September Fed Minutes

Fed’s Minutes from the September meeting were released on Wednesday. These Minutes stated, “Many participants noted that their economic outlook assumed additional fiscal support and that if future fiscal support was significantly smaller or arrived significantly later than they expected, the pace of the recovery could be slower than anticipated.” Fed strongly supports a fiscal stimulus as do many.

That being said, the economy was solid in August and September even without the stimulus. There is nowhere to go but up in the next 6 months as COVID-19 gets further under control. We can be fairly confident that there will be a stimulus at some point because both parties appear to support it. However, the Fed is using its platform to lobby for one which makes total sense.

And the Fed stated the recovery in GDP has been “rapid” which is obviously true. This has been the quickest recession and fastest recovery ever. Fed mentioned how minorities and the poor would be hit the hardest by the lack of a stimulus. That’s exactly true, but they would also be helped the most by COVID-19 getting under control, so their outlook is positive. Obviously, if someone doesn’t have enough money for essentials, their first concern isn’t about 6 months from now. They are worried about now.

Their Minutes added, “with longer-term interest rates already very low, there did not appear to be a need for enhanced forward guidance at this juncture or much scope for forward guidance to put additional downward pressure on yields.” There is no point in locking in a forecast for rates.

Obviously, Fed wants to be flexible. The market already believes it that rates will stay low for years. Furthermore, there’s no point in trying to control the long end of the yield curve, because long yields are low too. Also, in the past few days long yields have risen, but rates are still low. Either way, that increase occurred after the Fed’s meeting.

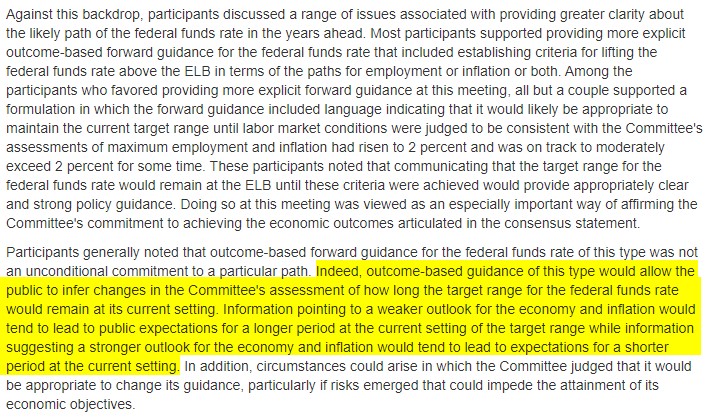

As you can see from the highlighted paragraph above, the Fed completely hedged itself by saying outcome-based guidance would lead to near zero rates only for a short time if there is a stronger economic outlook and inflation. Fed is already saying it would keep rates near zero for a short-term time if conditions surprise to the upside. Most investors believe the Fed will keep rates low forever, but some see a situation where it could raise rates as early as 2022.

If the leisure and hospitality industry fully recovers next year and we get a stimulus, we could be looking at below 5% unemployment by the end of the year and about 2% inflation. Some already correctly predicted the unemployment rate would fall below 8% by the end of the year a few months ago. That was an optimistic projection at the time; now it looks like the rate could fall below 7.5%.

Better Treatment Is Here

There will be better treatments by the end of the year. On Wednesday we got good news from Eli Lilly. Phase 2 of their treatment trials went well so they submitted a request for emergency use for monotherapy to the FDA. Lilly will be able to supply 1 million doses of monotherapy in Q4, with 100,000 in October.

Furthermore, there will be 50,000 doses in Q4 for combination therapy. That supply will increase further in Q1 as the firm announced a manufacturing collaboration with Amgen.

Screenshot below shows the strongly positive results from combination therapy and monotherapy in lowering hospitalizations and emergency room visits. One of Lily’s main goals is to get its treatment out before the vaccines come out.

Timeline has generally been that rapid testing would come first, then better treatment, and then a vaccine. There is an onslaught of potential solutions for COVID-19 coming by the end of the year. That’s why many are optimistic on the potential for a return to normalcy in 2021.

COVID-19 Update

Taw total of deaths has fallen below the average from 2015 to 2019. That means there aren’t any excess deaths. Our main concern is obviously COVID-19. Keep in mind, that with the lack of travel, there will be fewer deaths from all other activities.

It’s certainly possible that less exercise and less human interaction made people less healthy, but that’s more of a long term issue. Point here is, all else being equal, there should be fewer deaths than average. COVID-19 is still killing people, but not enough to make up for the decline in risky activities.

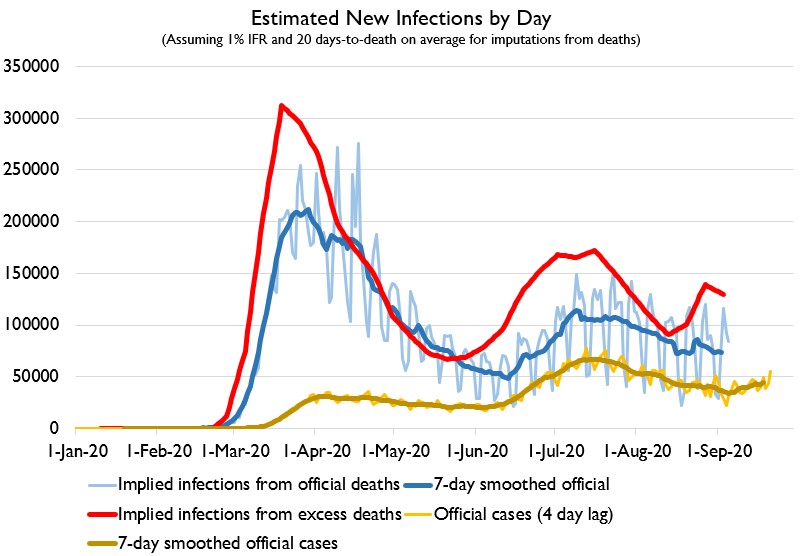

As you can see from the chart below, the implied infections measured by excess deaths shows the spike in July was much less than March/April. To be clear, treatment got better in the summer. On the other hand, testing was much sparser in the spring.

It’s great to see that the implied infection rate fell in the first week of September. To be clear, this doesn’t forecast results. As more people go to the hospital, deaths will increase. We can expect to see a modest increase in deaths in the 2nd half of October.

According to the COVID-19 tracking project, the data was pretty bad on Wednesday as the virus got worse. There were only 850,784 new tests, yet 50,602 new cases. Peak in cases on the week has moved to Wednesday from Tuesday. There were 916 new deaths which pushed the 7 day average down to just 667. We have finally reached the point where deaths don’t spike over 1,000 any day of the week.

Biggest issue with the data is that there were 32,124 hospitalizations which means deaths should increase modestly within the next few weeks. Bad national data has been catalyzed by the Midwest. This isn’t anything new as that area has been a hotspot for about 3 weeks.

Montana and South Dakota both hit record highs in case counts. Many previously said COVID-19 couldn’t spread in areas with low population density, but here we are. Good news is the 7 day average of new cases in Wisconsin peaked on October 3rd. This latest round of hotspots should be under control by the end of the month.