Different Market

The stock market was different on Friday. As per usual, the Nasdaq outperformed the Russell 2000 as the tech index was up 0.42% and the small cap index fell 0.76%. However, the rally was mostly in Tesla and Apple. The market’s breadth narrowed considerably. For example, the cloud index fell 0.97%.

Amazon, Microsoft, Facebook, Netflix, and Alphabet fell 0.38%, 0.73%, 0.74%, 1.12%, and 0.08%. Not even FAANMG can rally. This is now an AT market (Apple and Tesla). This can’t last. Best guess is Apple tops very soon and Tesla is the only stock that rallies for the next couple weeks before the entire growth trade ends.

On the day, Nasdaq rallied more than 0.4% to a 52 week high, yet only 29% of stocks in the index were up. This is the lowest in history by far. Next worst was a day in July. In other words, the index has never done this well with this few stocks going up. That makes sense because the Nasdaq started in 1971. Top firms are the largest since the 1970s.

Only opportunity for such bad breadth to occur was the 1970s, but there wasn’t euphoria then. Let’s compare this market to 2000. Then the top 10 stocks were 43.6% of the Nasdaq 100; now the top 10 have 58.6% share. Top 5 made up 30.9%; now it’s 47.1%. Top 3 made up 21.2%; now it’s 35.7%. Even European investors are betting on the Nasdaq as $3.3 billion or 28% of total European flows have gone to Nasdaq 100 products.

Sentiment Has Gone Crazy

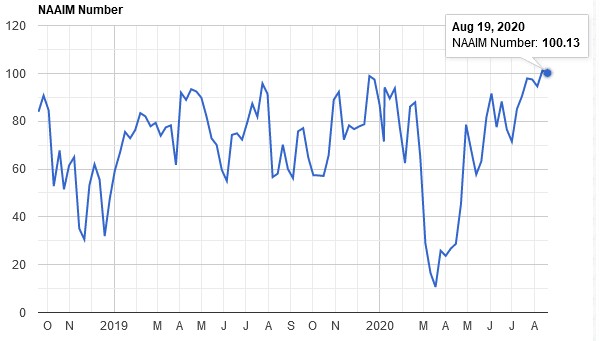

It was disappointing to find that the AAII sentiment survey barely changed as there were still more bears than bulls as the record extended further. Next week, there will likely be even more bears because the market’s breadth has been so bad and a fiscal stimulus hasn’t passed. Like expected, the NAAIM index stayed high. It was above 100 for the 2nd time as the chart below shows.

Record is 3 straight readings above 100. Last time there were 2 straight over 100 readings was December 2017 which was about 1 month before the short VIX trade blew up and stocks corrected. We're looking for a 15% decline in the S&P 500, a 30% decline in the Nasdaq, and a 10% decline in the Russell 2000. Financials will likely rally slightly. It feels very good to see your stock rally even 2% in a month where the major indexes crash.

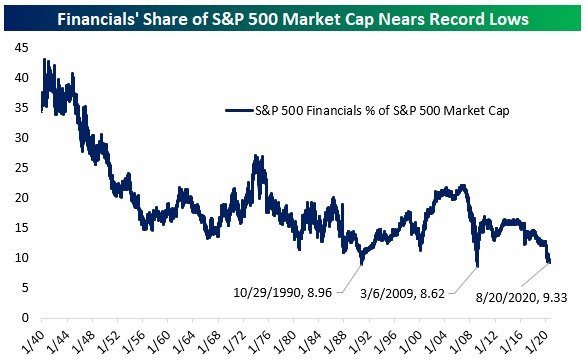

Irrelevant Financials

Financials are irrelevant. That whole sector is the size of Microsoft and Apple combined. As you can see from the chart below, this sector is 9.33% of the index which is only slightly above its record low in March 2009. This doesn’t tell the whole story because financial services have rallied, while the banks have been weak.

Specifically, stocks like Moody’s, MSCI, S&P Global, FICO, Transunion, and Intercontinental Exchange have done well, while stocks like JP Morgan, Wells Fargo, and the regional banks have done terribly. Regional bank index is down 20% since June 2006. That’s 14 years of weakness.

Nasdaq bank index is down 35% since March 2007. Since March 2000, JP Morgan stock is only up 60%. A bank run by the best banker in the country has only returned 60% in over 20 years (excluding dividends).

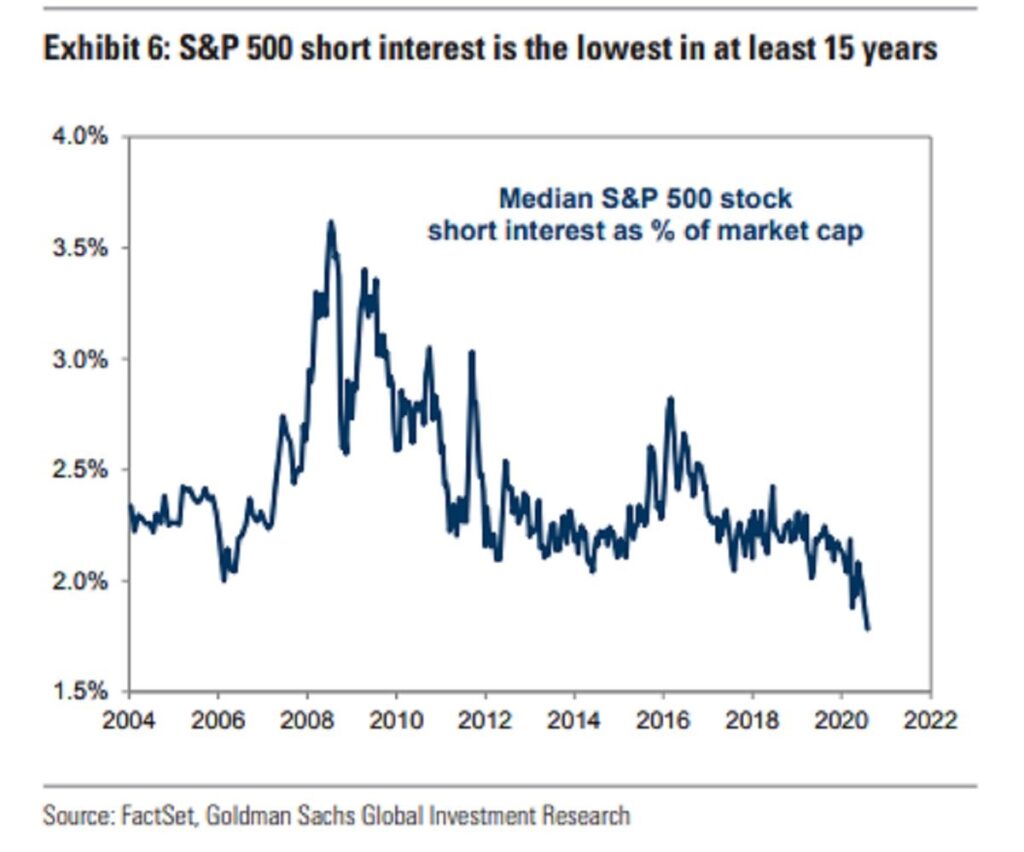

No One Is Short?

This seeminly isn’t a world for short sellers. Lately it seems like the worse the company, the better the stock does. Even if you knew Wirecard was a fraud, you probably didn’t make money in the short because the stock did well for years.

If the Tesla short sellers end up being correct, they probably won’t make money because so many have covered. Tesla shorts have been betting against the company for 7 years. Even if you’ve only been short for 3 months, you’ve gotten destroyed. If you were short via long dated puts a few years ago, your puts expired worthless.

As you can see from the chart below, the S&P 500 short interest is the lowest in at least 15 years. This is the most euphoric stock market since the 1990s. It’s closer to the 1920s because the economy is so bad. This chart shows the same thing the put to call ratio shows. It seems that no one believes stocks can go down.

COVID-19 Cases Fall Sharply Again

This week COVID-19 cases fell more than expected, but deaths fell less than expected. Specifically, there were 50,455 new cases which sounds like a lot, but actually isn’t because there usually are a lot of cases on Fridays. That was down from 60,015 last Friday. 7 day average has fallen to 45,022 which is close to the April peak of 32,471. At this recent rate of decline, it will fall below that peak in about 2 weeks.

On the other hand, there were 1,170 new deaths which was down 1 from last week. 7 day average has fallen, but not much. Some predicted the 7 day average would get to 800 by the end of the month, but it’s still at 1,022 with 1 week to go.

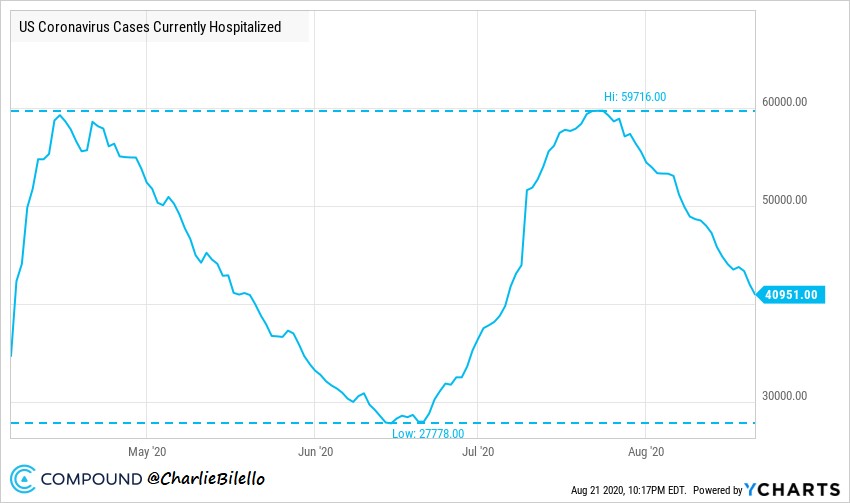

As you can see from the chart above, the number of currently hospitalized people has fallen from 59,716 in late August, which was slightly above the April peak, to 40,951. If the death rate stays the same as a month ago, new deaths should start falling very soon.

Conclusion

Only Apple and Tesla are left of the momentum tech trade as very few of the hot stocks are at their record highs. Nasdaq is possibly on the precipice of a 30% decline. However, the Russell 2000 should only fall 10% or less because the banks are already oversold.

Frankly, with Wells Fargo at $23.64, it’s hard to predict it even falling 5%. COVID-19 deaths are about to plummet since hospitalizations have been falling sharply for about 4 weeks.