New Home Sales Actually Miss Estimates

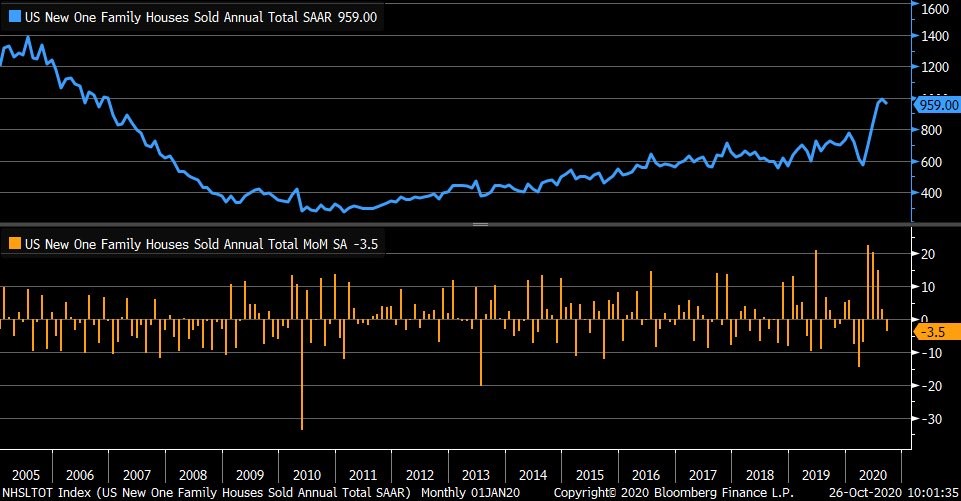

The impossible happened. A housing data point missed estimates. New home sales in September fell from 994,000 to 959,000 which significantly missed estimates for 1.016 million and the lowest estimate which was 1 million. Furthermore, the August reading was revised lower from 1.011 million. The chart below shows this is the first monthly decline since April.

It’s amazing to look at the spring’s data because you wouldn’t be able to tell by looking at this that we had a terrible recession. Housing was crimped by the stay at home orders, but once those were gone, we were back to normal. In a couple months, the housing market got hot because rates were so low.

Median new home prices were $326,800 which was 3.5% yearly growth. The average selling price was $405,400. This wasn’t a bad reading just because sales missed estimates though. New home sales were still up 32% yearly. That’s not on an easy comp either.

We will comp the easy numbers next spring. There is a 3.6 month supply of new homes which is an uptick from 3.4 months, but still very low. It’s one of the lowest readings ever.

When supply is below 4.3 months, it’s excellent from home builders and when it’s below 6.5 months, starts grow. We’re quite far away from an oversupply. If rates were to suddenly spike, that would happen quickly, but until then, housing is in great shape. Northeast had a 29% decline in new home sales. Midwest and south had 4.1% and 4.7% declines. West was up 3.8%. Forest fires didn’t stop the West in September.

TSA Checkpoint Numbers Lag

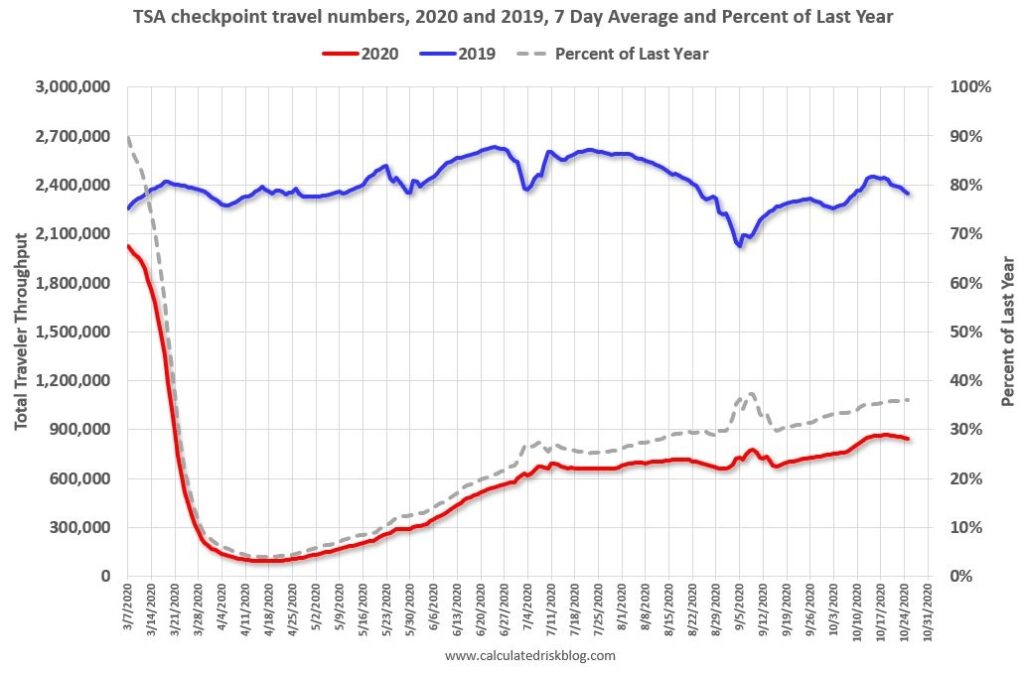

Last week, it was noted that TSA checkpoint travel numbers had been strong still despite the major spike in COVID-19 cases. This week, we are starting to see evidence of a decline. There has been week over week decline for 7 straight days which is the 2nd longest streak since late August.

As you can see from the chart below, there was weakness at this time of the year in 2019, so the weakness this month has been covered up on a yearly basis. That cover up probably won’t last as COVID-19 is leading to heavier economic/travel restrictions.

Angela Merkel of Germany plans what she called a ‘lockdown light.’ Politicians are very weary of complete lockdowns because they destroy the economy. Good news is AstraZeneca’s initial findings from its vaccine show it is producing an immune response in older adults.

Furthermore, Pfizer is releasing its results from its phase 3 vaccine trial in the 3rd week of November. Initially, the application for emergency approval was supposed to come in October, but an extra month of data was required by regulators; that’s why it was pushed to next month. Right now, we just have murmurs of potential good news. That should change in the next few weeks.

Dallas Fed Manufacturing Index Rises

In September, the regional Fed manufacturing indexes were mostly strong, but the ISM index wasn’t. The ISM index ended up being right because the industrial production report was weak. That happens sometimes. Even still, it's good to follow the regional Fed indexes because they give us the earliest look at how the month went.

Many investors are still bullish on the cyclical recovery. General activity index in the Dallas Fed survey was up from 13.6 to 19.8; the production index was up from 22.3 to 25.5. That’s despite the weakness in energy. Texas is a big energy state, but it has diversified itself by expanding in other industries in the past few years.

New orders index was up 5.2 points to 19.9. Outlook index was up 2.9 to 17.8, but the uncertainty index was up 4.3 to 11. The 6 month expectations for new orders index fell 11.1 points to 38.2. As the sector recovers, it’s harder to expect an increase (there is a higher base). October manufacturing ISM report comes out on November 2nd (this coming Monday).

Banks Having A Good Earnings Season?

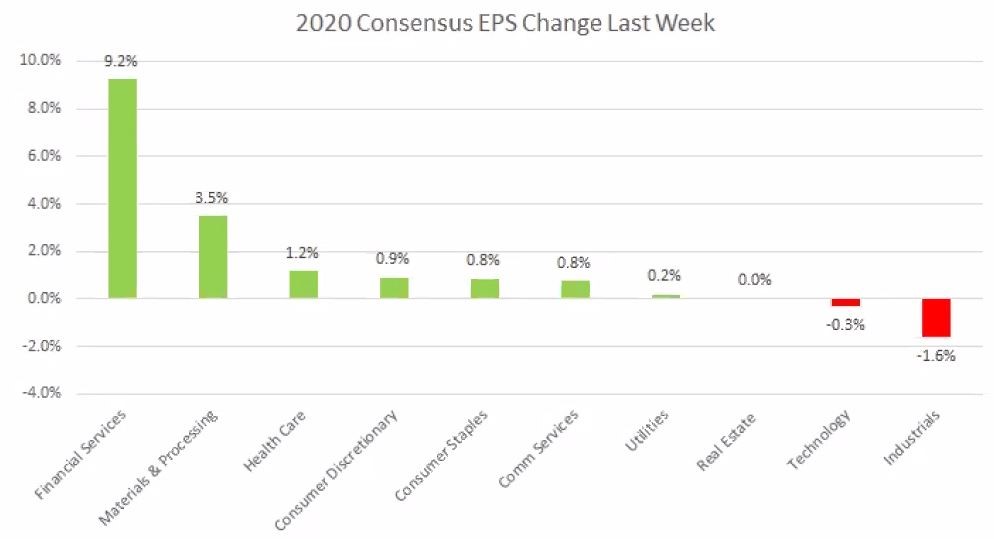

Sentiment on the banks is quite bad. However, they recently rallied in the past month on rising rates. Maybe they should be up anyway because they have been reporting solid numbers. They are well capitalized and have strong growth in deposits and mortgage lending.

As you can see from the chart below, as a result of their earnings, 2020 EPS estimates in the financial services sector rose 9.2% in the past week which was the best sector performance. Tech actually saw a decline of 0.3%. Obviously, this is only one week. Major FAANMG names (other than Netflix) still haven’t reported yet.

In Q3, the industries with the worst earnings declines were the usual suspects. Airlines had a 313% decline. That’s why many would be on the brink of failure if it wasn’t for government help. Hotels, restaurants, and leisure had a 133% decline.

Obviously, everything with a greater than 100% decline means they lost money. There were 4 industries in that category. Oil and gas firms had a 129% decline and oil services firms had a 68% decline. That’s why the energy sector is so hated. This is the worst cyclical decline it has ever faced. Z-score on energy ownership by funds is -2.1.

Part of the story that investors are getting wrong is they think fossil fuel usage is in terminal decline like coal. They are forgetting coal usage crashed because of cheap natural gas. When the energy cycle turns like it always does there won’t be bears claiming fossil fuels are dead. These low prices are causing projects to be canceled and small firms to go bust. That will limit supply in the future.

When oil demand returns as the economy reopens next year, there will be a supply shortage rather than a glut like we have seen this year. Energy stocks will roar higher very quickly. It will be just like the spike from late March to early June. As a reminder, ExxonMobil rose 74% in that period. On Monday, BP hit a new record low (below the March bottom).