Powell’s Jackson Hole Speech

Powell gave his Jackson Hole speech on Thursday. Not much changed, but the media reported it as a big pivot and the 10 year yield increased. 10 year yield went from about 68 basis points to about 75 basis points because the Fed suggested it would let inflation ramp higher than 2% before hiking rates. This is because higher inflation causes the long yield to increase.

Fed didn’t change much because it has been saying for years that it will allow inflation to get above 2%. And it wants the average rate to be 2%. Meaning, a temporary rise above 2% won’t cause it to raise rates because it has mostly been below 2% for the past decade. If the Fed sticks with that original goal, it won’t raise rates even if inflation gets to 2.5%. Context matters because when inflation rises Fed determines if the movement is sustainable.

Economists are treating the new inflation target as 2.5% and investors are saying the Fed won’t raise rates for 5 years. This is all guidance. Fed can change its mind at any moment. It can’t cut rates below zero, so it needs to be as dovish as possible. Considering that the July Minutes were interpreted as hawkish, it’s no surprise this speech was dovish.

Powell stated, this “robust updating” involved the Fed formally agreeing to a policy of “average inflation targeting.” This will allow inflation to be “moderately” above the Fed’s 2% goal “for some time.” Fed is all about open mouth policy. Remember, the Fed barely bought any corporate bonds.

It’s programs didn’t come close to hitting their limits. All it needed to do was give an announcement that it would buy some junk bonds, and that was enough to send the stock market higher and make financial conditions looser.

Powell addressed the critics of the Fed when he said, “Many find it counterintuitive that the Fed would want to push up inflation. However, inflation that is persistently too low can pose serious risks to the economy.” Fed critics say the Fed wants people’s cost of living to go up. The Fed believes higher inflation comes with economic growth.

Ultimately, this entire policy speech wasn’t a big deal because the Fed already was dovish. All primary dealers expected the Fed to raise rates by 2024. Secondly, the Fed has failed to push inflation to its goal anyway. The chart above shows the market still doesn’t see the Fed getting to 2% inflation (based on the 30 year breakeven rate).

Will more dovishness bring higher inflation or will it just create a stock market bubble? It's possible that the latter is what’s happening judging by the rise in the Nasdaq. It’s up 48.5% in the past year.

Housing Market Stays Strong

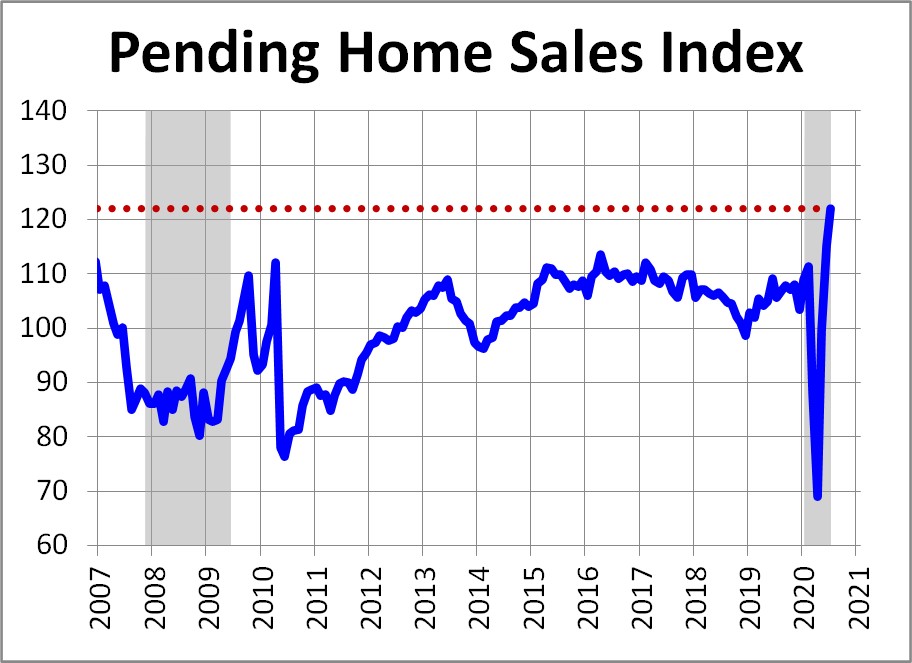

Pending home sales index was strong as you’d expect given the red-hot housing market. Toll Brothers stock is up 212% since March 23rd. Specifically, the pending home sales index rose from 115.3 to 122.1 as you can see from the chart below. That’s 5.9% growth on top of 15.8% growth. Estimate was for 1.5% growth. This has been a V shaped recovery. Right side of the V is stronger than the left side.

NAR’s chief economist stated, “If 20% more homes were on the market, we would have 20% more sales, because demand is that high.” This is mostly because of low rates. There are also some people moving out of cities and into single family homes because of the pandemic (people working from home). Current 30 year fixed mortgage rate is 2.91%. Lowest was 2.88% earlier in August.

In the MBA applications report from the week of August 21st, the composite index was down 6.5% weekly after falling 3.3%. Refinance index was down 10% after falling 5%. Banks aren’t lowering mortgage rates as much as the long bond yield indicates they can. We are at a floor.

With the recent rise in the 10 year yield because of the Fed’s stance on inflation, we might see mortgage rates creep up slightly. Worse the economy, the better the housing market because economic weakness leads to lower rates. Purchase index was up 0.4% after being up 1%. It was up 22% yearly, which followed yearly growth of the same rate.

Not A Great Jobless Claims Report

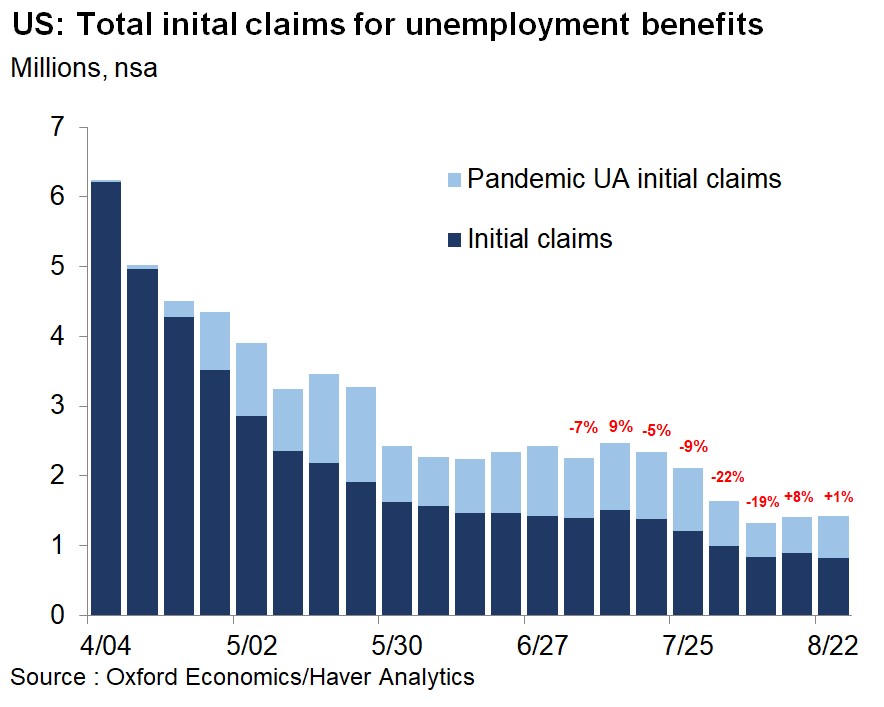

Jobless claims report from the week of August 22nd wasn’t great. It wasn’t a disaster either. Seasonally adjusted initial claims fell from 1.104 million to 1.006 million which was above estimates for 987,000. Highest estimate was 1.1 million. We’re still above the reading from 2 weeks ago.

Non-seasonally adjusted claims fell from 890,000 to 822,000 which is below the reading from 2 weeks ago. PUA claims were up 82,000 to 608,000. Total is 1.43 million. As you can see from the chart below, that led to a 1% increase from last week. Many were hoping for a low single digit decline.

Considering the rise in initial claims last week, the continued claims reading from that week was good. Continued claims fell from 14.758 million to 14.535 million. IFR Markets estimates that it will take 8 more weeks for continued claims to stay consistently below 10 million. That sounds good.

Abbott’s new testing kit that costs $5 and takes 15 minutes to give a result could allow the economy to reopen quicker. President Trump announced a $750 million deal for the purchase of at least 150 million rapid tests. This sent Abbott’s stock up 8%.

Abbott said it will “ship tens of millions of tests in September, ramping production to 50 million tests a month in October.” If this test works out, the economy could have a second leg to its recovery. The V shaped recovery in April and May can restart in October and November. In that case, we probably will see continued claims rapidly fall.