Another Modest Decline

The stock market fell modestly on Wednesday with the small caps falling the hardest despite the outperformance of the banks. That’s because small cap growth stocks were weak again. It appears that the market is dealing with a bunch of factors at once. We have the uncertainty over the election. It’s worried about a potential stimulus.

Furthermore, it’s following earnings, COVID-19, and the rise in yields. By the way, Netflix fell 6.9% on its report. It has recently made a habit of falling on earnings and then recovering. It's unlikely that it will recover this time because if the economy is expected to reopen, less people will watch Netflix inside.

Dollar Decline

A recent trend has been a decline in the dollar, a rise in the Chinese Yuan, modest weakness in U.S. stocks, and a rise in the 30 year yield. As you can see from the chart below, the dollar versus the Yuan had its fastest 100 day decline since at least 2011. Dollar index is at 92.79 which is near its 2.5 year low.

30 year yield is up to 1.62% which is about 5 basis points from its June high. There appears to be some resistance at the June high which makes sense because COVID-19 cases are increasing and we don’t have clarity on the stimulus. We know it’s coming, but we don’t know its timing or size.

Wednesday’s Action Reviewed

Nasdaq fell 28 basis points and the Russell 2000 fell 86 basis points despite the 37 basis point rise in the regional bank index. Small cap growth index fell 1.27%. Semiconductor index is now on a 7 day losing streak. It’s only down 2.64% in that period, but it’s notable. Solar stocks imploded.

Invesco Solar ETF (TAN) was down 8.38%. Maybe investors are having 2nd thoughts about how much Biden will support green energy given the explosion in fiscal deficits.

The cloud stock index fell 1.87% as Zoom fell another 4.44%. It’s down 7.97% in 2 days which is crazy because there has been a massive spike in COVID-19 cases. You’d think that would be bullish for Zoom. Maybe investors are looking past this spike.

We will know it’s near its end when Wisconsin’s 7 day average of cases peaks. It was one of the first hotspots in the 3rd wave. 1 daily decline isn’t enough. We need to see the 7 day moving average stop rising.

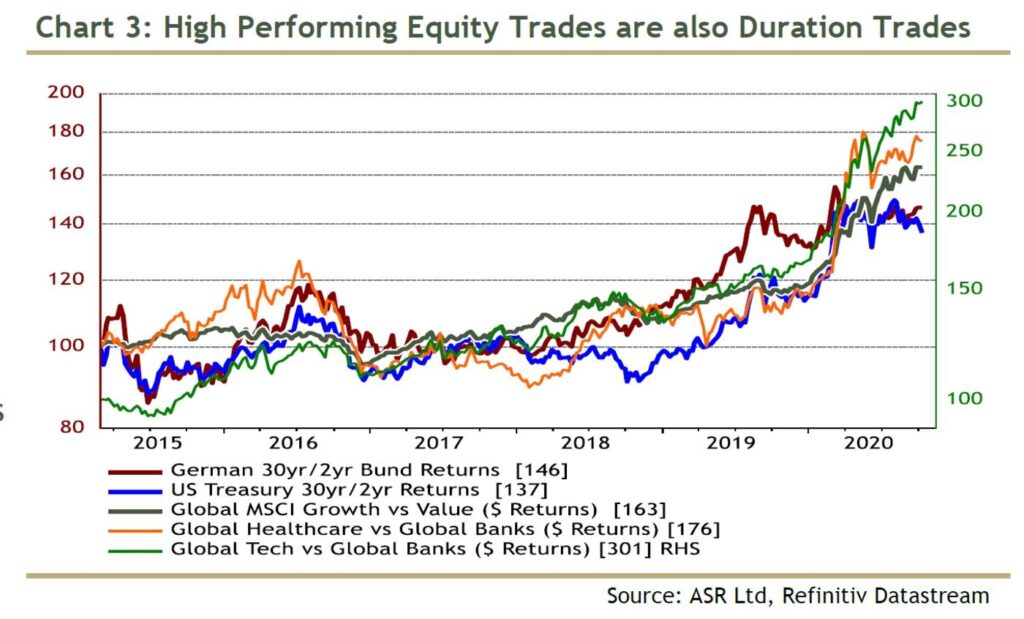

Everything Is A Duration Trade

The market has been in a duration trade for a while, meaning investors have banked on low and falling yields. Adifference now is that yields are so low, they are creating a mania. Bad news for risk averse investors is they have almost nowhere to hide. It makes sense to want to avoid this trade because yields are already near zero.

10 year yield probably isn’t going negative. The chart above shows the various relationships that have gotten unhinged because of the duration trade. Best place to hide is in energy and banks. A problem is energy has done so badly, you can lose 30% of your money before you blink.

99.9% of investors likely have less than 30% of their money in energy and banks combined. No one wins if rates rise which is exactly why they will rise.

Tesla Reports Another Loss (Excluding Tax Credits)

Tesla reported Q3 earnings on Wednesday. This continues to be by far the most controversial stock on Wall Street. I’ve never seen anything like it. The firm reported a profit, but that was only due to regulatory credits. Meaning, the debate on whether this company will ever survive without the government will continue.

Just making a profit isn’t close to enough to justify the valuation. Estimates call for $3.36 in 2021 EPS which would give in a 126 PE multiple. These are pie in the sky numbers. We will see how close Tesla gets very soon.

The firm reported 76 cents in adjusted EPS which beat estimates for 57 cents. However, the chart above shows the firm has lost money without tax credits 4 quarters in a row. That’s why it won’t be added to the S&P 500 anytime soon. It had $8.77 billion in sales which beat estimates for $8.36 billion.

It is well on its way to selling 500,000 cars this year. These are still small numbers. The company needs to be a major player in the auto market and sell full self-driving software at high margins to justify its current valuation. The bar has been set impossibly high.

This firm is already losing share in Europe even though most of the competition hasn’t come out with their full lineup of electric cars. Europe is a much bigger EV market than America because of intense subsidies. Tesla had $331 million in GAAP net income which missed estimates for $394 million.

Furthermore, the firm had $397 million in tax credits. Headlines would look terrible if next quarter tax credits fall substantially, causing the firm to lose money. It would prove the bears right. The stock didn’t react much to this report as it rose 3.2% after hours. It’s always hard to gauge this stock based on its earnings reports because its valuation is so much different than the business. It lives on hype, not the numbers.

For the past 8 years, the bears have been waiting for the next quarter to finally be Tesla’s undoing, but nothing happens. It’s difficult to expect the stock to crash on losses without tax credits since that’s not a new thing. This stock has been great for the longs. It has rallied on profits generated by tax credits. If it ever makes money from its actual business, we can only imagine how much it would rally.