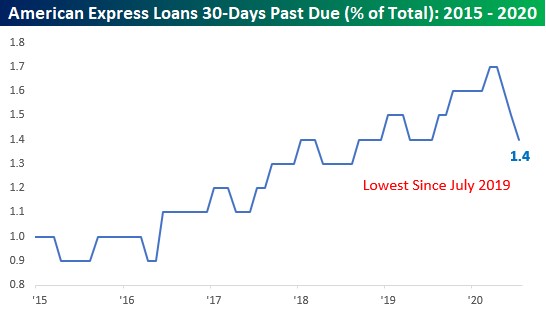

Delinquencies Fall Sharply

This was a unique recession because many who are poor and middle class actually made more money from unemployment insurance than they would normally earn from their jobs. As you can see from the chart below, 1.4% of American Express’ loans are 30 days past due. That’s down from 1.7% earlier this year. This is the lowest delinquency rate since July 2019. This has been a backwards recession.

It’s odd that the delinquency rate rose in the last cycle since consumers deleveraged. That’s probably because the source of the deleveraging was housing debt. That being said, credit card debt isn’t that high either (compared to the 2000s). Problem areas in the last expansion were auto and student loans.

We always knew unemployment benefits wouldn’t last. Cut off has been abrupt as it appears the $300 in weekly benefits given out in Trump’s executive order will take time to get sent out. Timing will depend on the state as many states will need to upgrade their unemployment systems. This is why the Democrats didn’t want to pay people 70% of their income.

In theory, it makes sense to pay everyone a percentage of their income, but the computer systems are in terrible shape. It’s like using a 15 year old computer. You won’t get very far with that. Even though the executive orders are turning out to be an insufficient safety net, Congress isn’t close to making a deal.

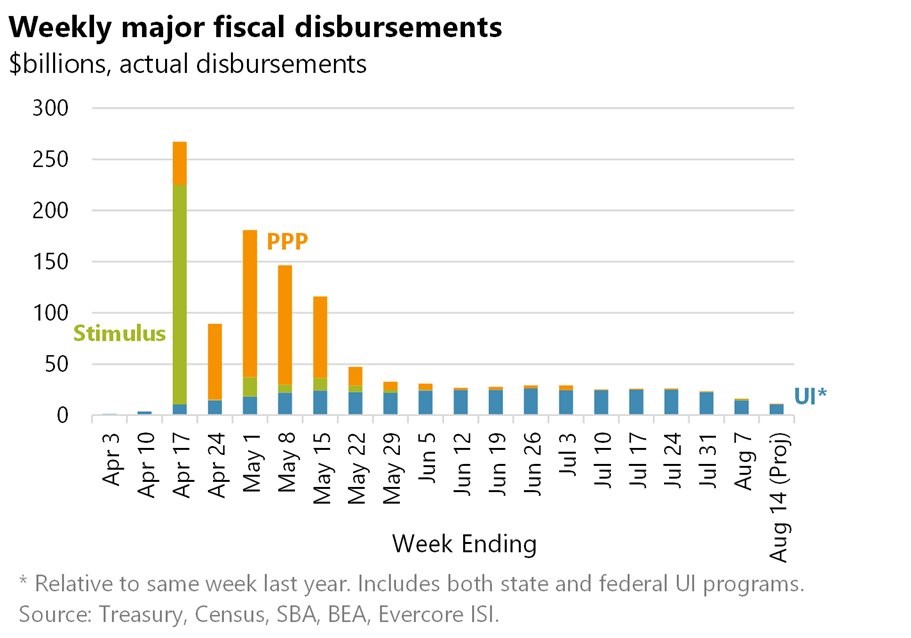

Lower Government Disbursements

It's fair to contextualize the decline in American Express delinquencies because the data was great in July, but the working poor might be in trouble this fall. So far, we have seen a decline in jobless claims and an improvement in Redbook same store sales growth in August. It appears to be a race against the clock. Consumers have some excess cash and are getting their jobs back. Question is if that’s enough to counter the decline in benefits.

As you can see from the chart above, fiscal disbursements have been declining since the spring and fell again this week. Unemployment benefits declined by about $15 billion per week which is almost 4% of GDP. Even still, COVID-19 cases have been falling and people have been getting their jobs back.

So far, there has been no weak data from August. Continuing claims were 15.5 million in the week of August 1st. They still have a lot to fall to get to the peak of 6.6 million in the last recession. If they fall 500,000 per week, it would take about 18 weeks to get back to that peak. Workers without a job who are getting small benefits are unlikely to last 4 more months without additional help. Even if it takes until September, it’s still important for Congress to get something done.

When Will Congress Act?

Some are saying that Congress won’t act unless they are forced to by weak economic data or a declining stock market. It’s not good for stocks or the economy if Congress needs bad news to act. It would be odd if a bear market in tech stocks causes Congress to act. That would arguably be a great combination for cyclicals because investors wouldn’t leave value stocks for growth to chase performance and Congress would be helping the economy.

A decline in tech stocks wouldn’t signal the economy is in trouble. These valuations can’t be maintained. Bubble will end regardless of whether Congress passes a stimulus. Best guess is these stocks fall for no reason. We’ve seen the economy weaken this summer.

Cyclicals fell and tech rose. We saw the economy rebound in May and August. In those situations, cyclicals and tech rose. Small cap value is outperforming in August, but most of the tech stocks are still doing well.

In July, Congress might have been motivated to pass a stimulus by a weak labor report. However, since the labor report was strong, so nothing got done. If we are waiting for a weak labor report, it might be a while. Even if the decline in unemployment benefits starts hurting the labor market in the 2nd half of August, it would take until the September report to see evidence, since last week was the BLS survey week for August.

That means Congress would see weak data on the first Friday of October. Nasdaq’s potential decline could come earlier. Election complicates everything. Maybe Congress might not want to act right before the election or maybe it will. It depends on how each party sees the political landscape. Any stock market decline might be blamed on the election, which means volatility might not force Congress’ hand unless it comes soon.

COVID-19 Update

There was another decline in COVID-19 cases and a small increase in deaths. That’s a continuation of the recent trend. There weren’t as many COVID-19 tests on Monday, but this wasn’t a one-off decline in cases; they have been falling for a few weeks. Hospitalizations have been declining sharply, but that hasn’t led to a big decline in deaths yet. That decline will likely occur this week.

As you can see from the charts below, the decline in COVID-19 cases have led to a decline in unemployment claims and an increase in department store foot traffic. That’s after the spike in cases weakened the labor market and department store foot traffic in July.

Specifically, there were 40,612 new cases on Monday which was down from 49,840 last Monday. There were only 37,682 cases on Sunday which was down from 48,011. These declines caused the 7 day moving average to fall to 50,800. It’s almost at my target of below 50,000.

There were 589 new deaths which was 20 above last Monday. After an initial decline in the first week of August, the 7 day average of deaths has been flat. Deaths will likely fall this week. A decline in hospitalizations should lead to a decline in deaths, but the impact has been slower than expected.