Monday Blues

The stock market had a rough Monday, although it did rally solidly off its afternoon low. S&P 500 fell 1.86%. It increased 1.06% from its low at 1:35PM. It’s fairly common to see the market bottom between 2:30 PM and 3:30 PM on big down days, but this bottom was earlier than usual.

Of course, sometimes the market closes at the lows. It does that just enough times to confuse you. One theory is that stocks bottom from 2:30 to 3:30 because of margin calls. We are back to hearing questions about a potential double top now that stocks are down 3.8% from the October 12th high.

We have more important things to worry about than the technicals. A main worry is the spike in COVID-19 cases without a stimulus passing. This is like a redo of the spring except there isn’t help coming. A main benefit we have now as compared to the spring is we know more about COVID-19. There is less uncertainty over its effects.

As far as health is concerned, the ability to treat the virus and slow its spread are better. Why does the virus spread if we know how to contain it? Because policymakers and citizens become lax. Plus, by doing more activities indoors because of the cold weather, it’s easier for the virus to spread.

With the increased restrictions and more cautious behavior, it seems like the spike in Midwest cases is near its crux. But lots of people have been too early in calling for a peak before. Number of cases per person in the Midwest is higher than any peak in the other 2 waves in the other 3 regions. There is more testing now than in the spring. And the number of cases per person in the northeast would have been much higher in the spring if there was more testing.

Details On The Selloff

A deep selloff was bad for the cyclical small caps which makes sense because higher COVID-19 cases without a stimulus are terrible for the economy. We are likely facing a tough situation in the next 2 months, but it will be tough to ignore the potential for a stimulus early next year once the election is over.

Furthermore, COVID-19 won’t be as much of a worry if better treatments and vaccines come out in November. That’s why even though the next few weeks look dire, many investors are holding on now.

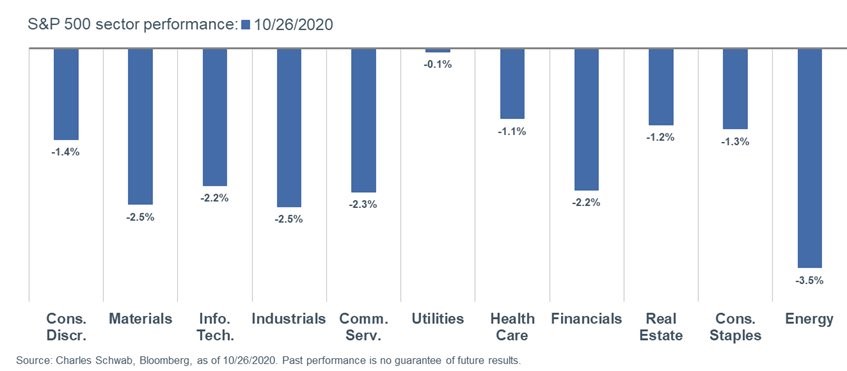

Nasdaq fell 1.64% and the Russell 2000 fell 2.15%. Apple was the only Dow stock that was up as it increased 1 penny. As you can see from the chart below, energy was the worst sector as it fell 3.5%. Hasn’t energy fallen enough? Apparently, the answer is no. WTI oil fell over 3% to a $38 handle. That’s not an egregious decline since there are fears of a spike in cases.

Generally, it has been bad to buy energy based on hopes for the future unless it is very oversold. It is oversold as ExxonMobil is down 39% from its June high. BP hit a record low today. It fell below its March bottom. And it's unlikely that most energy stocks will hit a new low. This is like how Wells Fargo hit a new low, while regional and community banks rallied. Wells Fargo is a laggard in good and bad times.

Tech actually sold off, so it wasn’t immune to the worries. Cloud index fell 1.46%. Fastly and Draftkings are in bear markets. They are down 42.5% and 37.8% since their peaks in early October. Draftkings fell 7.1% on Monday. As you can see, the utilities were the best performers as they lost just 1 tenth. That’s because interest rates have been falling. 10 year yield is down from its peak last week of 86.6 basis points to 79.9 basis points.

Growth Is Too High

We have gone over this many times in the past few months, but it’s worth reviewing again because such a powerful trend is coming to an end.

As you can see from the chart below, the 25 largest growth firms have gone vertical in relation to GDP. The chart shows the 25 firms are 62% of America's GDP. That’s such a short list of firms (which everyone can name) to make up almost 2/3rds of the economy. A peak in 1973 was only 16% and the peak in 2000 was 39%. If these stocks crash, they will take down the whole market.

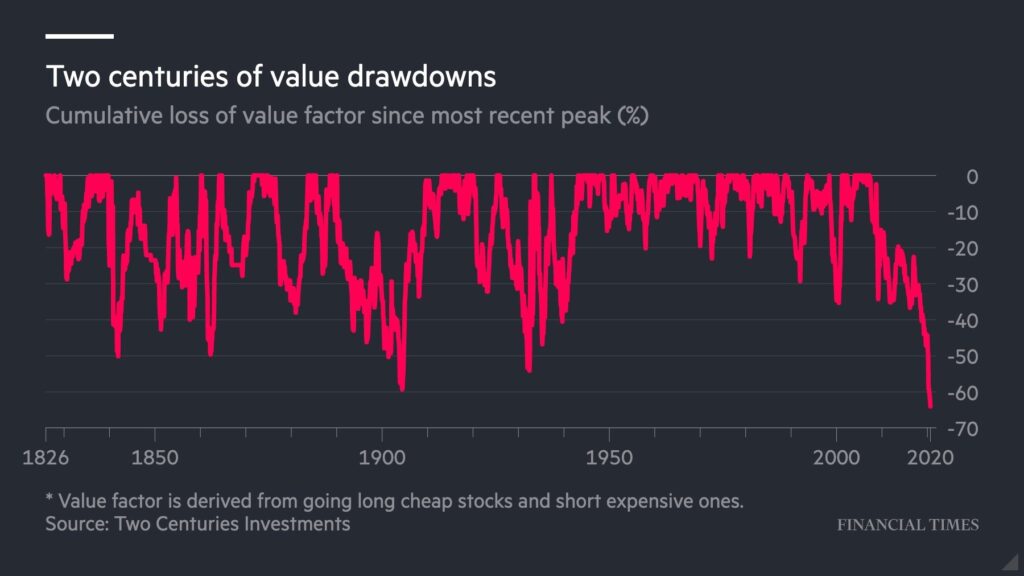

As you can see from the chart below, value stocks are cheaper in relation to growth stocks than at any point since 1826. This makes sense because interest rates are at record lows. Growth is hard to come by. Meaning, people are buying companies that can grow sales even if they will never make a profit. Best SaaS company, Snowflake, isn’t expected to make a profit through 2023. If interest rates rise, Snowflake will fall dramatically.

COVID-19 Is Rampant

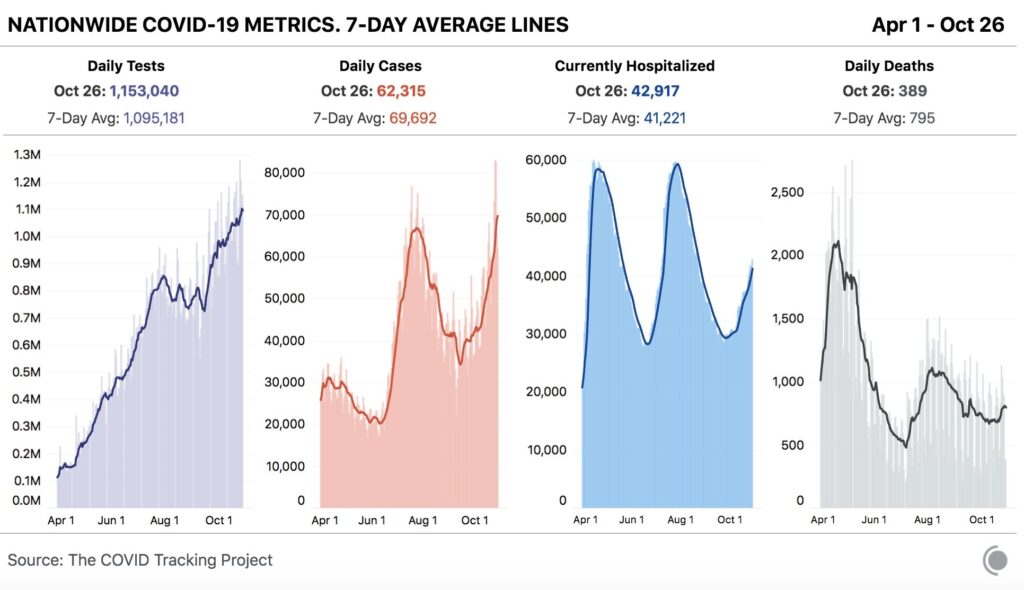

COVID-19 cases are increasing rapidly. Obviously, testing is increasing too, but the positive rate is soaring in the Midwest, meaning the virus is spreading. As you can see from the chart below, there were 42,917 people in hospitals because of COVID-19 which is a major issue because it rose from just 41,753 the day prior.

If hospitalizations rise at a 1,000 per day pace, we will see a new record high in 18 days. Frankly, we shouldn’t expect that. It’s just to explain how quickly the situation appears to be deteriorating. If we are to see another lower high in hospitalizations, then the peak must come in November.

Either way, we can all expect this wave to end before the vaccine and treatments come. That’s not to say they aren’t important. Even when we are at a trough, hundreds of people die per day. Furthermore, we need to prevent a 4th wave. If we see a peak in cases in Wisconsin and France (the original hotspots in this wave), some investors focused on leading indicators will calm down.

That’s like how stocks bottomed when Italy started getting less bad in late March. Currently, the 7 day average of cases in France and Wisconsin are 36,428 and 3,880. France is at a record and Wisconsin is 28 off its record it hit on Sunday.