

Demand for durable goods was pulled forward by the pandemic which means demand in 2021 came in 2020. On the other side, recreation services spending was down 32.4% as people went on fewer vacations. Spending on food services and accommodations fell 19.5%. This shows how far we are away from normalcy when it comes to spending money at restaurants.

Stimulus Effects

There needs to be a stimulus in the fall, not in early 2021. If we get a vaccine in November and it starts going out in December, the economy should be able to reopen by February or March.

If a stimulus passes in late January, the money will be given out just as people in hospitality and services are getting their jobs back. We might get an economic boom which is why yields will increase. 10 year yield can rise to 1.5% in that scenario.

This possibility is why the 10 year yield is still at 81.4 basis points even though COVID-19 cases are spiking and we have no stimulus now. 10 year bond isn’t as negative on growth as the stock market has been in the past 2 weeks.

Conclusion

Jobless claims report showed improvement and the Q3 GDP report was good. The stock market is still worried about the next 2 months though. No past reports matter because it sees doom ahead with cases rising. On Thursday, the number of people hospitalized rose to 46,095. Two more weeks of bad data would make this wave worse than the one in the summer.