Worries Are Here

Even though firms literally just reported great earnings this week, worries are back because traders believe Q3 is meaningless now that the economy is worsening. That’s true to an extent. The economy will be in worse shape in November because of COVID-19.

A difference between investor fears and these earnings reports is timing. Companies aren’t yet experiencing the weakness investors anticipate; they can’t give specific negative guidance until the weakness starts. Uncertainty is rising which scares traders.

One potential mistake the market could be making is that companies might be better able to adapt to the shutdowns than this spring. Plus, the market could be overestimating the coming spike in COVID-19 cases. The market is bipolar. Two weeks ago, the market ignored the rise in COVID-19 cases. There were some hopes for a stimulus and a vaccine. Now the market has decided the economy is going to tank next month.

A vaccine was expected by the end of October back in September. We have known for a couple weeks that the results were coming in November. That isn’t news. Plus, two phase 3 trials restarted in America last week. There is no reason to fear the lack of vaccine news unless you don’t have the patience to wait another 3 weeks.

Right now, the COVID-19 data looks bad, but it also looked bad prior to the past 2 peaks. There is no guarantee that this spike will be worse than the prior two. Investors fear the worst because France has seen record cases. However, keep in mind there is more testing now and there weren’t serious precautions taken until a few days ago.

Recovery Stalling?

The stock market is overreacting to the potential headwinds the economy faces in November. We are seeing COVID-19 headline risk. We are seeing more cases and more lockdowns which scares people. The situation is more nuanced. We could be looking at the recovery stalling rather than a crash. That’s what was said prior to the recent strong jobless claims report. We know the economy is improving at a slower pace, but we don’t know if it is fully stalling.

Keep in mind, all the economic data we have is from October. Investors are even more scared of November because there will be more cases and lockdowns. Obviously, the biggest fear is lockdowns for the entire winter until March without a fiscal stimulus or a vaccine. Good news is if stocks keep falling, a stimulus and Fed support will come. If a vaccine comes out in November, the most vulnerable will get it by the end of the year. Deaths this winter will be limited.

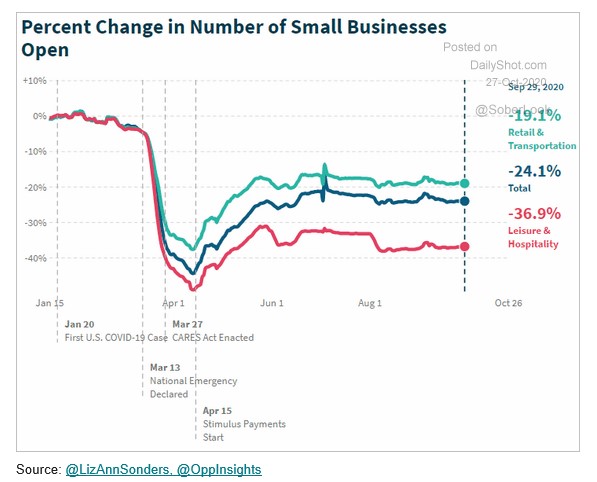

Getting back to the speed of the recovery, the chart above shows the small business recovery is stalling out. This is much worse than small business confidence which has nearly recovered all its recessionary losses. As you can see, in mid-October there was still a 24.1% decline in the number of small businesses open from January.

This chart reinforces the point I made earlier about the market being bipolar. There was evidence that the economy may have been stalling when the S&P 500 was near its record high 2 weeks ago. The market ignored the bad news until it couldn’t any longer. Now as stocks fall, the market is overreacting the other way. It takes a lot of guts to buy now because of the negative headlines, but it also took guts in March and April and that worked out well.

No Improvement In The Labor Market

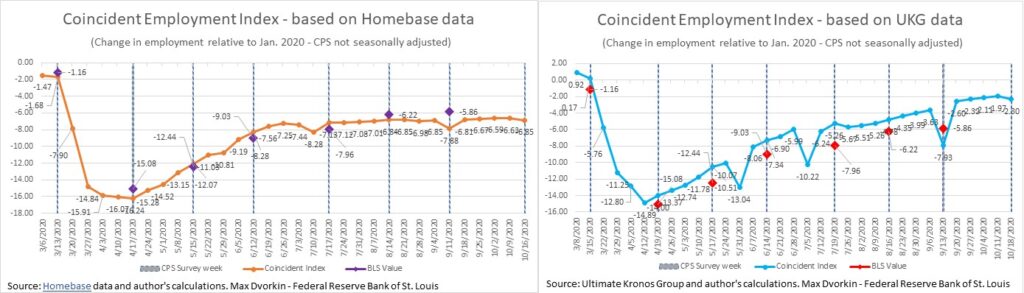

Jobless claims are the most important high frequency data point on the labor market, but it isn’t the only metric. As you can see from the chart on the left, the Homebase coincident employment index didn’t change 4 weeks in a row and then fell slightly in the past week. It has hardly improved since July. That's guessing that job creation will be positive, but it won’t be that strong.

The stock market’s reaction to the report next Friday will depend on where stocks go from here until then. If stocks fall, any job creation, as long as it is positive, will be enough to push stocks up. Most people’s understanding of the economy will be supported because the consensus is the recovery is slowing.

Maybe a good report will be ignored because everyone is so focused on November when COVID-19 will be worse. The chart on the right shows slightly better results using EKG data. It’s probably more accurate, since we can see little evidence of negative job creation.

Housing Is Still Strong

Housing market is still doing well. Such high price growth might limit demand especially if it comes along with higher rates. Luckily for housing, rates are falling as investors fear an economic slowdown. August FHFA home price index was insane. As you can see from the chart below, yearly growth rose from 6.5% to 8%.

Housing is on fire. This type of price growth is unsustainable as it is the highest since March 2006. Peak growth in the 2000s housing bubble was 10.7%. Unless we have a scenario with very easy comps, such growth won’t happen again.

MBA applications index also was strong. In the week of October 23rd, the composite index was up 1.7% which followed a 0.6% decline. Refinancing was up 3% after increasing 0.2%. Average 30 year fixed mortgage rate was 2.8% last week which was a record low. Purchase applications were up 0.2% after falling 2%. Yearly growth was 24%. There has been double digit growth for 23 weeks in a row.

It's interesting that Zillow stock is crashing. The stock is down 18.6% since October 5th. Housing is still doing well. This might be company specific as its house flipping business can’t generate a profit. It is one of the bubble tech stocks. The firm is expected to make 50 cents in 2022 which gives it a 179.3 PE ratio. That’s higher than any stock most would ever consider buying for the long term.