V Shaped Recovery In Retail Sales

It was wrong to be so negative on July’s economic data. Even though headline retail sales growth missed estimates, it was a pretty good report. We're still calling for a cyclical recovery. If August’s data is better than July’s it will be really good. We already saw how solid the recent jobless claims report was.

There’s nothing like eliminating the cause of the recession. In 2009, stocks rallied after the banking system was under control. Now, the cyclical stocks can rally once COVID-19 is under control. To be clear, it’s far from completely under control. However, stocks like to jump the gun. That’s a fair thing to do as cases have been falling.

Monthly retail sales growth was 1.2% which missed estimates for 2%. It was low because of the huge report in June which was revised from 7.5% to 8.4%. It’s hard to grow at all with such a tough comp. Almost everything about this report was great except auto and auto parts sales.

Overall real retail sales are actually 0.6% above the pre-recession peak. Sales got back to the previous high in 5 months which is the quickest recovery after a recession ever. It took 6 years for retail sales to recover after the last recession.

The stock market was right to recover so quickly. There are 2 caveats to that point. First, mostly tech has recovered. Cyclical stocks haven’t fully recovered. Secondly, the economy could weaken again with there being less of a stimulus. Remember, the $600 in weekly unemployment benefits lasted through the end of July. Retail sales would be especially likely to dip if cold weather or school reopenings lead to a 3rd wave of new COVID-19 cases.

Auto sales and parts were down 1.2% monthly and up 6.1% yearly which was down from 8.1% in the previous month. This is interesting because used car sales are on fire and lightweight vehicle sales in July were 14.5 million which was up from 13.1 million in June. Weakness in the biggest category caused the headline miss.

Monthly retail sales growth without autos was 1.9% which beat estimates for 1.5%. That’s even though last month’s growth was revised up a full 1% to 8.3%. June’s report was truly magical because of all the fiscal stimulus. Excluding autos and gas, monthly sales growth was 1.5% which beat estimates for 0.9%.

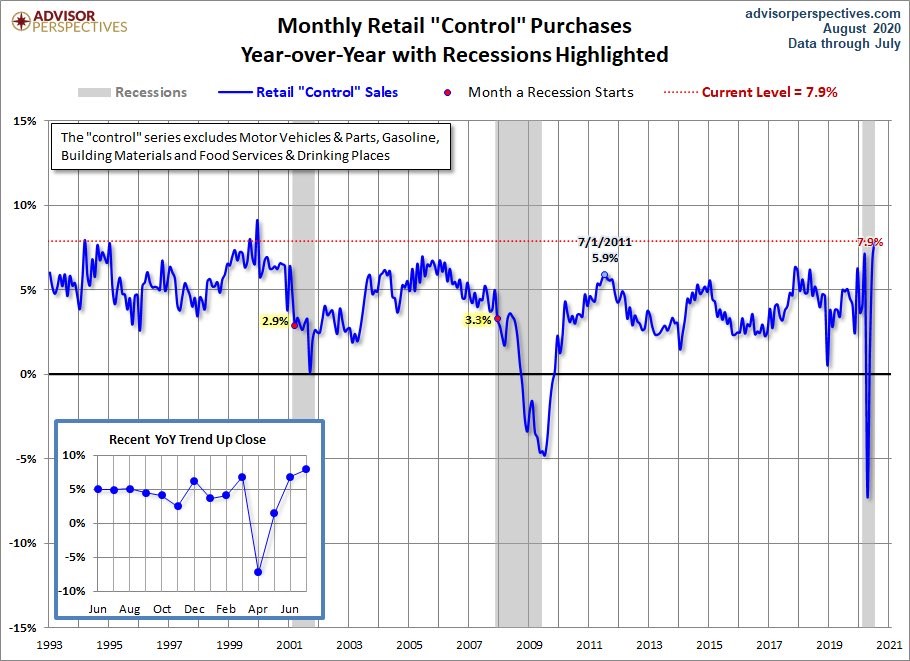

June’s growth was revised up by 1 point to 7.7%. Control group had 1.5% growth which beat estimates for 1%. Prior reading was revised from 5.7% to 6%. As you can see from the chart above, yearly growth was 7.9%. That’s the highest growth since 2000.

Details Of July’s Retail Sales Report

Just because sales are now above where they were before the recession doesn’t mean everything is back to normal. There has been a huge shift in how money is spent. As you can see from the chart below, overall nominal sales are 1.7% more than February. Online sales are 21.9% higher. It’s no surprise they won in a situation where human contact was discouraged.

In the next year, online sales will lose market share if COVID-19 cases continue to fall. That’s far outside the consensus as people think growth was accelerated by COVID-19 and won’t be given back. It sounds crazy to think we will go backwards, but the reality is people only shopped online because it was the only option.

Some of the spending will stick, but some won’t. Online sales growth was only 0.7% monthly, but it was 24.7% yearly. Momentum slowed, but we’re still way above last year.

Sporting goods sales are 17.6% higher than before the recession because people are doing more outdoor activities which are good for social distancing. It actually had a 5% decline on a monthly basis. People bought the items they needed in June. As the crisis is curtailed, there will be more declines.

Yearly growth was still 17.8%. Building materials and garden sales are 8.7% above February. Since people had more time at home, they improved their houses. Clothing and restaurant sales are still down 19.9% and 19.7% from February. Clothing and restaurants had strong monthly growth as they continued to recover. They had 5.7% and 5.1% monthly growth.

Off Price Retailers Back To Normal

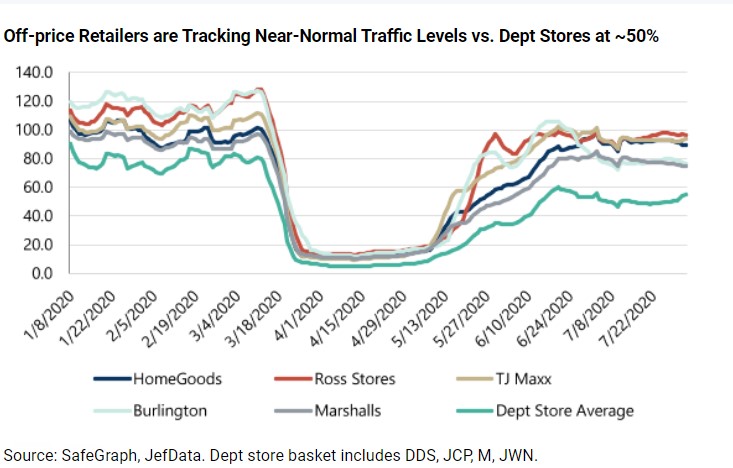

Off price retailers do well in recessions unlike premium priced stores because people trade down to cheaper items. As you can see from the chart below, department store sales are down over 40%. 3 off price retailers’ traffic were only down slightly and 2 had traffic declines of about 20%. Retail isn’t dead, but the department store like Macy’s is. The consumer wants a good deal.

Good Day For COVID-19 Recovery

After some bad days this week, COVID-19 improved on Friday. There were 60,600 new cases which sounds like a lot, but isn’t because Friday is typically the peak for the week. Last week had 63,413 cases on Friday. The 7 day average of new cases is now 54,102.

It has been starting to fall quicker in the past couple days. I’m hoping it gets below 50,000 by the end of the month. This wasn’t a good week for deaths, but they fell on Friday as there were 1,120 which was down from 1,292 last week. 7 day average will likely fall below 1,000 next week and will approach 800 by the end of the month.

Conclusion

Retail sales have fully recovered from the recessionary decline, but many areas like restaurants and clothing have much more room to recover. Good news is the labor market recovered in August. Bad news is there is less stimulus money which drove the recovery in spending. This was an ok week for new cases, but deaths didn’t fall which was unfortunate. They will likely fall sharply next week.